Opportunity… Not Concern

“Davidson” submits:

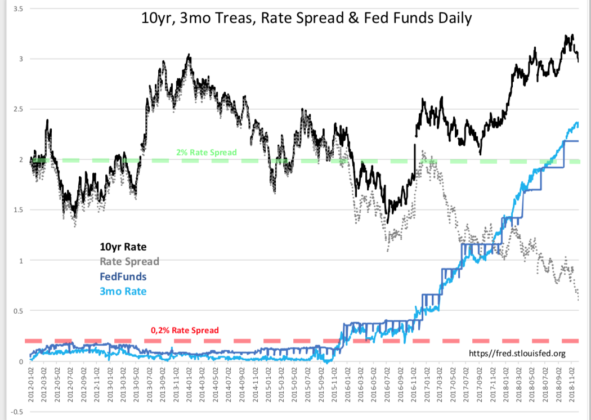

Most use what they have been taught in B’School about ‘Inverted Yields’, i.e. the 2yr vs 10yr. History shows it is the T-Bill/10yr Treasury rate spread which is most important and most reliable. Today we see 0.60% when 0.20% is the historical level for credit extension pull-back and the inability to refinance riskier credits. It is the riskier credits which default due to lack of refinancing that lead to the negative shift in the psychology of credit extension that produces recessions.

Historically, since 1953, experience teaches that the T-Bill/10yr rate spread falling below 0.20% arises from investors selling T-Bill holdings to invest in equities. This is the basis for the term “Speculative Top” when discussing market cycle peaks/ Market peaks always derive from excessive equity market optimism and excessive credit extension which is suddenly impacted by lenders unexpectedly pulling back. Borrowers only options are to sell assets or default on the debt loaned against the assets. Typically, both events occur and defaults rise as asset prices fall.

The current market pessimism defies previous market tops. There is something else going on.

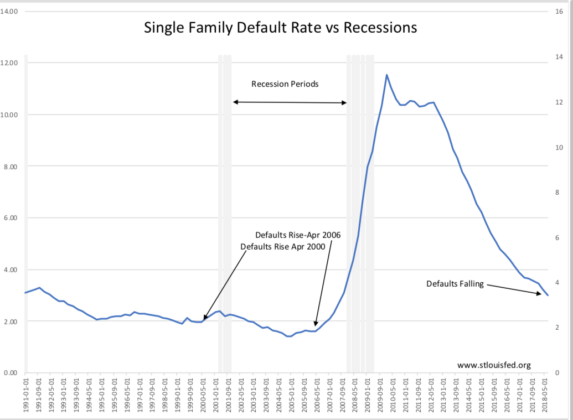

In support of continued economic expansion and counter to our high level of pessimism is that mortgage default rates have been falling and continue to fall.

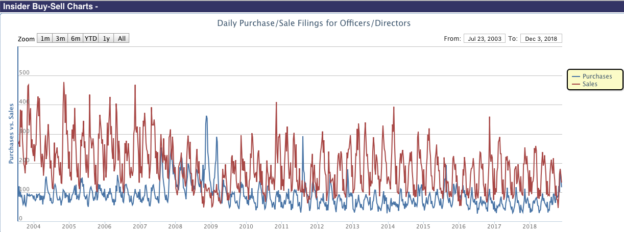

In lock-step with other periods of high market pessimism when economic activity remained strong is the ratio of Insider Buying/Selling. Recently Insider Buying has produced multiple days when Buys exceed Sales, BLUE LINE higher than the RED LINE. Insider has a long history of being a reliable economic forecasting tool and identifying periods when market prices under-valued business outcomes. http://openinsider.com/charts

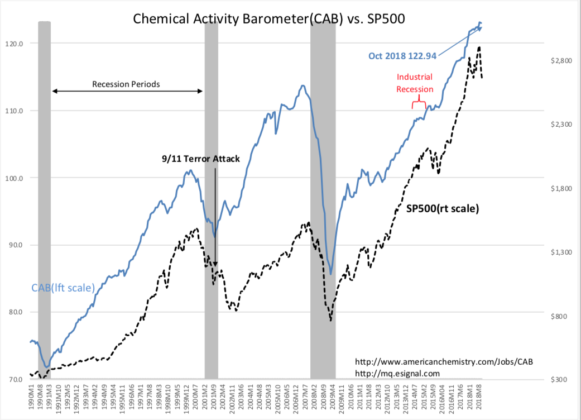

Important to the economic view is the CAB(Chemical Activity Barometer) with a history traced from 1919. The current trend of monthly higher revisions is a strong indicator of future economic expansion.

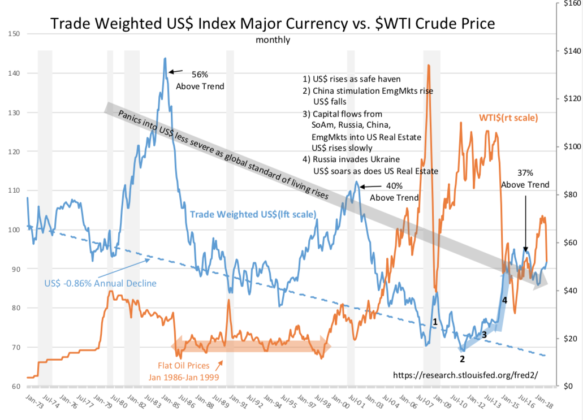

Lost in today’s conversation is the US role in the context of global economics and global investment markets. The US, having the strongest property protections, becomes a safe haven when risks to capital appear elsewhere. The US$(US Dollar) has always risen as a result till fears of this type have eased. Russia’s incursion into Ukraine and recent belligerent action continues to raise global fear. The US$ is markedly higher as a result. Add this geopolitical fear to the recent US tariff policy shift demanding lower global tariffs and one can identify multiple sources driving market pessimism and uncertainty in foreign markets.

Foreign markets began declining Spring 2018. Oil prices have plummeted as a result of 1) fears of over-production, 2) fears of declining demand and 3) fear of recession driven by inverse algorithm correlations of recessions to a rising US$. While we are at it, let’s just toss into the mix a poorly defined basket of heightened concerns. When one sums the many prominent perceptions at the moment, the default option, when confusion is heightened, becomes the interpretation that that ‘falling markets predict falling economies’.

The Investment Thesis:

If the economic threat is real, then it should be reflected in the key economic data which correlate well with predicting economic corrections. It is not! What produces any investment opportunity is how wide is the discrepancy between economic values and market perceptions. Today, the discrepancy providing opportunities for buyers is quite wide.

The recommendation is to buy equities.

Disclosure: The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or ...

more