Morning Call For Tuesday, Dec. 27

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 +0.06%) are up +0.06% and European stocks are up +0.10% in thin holiday trade. Markets in the UK, Australia and Hong Kong are closed today for holiday. A +0.30% rally in Feb WTI crude (CLG17 +0.26%) is positive for energy producing stocks, although a -0.22% decline in the price of Mar COMEX copper (HGH17 -0.22%) to a 1-1/4 month low is undercutting mining stocks and raw-material producers. Asian stocks settled mixed: Japan +0.03%, Hong Kong and Australia closed for holiday, China -0.25%, Taiwan -0.01%, Singapore +0.51%, South Korea +0.23%, India +1.57%. Economic concerns undercut Japanese stocks after Japan Nov household spending unexpectedly declined -1.5% y/y. Also, deflation concerns remain after Japan's Nov national CPI fell -0.4% y/y, weaker than expectations of -0.3% y/y and the ninth straight month prices have fallen.

The dollar index (DXY00 +0.17%) is up +0.07%. EUR/USD (^EURUSD) is down -0.08%. USD/JPY (^USDJPY) is up +0.19%.

Mar 10-year T-note prices (ZNH17 -0.09%) are down -3.5 ticks.

ECB Governing Council Member Knot said the ECB's assets purchase program prevents countries from taking structural reform measures and the program will have to come to an end at some point.

Japan Nov national CPI rose +0.5% y/y, right on expectations. Nov national CPI ex-fresh food fell -0.4% y/y, weaker than expectations of -0.3% y/y. Nov national CPI ex food & energy rose +0.1% y/y, right on expectations.

Japan Nov overall household spending unexpectedly fell -1.5%, weaker than expectations of +0.1% and the ninth consecutive month that spending has declined.

U.S. STOCK PREVIEW

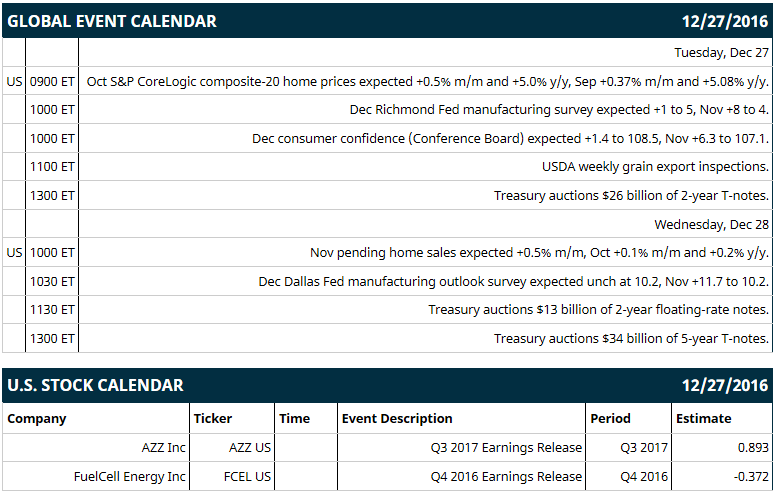

Key U.S. news today includes: (1) Oct S&P CoreLogic composite-20 home prices (expected +0.5% m/m and +5.0% y/y, Sep +0.37% m/m and +5.08% y/y), (2) Dec Richmond Fed manufacturing survey (expected +1 to 5, Nov +8 to 4), (3) Conference Board Dec U.S. consumer confidence index (expected +1.4 to 108.5, Nov +6.3 to 107.1), (4) Treasury auctions $26 billion of 2-year T-notes, (5) USDA weekly grain export inspections.

Russell 1000 earnings reports today include: none.

U.S. IPO's scheduled to price today: none.

Equity conferences this week: none.

OVERNIGHT U.S. STOCK MOVERS

Disney (DIS -0.26%) may move to the upside in today's trading after its 'Rogue One' movie was the number one movie seen over the weekend according to ComScore.

Lions Gate Entertainment (LGF +4.40%) was initiated with a 'Buy' at Argus Research with a 12-month price target of $34.

Ritchie Bros. Auctioneers (RBA +2.21%) was downgraded to 'Market Perform' from 'Outperform' at Raymond James.

Sotheby's (BID +1.84%) was rated a new 'Buy' at Sidoti & Company with a 12-month target price of $54.

Hologic's (HOLX +0.65%) received U.S. FDA approval for commercial distribution of its HIV-1 test.

MacroGenics (MGNX +6.59%) was granted orphan drug status by the U.S. FDA for its Cd123 X drug in treatment of acute myeloid leukemia.

Shire (SHPG +1.43%) said the U.S. FDA approved its hemophilia therapy of Adynovate in pediatric patients under 12 years old and for use in surgical settings for adult patients.

International Value Advisers cut its stake in DeVry Education Group (DV +0.47%) to 7.0% from 8.5%.

Point72 Asset Management cut its stake in Whiting Petroleum (WLL +0.32%) to 1.9% from 5.7%.

Protalix Biotherapeutics (PLX unch) jumped 8% in pre-market trading after it received a $24.3 million order for its alfataligilicerase drug to treat Gaucher patients in Brazil by the Brazilian Ministry of Health.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 +0.06%) this morning are up +1.25 points (+0.06%). Friday's closes: S&P 500 +0.13%, Dow Jones +0.07%, Nasdaq +0.11%. The S&P 500 on Friday closed slightly higher on the +5.2% increase in U.S. Nov new home sales to a 4-month high of 592,000 (stronger than expectations of +2.1% to 575,000) and on the unexpected +0.2 point gain in Dec University of Michigan U.S. consumer sentiment index to 98.2 (stronger than expectations of unchanged and the highest in 12-3/4 years). Stocks were undercut by concerns about Chinese economic growth after Chinese President Xi Jinping said he's open to China's GDP slowing below the government's 6.5% annual target.

Mar 10-year T-notes (ZNH17 -0.09%) this morning are down -3.5 ticks. Friday's closes: TYH7 +3.00, FVH7 +1.75. Mar 10-year T-notes on Friday climbed to a 1-week high and settled higher on carry-over support from a rally in German bunds to a 3-week high and on Chinese President Xi Jinping's comment that he is open to China's GDP growth slowing below the government's 6.5% GDP target, which would lead to slower global economic growth.

The dollar index (DXY00 +0.17%) this morning is up +0.070 (+0.07%). EUR/USD (^EURUSD) is down -0.008 (-0.08%). USD/JPY (^USDJPY) is up +0.22 (+0.19%). Friday's closes: Dollar index -0.080 (-0.08%), EUR/USD +0.0019 (+0.18%), USD/JPY -0.21 (-0.18%). The dollar index on Friday closed lower on the decline in U.S. T-note yields and on long liquidation pressure ahead of the long Christmas holiday weekend.

Feb WTI crude oil (CLG17 +0.26%) prices this morning are up +16 cents (+0.30%) and Feb gasoline (RBG17 -0.18%) is down -0.0009 (-0.05%). Friday's closes: Feb crude +0.30 (+0.57%), Feb gasoline +0.0162 (+1.00%). Feb crude oil and gasoline on Friday settled mixed. Crude oil prices were boosted by the weaker dollar and by the rise in the crack spread to a 1-1/2 month high, which may boost refinery demand for crude to refine into gasoline. Crude oil prices were undercut by news that Libyan crude oil returned to the global market after crude cargoes were loaded at the Es Sider terminal, Libya's biggest oil export terminal, for the first time in two years due to the civil war.

(Click on image to enlarge)

Disclosure: None.