Morning Call For Sept. 29, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.62%) this morning are down -0.63% and European stocks are down -0.57% after Eurozone Sep economic confidence fell to a 10-month low. A slide in European bank stocks is weighing on the overall market as well with Commerzbank AG down nearly 4% after a person with knowledge of the matter said the bank faces a U.S. inquiry into whether it broke anti-money laundering laws. Also, HSBC and Standard Chartered PLC both fell over 1% after they closed some of their Hong Kong branches as pro-democracy protesters clashed with police. The ruble fell to a record low of 39.59 per dollar on concern that EU and U.S. sanctions against Russia will propel capital outflows out of Russia. Asian stocks closed mixed: Japan +0.50%, Hong Kong -1.90%, China +0.43%, Taiwan -0.32%, Australia -0.93%, Singapore -0.08%, South Korea -0.15%, India -0.11%. Japanese exporters rose and led Japan's Nikkei Stock Index higher as a slide in the yen to a fresh 6-year low against the dollar boosted the earnings prospects of Japanese exporters. Commodity prices are mixed. Nov crude oil (CLX14 -0.50%) is down -0.55%. Nov gasoline (RBX14 +0.42%) is up +0.28%. Dec gold (GCZ14+0.65%) is up +0.52%. Dec copper (HGZ14 -0.18%) is down -0.21% at a 3-1/2 month low on Chinese demand concerns after China Aug industrial profits fell for the first time in 2 years. Agriculture prices are mixed with Nov soybeans down -0.22% at a 4-1/2 year low as U.S, farmers begin to harvest a record crop. The dollar index (DXY00 -0.10%) is down -0.02%. EUR/USD (^EURUSD) is up +0.02%. USD/JPY (^USDJPY) is up +0.18% at a fresh 6-year high. Dec T-note prices (ZNZ14 +0.20%)are up +5.5 ticks.

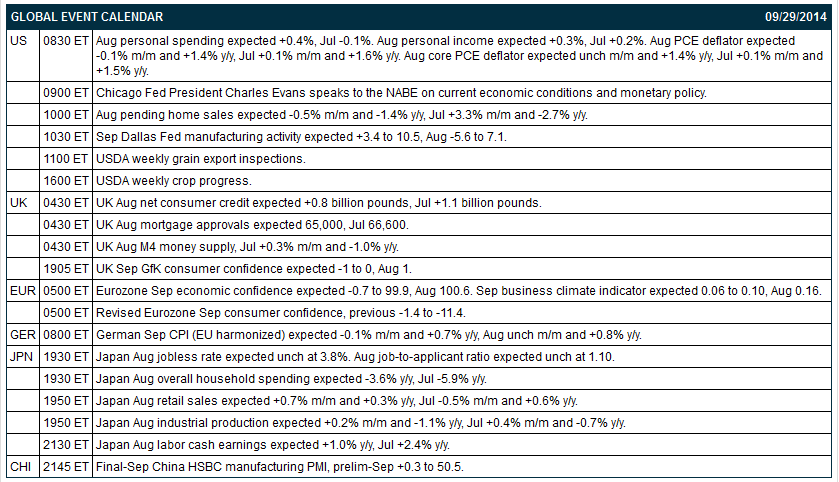

Eurozone Sep economic confidence fell -0.7 to 99.9, right on expectations and the lowest in 10 months. The Eurozone Sep business climate indicator fell-0.9 to 0.07, a larger decline than expectations of -0.06 to 0.10 and the lowest in 11 months.

UK Aug net consumer credit rose +0.9 billion pounds, more than expectations of +0.8 billion pounds.

UK Aug mortgage approvals were 64,200, less than expectations of 65,000, and Jul was revised lower to 66,100 from the originally reported 66,600.

China Aug industrial profits fell -0.6% y/y, the first decline in 2 years.

U.S. STOCK PREVIEW

Today's Aug personal income and spending reports is expected to improve to +0.3% and +0.4%, respectively, from the July reports of +0.2% and -0.1%. Today's Aug PCE deflator is expected to ease to +1.4% y/y from +1.6% y/y in July. Meanwhile, today's Aug core PCE deflator is expected to ease to +1.4% y/y from +1.5% in July. Today’s Aug pending home sales report is expected to show a decline of -0.5% m/m, falling back after the +3.3% increase seen in July. There is one of the Russell 1000 companies that report earnings today: Cintas (consensus $0.75).

Equity conferences this week include APICS Supply Chain Council - Europe conference 2014 on Mon, European Society for Medical Oncology (ESMO) Meeting on Mon, Oracle OpenWorld 2014 on Mon-Wed, Johnson Rice Energy Conference on Mon-Tue, Bloomberg Canadian Fixed Income Conference on Tue, SACHS ASSOCIATES - Biotech in Europe Forum For Global Partnering & Investment on Tue, Deutsche Bank Leveraged Finance Conference on Tue, Leerink Partners Rare Disease Roundtable on Tue, JMP Securities Financial Services & Real Estate Conference on Tue, TAG Fall Consumer Conference on Tue, Unconventional Resources Conference Canada 2014 on Wed, and Paris Motor Show 2014-Press Days on Thu.

OVERNIGHT U.S. STOCK MOVERS

Ferrellgas Partners LP (FGP +1.44%) reported a Q4 EPS loss of -58 cents, wider than consensus of a -31 cent loss.

Mattel (MAT -1.25%) was downgraded to 'Neutral' from 'Buy' at MKM Partners.

Baidu (BIDU +0.68%) was upgraded to 'Buy' from 'Neutral' at UBS.

FedEx (FDX +1.67%) was upgraded to 'Outperform' from 'Market Perform' at Cowen.

Rent-A-Center (RCII +0.03%) was upgraded to 'Buy' from 'Hold' at KeyBanc.

Janus Capital (JNS +43.02%) was upgraded to 'Equal Weight' from 'Underweight' at Morgan Stanley.

Encana (ECA +0.86%) acquires Athlon Energy (ATHL +2.61%) for $58.50 per share or $5.93 billion.

Nike (NKE +12.23%) was upgraded to 'Outperform' from 'Neutral' at Credit Suisse.

Allianz (AZSEY -6.14%) was downgraded to 'Neutral' from 'Outperform' at Credit Suisse.

The U.S. Navy awarded Raytheon (RTN +1.33%) a $251 million contract to procure Tomahawk Block IV tactical cruise missiles for fiscal year 2014 with an option for 2015 for the U.S. Navy and for the U.K. Royal Navy.

HealthCor Management reported a 4.0% stake in Allscripts (MDRX +1.04%) .

Point72 Asset reported a 5.1% passive stake in Stage Stores (SSI +1.95%) .

Meritage Group reported a 5.0% passive stake in Sally Beauty Supply (SBH +0.47%) .

Alimera Sciences (ALIM -3.90%) soared over 25% in after-hours trading after it announced that the FDA has approved its Iluvien drug for the treatment of diabetic macular edema.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 -0.62%) this morning are down -12.50 points (-0.63%). The S&P 500 index on Friday closed higher: S&P 500 +0.86%, Dow Jones +0.99%, Nasdaq +1.15%. The main bullish factor Friday was the upward revision in U.S. Q2 GDP to +4.6% q/q annualized from +4.2%, right on expectations and the fastest pace of expansion since Q4 of 2011. On the negative side was the final-Sep U.S. consumer confidence index from the University of Michigan, which came in unchanged at 84.6, weaker than expectations of +0.2 to 84.8.

Dec 10-year T-notes (ZNZ14 +0.20%) this morning are up +5.5 ticks. Dec 10-year T-note futures prices on Friday fell back from a 2-week high and closed lower. Bearish factors included (1) reduced safe-haven demand for Treasuries after stocks rallied, and (2) concern that the departure of Bill Gross, the manager of the world’s largest bond fund at PIMCO, may lead to reduced exposure in the fund to U.S. Treasury securities. Closes: TYZ4 -10.00, FVZ4-6.75.

The dollar index (DXY00 -0.10%) this morning is down -0.014 (-0.02%). EUR/USD (^EURUSD) is up +0.0003 (+0.02%) and USD/JPY (^USDJPY) is up +0.20 (+0.18%) at a 6-year high. The dollar index on Friday climbed to a new 4-year high and closed higher. Bullish factors included (1) the upward revision to U.S. Q2 GDP to +4.6%, the fastest pace of growth since Q4 of 2011, and (2) weakness in EUR/USD which dropped to a 1-3/4 year low after German Oct GfK consumer confidence fell to a 9-month low and after ECB Governing Council member Coene said the situation in the Eurozone “remains fragile.” Closes: Dollar index +0.445 (+0.52%), EUR/USD -0.00684 (-0.54%), USD/JPY +0.522 (+0.48%).

Nov WTI crude oil (CLX14 -0.50%) this morning is down -51 cents (-0.55%) and Nov gasoline (RBX14 +0.42%) is up +0.0069 (+0.28%). Nov crude and gasoline prices on Friday settled mixed: CLX4 +1.01 (+1.09%), RBXX4 -0.0517 (-2.04%). Crude prices rose on signs of increased U.S. fuel demand after Q2 GDP was revised higher to +4.6%, the fastest pace of expansion since Q4 of 2011. Gasoline prices fell after the dollar index rose to a 4-year high and on speculation that gasoline supplies in the U.S. Northeast will be adequate despite the shutdown of Irving Oil’s 146,000 bpd St. John, New Brunswick, refinery.

Disclosure: None