Morning Call For September 29, 2016

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 -0.03%) are down -0.07%, as crude oil (CLX16 -0.09%) drops -0.60% and gives back some of yesterday's sharp rally. European stocks are up +0.73% as energy stocks there catch up to the rally in U.S. stocks late yesterday after OPEC unexpectedly cut its production target. Another positive for European equities was the unexpected increase in Eurozone Sep economic confidence to an 8-month high. Asian stocks settled mostly higher: Japan +1.39%, Hong Kong+0.51%, China +0.36%, Taiwan +0.83%, Australia +1.09%, Singapore +0.97%, South Korea +0.83%, India -1.64%. India's BSE Sensex Stock Index sold-off over 1.6% after India launched a raid into Pakistan to attack terrorist targets. Japanese stocks rose as exporters rallied after USD/JPY rose to a 1-week high, which boosts exporters' earnings prospects.

The dollar index (DXY00 +0.06%) is up +0.12%. EUR/USD (^EURUSD) is up +0.01%. USD/JPY (^USDJPY) is up +0.74% at a 1-week high.

Dec 10-year T-note prices (ZNZ16 -0.12%) are down -5.5 ticks.

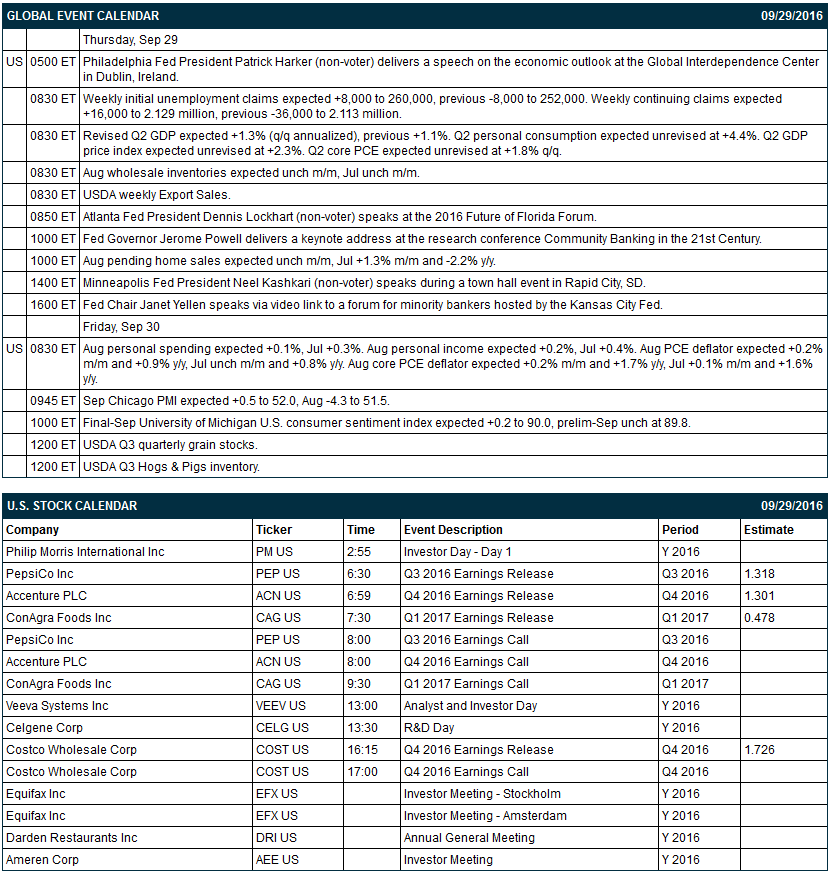

Speaking in Dublin, Ireland, Philadelphia Fed President Harker said he's "somewhat concerned" about falling behind the curve and that "he tends to be in the camp of normalizing interest rates sooner, rather than later. He added that "every meeting is a live meeting" for the FOMC to change monetary policy.

Eurozone Sep economic confidence rose +1.4 to 104.9, stronger than expectations of unch at 103.5 and the highest in 8 months. The Sep business climate indicator rose +0.42 to 0.45, stronger than expectations of +0.03 to 0.05 and the highest in 11 months.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Philadelphia Fed President Patrick Harker (non-voter) delivers a speech on the economic outlook at the Global Interdependence Center in Dublin, Ireland, (2) weekly initial unemployment claims (expected +8,000 to 260,000, previous -8,000 to 252,000) and continuing claims (expected +16,000 to 2.129 million, previous -36,000 to 2.113 million), (3) revised Q2 GDP expected +1.3% (q/q annualized) vs previous +1.1%, (4) Aug wholesale inventories (expected unch m/m, Jul unch m/m), (5) Atlanta Fed President Dennis Lockhart (non-voter) speaks at the 2016 Future of Florida Forum, (6) Fed Governor Jerome Powell delivers a keynote address at the research conference “Community Banking in the 21st Century,” (7) Aug pending home sales (expected unch m/m, Jul +1.3% m/m and -2.2% y/y), (8) Minneapolis Fed President Neel Kashkari (non-voter) speaks during a town hall event in Rapid City, SD, (9) Fed Chair Janet Yellen speaks via video link to a forum for minority bankers hosted by the Kansas City Fed, (10) USDA weekly Export Sales.

Russell 1000 companies that report earnings today: Accenture (consensus $1.30), PepsiCo (1.32), ConAgra Foods (0.48), Costco (1.73).

U.S. IPO's scheduled to price today: Independence Realty Trust (IRT), Nutanix (NTNX).

Equity conferences during the remainder of this week include: Leerink Partners Rare Disease & Immuno Oncology Roundtable Conference on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

Fitbit (FIT +1.03%) fell 3% in pre-market trading after it was dowmgraded to 'Underweight' from 'Sector Weight' at Pacific Crest.

Targa Resources (TRGP +4.90%) was downgraded to 'Hold' from 'Buy' at Stifel.

Incyte (INCY +4.64%) was upgraded to 'Outpeform' from 'Market Perform' at Raymond James with a 12-month target price of $115.

eBay (EBAY -0.28%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank.

Progress Software (PRGS +1.61%) tumbled 10% in after-hours trading after it reported Q3 adjusted EPS of 44 cents, below consensus of 45 cents, and said it sees Q4 adjusted EPS of 55 cents-58 cents, on the low end of consensus of 58 cents.

Vertex Pharmaceuticals (VRTX -0.31%) lost 2% in after-hours trading after it cut its Orkambi revenue view to $950 million-$990 million from a prior view of $1.0 billion-$1.1 billion.

Transocean (RIG +6.37%) may open lower today after Carl Icahn said he reduced his position in the company to 5.45 million shares from 21.5 million shares on June 30 for tax purposes.

Vulcan Materials (VMC +1.26%) slipped almost 1% in after-hours trading after it said it sees 2016 adjusted Ebitda trending toward $1 billion, below consensus of $1.09 billion.

Himax Technologies (HIMX -6.85%) gained nearly 2% in after-hours trading after it was rated a new 'Buy' at Roth Capital with a price target of $10.

Pier 1 Imports (PIR +2.15%) lost 1% in after-hours trading after it cut its view on full-year adjusted EPS to 24 cents-32 cents from a June 29 view of 32 cents-40 cents.

Globalstar (GSAT unch) rose over 3% in after-hours trading after it said initial test flight results "indicated continuous communication" in the testing of its ADS-B Link Augmentation System in a NASA test flight.

Aegerion Pharmaceuticals (AEGR -9.45%) jumped over 20% in after-hours trading after Japan's Ministry of Health, Labor & Welfare approved Aegerion's Juxtapid capsules for patients with homozygous familial hypercholesterolemia.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 -0.03%) this morning are down -1.50 points (-0.07%). Wednesday's closes: S&P 500 +0.53%, Dow Jones +0.61%, Nasdaq +0.18%. The S&P 500 on Wednesday closed higher on a rally in energy producer stocks on the +5.57% surge in crude oil prices seen after news that OPEC agreed in principle to limit oil production. Stocks were also boosted by the +0.6% increase in U.S. capital spending (Aug capital goods orders nondefense ex-aircraft), stronger than expectations of -0.1%. Stocks were undercut by Fed Chair Yellen's comment that most FOMC members believe an interest rate increase is needed this year.

Dec 10-year T-notes (ZNZ16 -0.12%) this morning are down -5.5 ticks. Wednesday's closes: TYZ6 -3.00, FVZ6 -1.25. Dec 10-year T-notes on Wednesday settled mildly lower. T-note prices were undercut by a rally in stocks and the stronger-than-expected U.S. Aug durable goods orders report. T-notes were also undercut by Fed Chair Yellen's hawkish comment that a majority of FOMC members believe a rate hike will be necessary this year. In addition, San Francisco Fed President Williams said the U.S. economy can "handle" a rate hike.

The dollar index (DXY00 +0.06%) this morning is up +0.119 (+0.12%). EUR/USD (^EURUSD) is up +0.0001 (+0.01%). USD/JPY (^USDJPY) is up +0.75 (+0.74%) at a 1-week high. Wednesday's closes: Dollar index -0.004 (unch), EUR/USD +0.0002 (+0.02%), USD/JPY +0.26 (+0.26%). The dollar index on Wednesday closed little changed. The dollar was boosted by the smaller-than-expected decline in U.S. Aug durable goods orders and Fed Chair Yellen's comment that most FOMC participants see a rate hike as likely this year.

Nov WTI crude oil (CLX16 -0.09%) this morning is down -28 cents (-0.60%) and Nov gasoline (RBX16 -0.91%) is down -0.0181 (-1.26%). Wednesday's closes: Nov crude +2.49 (+5.57%), Nov gasoline +0.0777 (+5.70%). Nov crude oil and gasoline on Wednesday closed higher with Nov crude at a 2-week high. Crude oil prices were boosted by OPEC's surprise preliminary agreement to cut its oil production to 32.5 million bpd, which would be its first output cut in 8 years. Crude oil prices were also boosted by the unexpected -1.88 million bbl decline in EIA crude inventories to a 7-1/2 month low (vs expectations of +3.0 million bbl) and the -631,000 bbl decline in Cushing crude oil inventories to a 9-month low. Crude oil prices were undercut by a stronger dollar and by the +2.03 million bbl increase in EIA gasoline stockpiles, more than expectations of +500,000 bbl.

(Click on image to enlarge)

Disclosure: None.