Navigating With The R Star

“It’s difficult to make predictions, especially about the future.” – Niels Bohr

On November 28, 2018, Federal Reserve (Fed) Chairman Jerome Powell gave a speech at the Economics Club of New York that sent the stock market soaring by over 2%. The reason cited by market pundits was the reversal of language he used a few weeks earlier suggesting that the Fed still had several more rate hikes ahead. In other words, he softened that tone and seemed to imply that the Fed was close to pausing.

By most accounts, Fed policy remains very accommodative but the “Powell Pivot”, which began in late November and continues to this day, hinges on an obscure metric called R-Star (r*). Even though interest rates have been held low and vast amounts of liquidity force fed into markets through quantitative easing, the idea that interest rates should not rise much further presents a unique dilemma for the Fed. Rationalizations for their guidance hinges on r*. Before going into details about this important measure, let us reflect on history.

Doomed To Repeat It

“Well, we currently see the economy as continuing to grow, but growing at a relatively slow pace, particularly in the first half of this year. As the housing contraction begins to wane, as it should sometime during this fiscal year, the economy should pick up a bit later in the year. –Federal Reserve Chairman Ben Bernanke on January 17, 2008, in response to Congressman John Spratt ranking member of the House Budget Committee

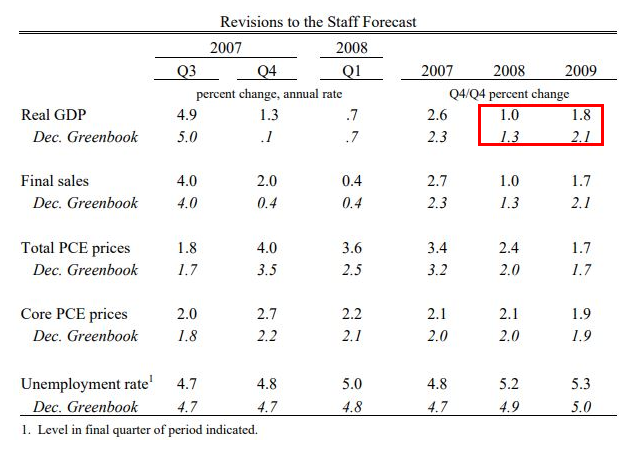

The table below was a document used on an unscheduled Fed conference call on January 9, 2008, to discuss deteriorating credit conditions in the U.S. economy. At that time and unbeknownst to the Fed, the economy slipped into recession the prior month, yet the Fed’s commentary and one- and two-year outlook for growth remained positive. The point is not to deride Bernanke and the Fed but show that even the most well-informed Ph.D. economists struggle to forecast economic activity or assess current economic conditions properly.

(Click on image to enlarge)

The challenge in assessing the outlook for a highly complex system like the U.S. economy cannot be overstated. Yet, what we saw in the past and still see currently, is a small group of people with enormous influence over the economy failing to grasp the natural mechanisms of a market economy. To put it another way, the Fed continues to believe that they know things they simply cannot know, and most concerningly, they set monetary policy on the basis of that fallacy.

An Abstract Barometer

Over the past several years, Fed economists invented a concept that purportedly identifies the point at which monetary policy is “neutral” or in equilibrium with economic activity. This number, called r* (r-star), is abstract and imprecise as it requires a variety of assumptions about the level of interest rates and economic activity. R* is formally defined as the “inflation-adjusted, short-term interest rate that is consistent with the full use of economic resources and steady inflation at or near the Fed’s target level.”

As discussed in Clues from the Fed II – A Review of Jerome Powell’s Speech 11/27/18, his exact language was the following:

“Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy – that is, neither speeding up nor slowing down growth.”

The current “target level” for the Fed Funds rate, the primary interest rate lever used to impact the economy by altering interest rates, is currently in a range of 2.25-2.50%. What Powell seems to have implied, or what the market gleaned from the comment above, is that the Fed may only increase the target rate by another 0.25-0.50% as opposed to the 1.00-1.50% forecast by the very same Fed just two months prior. The extent to which the Fed is willing to tighten monetary policy by raising interest rates has a dramatic impact on the amount of risk investors are willing to take. Thus, with the dovish change in Powell’s language, the stock market took off.

Just The Facts

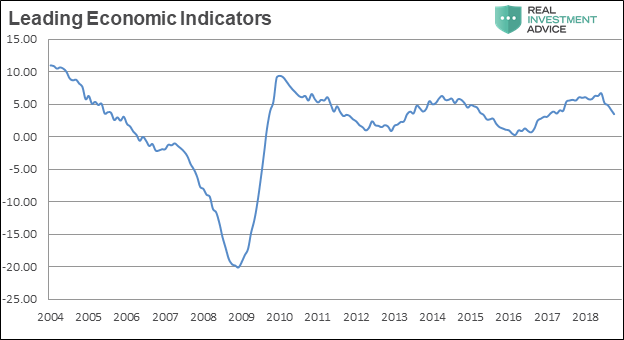

The data on the economy remains robust. Annualized GDP growth through the 3rd quarter of 2018 was 3.3% and the unemployment rate sat near a historic low at 3.9%. The regional surveys from the Fed consistently reflect that companies are having difficulty finding qualified workers, which implies that demand is good and wage growth, a key determinant of inflation, is likely to move higher. The index of Leading Economic Indicators remains solidly positive and consumer and business sentiment surveys nationally, while weakening, continue to point towards expansion.

(Click on image to enlarge)

Data Courtesy: St. Louis Federal Reserve

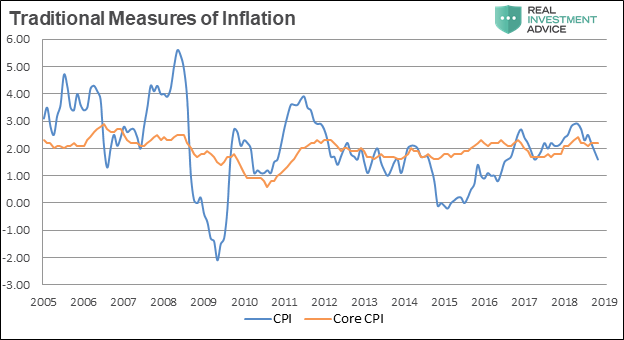

Examining charts of various measures of inflation also offers insight into current circumstances. The traditional measures of inflation, Consumer Price Inflation (CPI) and Core (ex-food & Energy) CPI seem benign with core levels at roughly 2.2% although those indicators have declined modestly in recent months.

(Click on image to enlarge)

Data Courtesy: St. Louis Federal Reserve

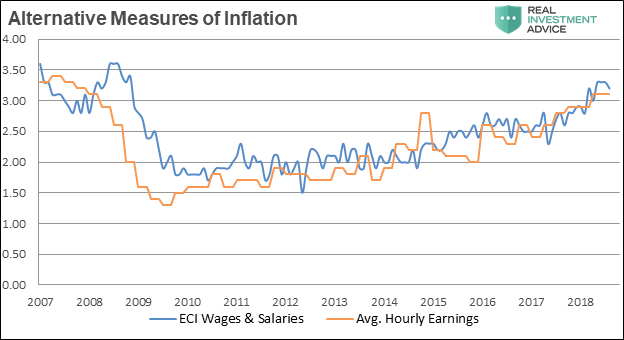

Alternative inflation indicators like the Employment Cost Index (ECI) wages and average hourly earnings reflect a steady trend of rising wage pressures as shown in the chart below.

(Click on image to enlarge)

Data Courtesy: St. Louis Federal Reserve

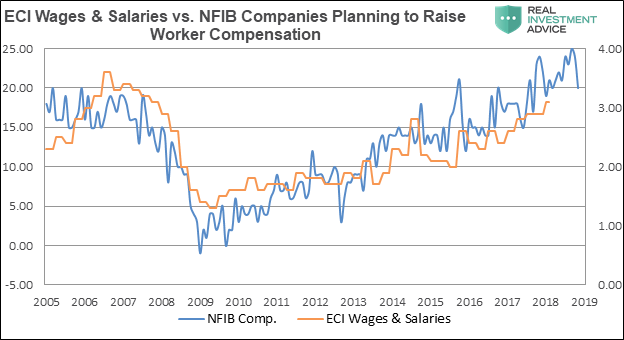

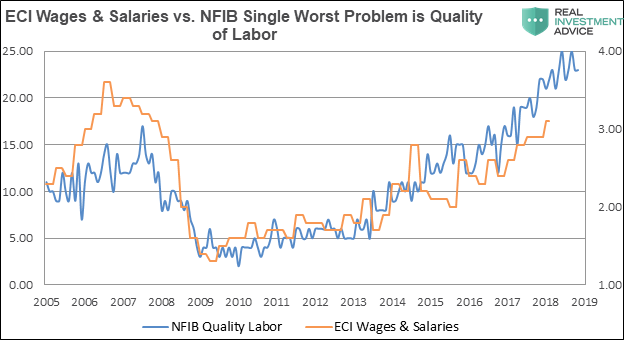

The chart below uses the ECI Wages and Salaries data from above and compares it with two components of compensation from the NFIB small business survey. As shown, both metrics demonstrate mounting wage pressures. The NFIB survey shows that companies planning to raise worker compensation is trending higher. Additionally, the survey shows that the single biggest problem for small business is availability of quality labor (correlation using 9-month lead is over 76%) and that measure is also trending higher.

(Click on image to enlarge)

(Click on image to enlarge)

Data Courtesy: St. Louis Federal Reserve

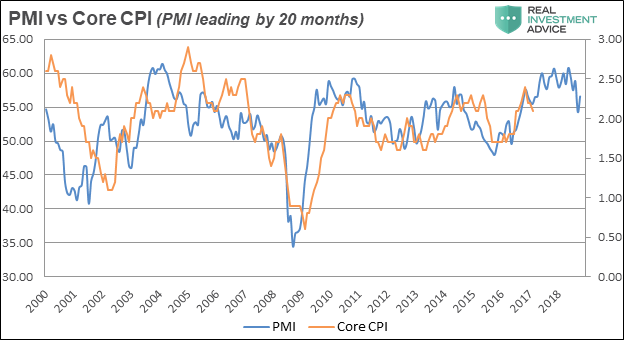

Manufacturing activity captured via the Purchasing Managers Index (PMI) appears to lead CPI with some durability. The correlation is 52% since 2000 and 76% since 2006. Given the current level of manufacturing activity, it suggests that Core CPI should remain above 2.0% over the next several months.

(Click on image to enlarge)

Data Courtesy: St. Louis Federal Reserve

Economies Are Hard To Forecast

Economic systems are complex with many hidden, unobservable and non-linear relationships making economic activity very difficult to forecast. However, by applying simple logic about possible outcomes, we can better frame the risks of higher inflation due to wage pressures. If, as is currently forecast, GDP growth begins to gradually decline as the effects of tax reform and fiscal stimulus diminish, then we should expect gains in employment to moderate. That scenario does not necessarily argue for unemployment to rise which leaves the current labor market situation tight. The effects described above would remain well in place and higher labor costs could reasonably push inflation higher. Higher inflation would put upward pressure on long-term interest rates while creating a headwind for corporate profits, margins and stock prices. That would not be good for most investors.

Another scenario, again given the difficulties associated with forecasting GDP, is that economic growth does not moderate as much as expected and remains somewhat above the post-crisis trend. Labor costs, in that case, would accelerate and could cause wage inflation to move meaningfully higher. Clearly, the risks emanating from that scenario would be very bad for both stocks and bonds and thus a world enamored with passive investing and awash in 60/40 portfolios.

Other Info

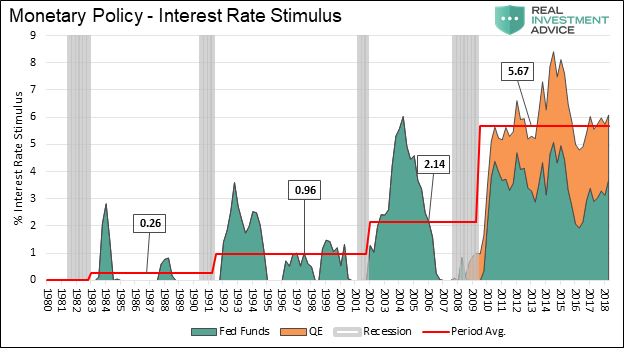

A cursory review of other economic data provides even more evidence that the level of interest rates is well below what it should be. Household net worth, industrial production and retail sales are all more than fully recovered from the crisis and have been for some time. Furthermore, the U.S. never experienced deflation, and thus the common point of comparison and rationalization for gradual policy adjustments – that the U.S. could end up in a situation akin to what Japan has been experiencing and combatting for decades – rings hollow. The counter-factual argument is that Fed actions prevented a “Japan-like” outcome, but there is no evidence to support that claim. All this strongly argues that the Fed Funds target rate remains not just slightly accommodative as Powell acknowledges but extremely accommodative.

The following graph, from our article Why Fed’s Monetary Policy Is Still Very Accommodative, shows that the current level of monetary policy is accommodative and unprecedented over the last four decades.

(Click on image to enlarge)

Fortunetellers

Since the financial crisis, the Fed has exerted ever more influence over the economy through extraordinary policy measures. Importantly, their financial crisis and post-crisis involvement came partially as a result of their prior involvement in stoking a housing and stock market bubble that in part led to the crisis.

Now, as they seek to reverse out of those policies, their job is proving more difficult than anticipated and contrary to what Bernanke, Yellen, and Dudley told us as they were enacting said policy. That circumstance does not appear to have imposed much humility on the Fed. Despite all their innovations, such as r*, complex labor market indicators, data dependency, and forward guidance, Jerome Powell is flying just as blind as Bernanke was in the early innings of the financial crisis. He confirmed this by reasserting and then reversing prior language around his assessment of the economy four times since October 3, 2018. This is not the most confidence-inspiring tactic for a Fed Chairman.

A more reliable approach to monetary policy would be to allow markets to dictate prices. Billions of buyers and sellers, borrowers and lenders, who transact every day are collectively better informed than the small group of unelected and unaccountable figureheads at the Fed. Should the Fed find the urge to become engaged, and it would be a rare occasion indeed, they should respond to market forces and stay out of the way of the robust pricing mechanisms of markets.

Summary

The analogy for the Fed and its approach to monetary policy is one of a driver on a curvy country road. A licensed driver obeying the law who pays attention to the speed limit and other important road signs indicating warnings should be able to successfully navigate to a destination. If, however, the driver decides to navigate by anticipating the contours of the road and confidently driving above the speed limit, he will eventually end up off the road, through a fence or over a cliff. Unfortunately, we are all passengers along for the Fed’s ride currently.

Most of us are willing passengers, having been convinced that the Fed knows what they are doing. That is understandable given the influence on markets from the trillions in liquidity they supplied, but it is not true. The consequences of years of excessive policy will eventually begin to reveal themselves, and we posit they already are. The intersection of manipulated economic forces and societal outrage are exhibit A. What is so confounding, is the misplaced trust in the entities and leaders that are causing the problems described.

R* and all the other economic terms that supposedly guide policy-makers are conjured from the realm of scientific economic analysis but human beings and their behavior cannot be modeled in a spreadsheet. The problem is the failure to apply proper humility or even common sense when crafting the formulas on which policies rest and livelihoods depend.

Disclaimer: Click here to read the full disclaimer.

Interesting article. The Fed did not know what it was doing in 2007-2008, as inflation was still strong as recession took hold. NGDP was falling like a rock. Libor was inverted with the Swap rate. Those things took banks to the end of their rope. Does the Fed know what it is doing now? Who knows?

When has it ever known?