Morning Call For Sept. 23, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.33%) this morning are down -0.25% and European stocks are down -1.22% after a gauge of European manufacturing activity weakened more than expected to its slowest pace in 14 months. Geopolitical concerns in the Middle East are another negative for stocks as Saudi Arabia, Jordan, the United Arab Emirates, Qatar and Bahrain joined the U.S. in a series of airstrikes against Islamic State positions in Syria along the Iraqi border. Meanwhile, Israel shot down a Syrian fighter jet after it penetrated Israeli airspace over the Golan Heights. Asian stocks closed mixed: Japan closed for holiday, Hong Kong -0.49%, China +0.86%, Taiwan -0.54%, Australia +0.98%, Singapore +0.05%, South Korea -0.64%, India -1.58%. Chinese stocks rallied and closed higher after a gauge of China's manufacturing activity unexpectedly increased. Commodity prices are mostly higher. Nov crude oil (CLX14 +0.78%) is up +0.47%. Nov gasoline (RBX14 +0.95%) is up +0.37%. Dec gold (GCZ14 +1.27%) is up +0.73%. Dec copper (HGZ14 +0.31%) is up +0.26%. Agriculture and livestock prices are mostly lower. The dollar index (DXY00 -0.37%) is down -0.35%. EUR/USD (^EURUSD) is up +0.29%. USD/JPY (^USDJPY) is down -0.35%. Dec T-note prices (ZNZ14 +0.11%) are up +4 ticks.

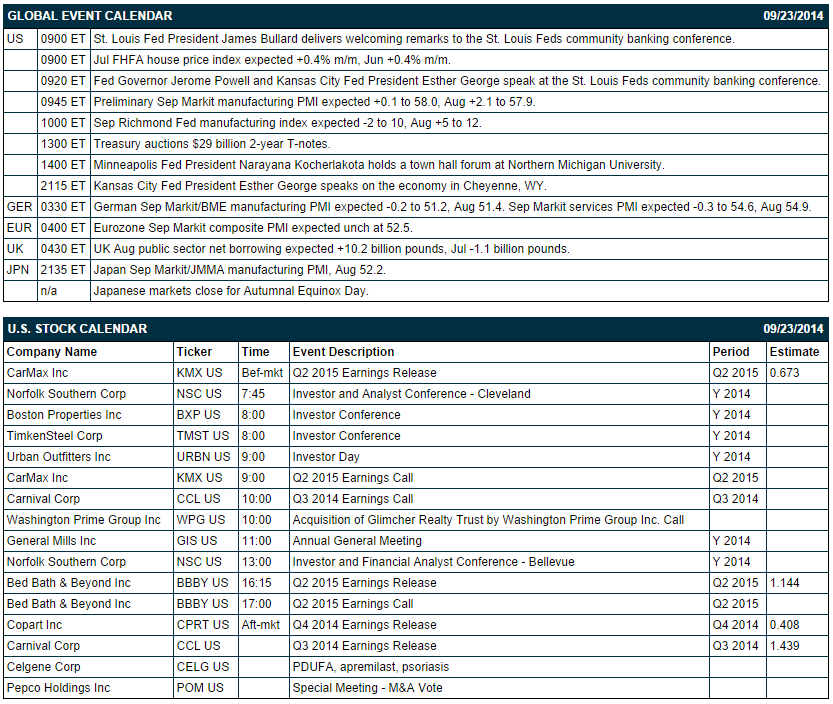

The Eurozone Sep Markit manufacturing PMI fell -0.2 to 50.5, a bigger drop than expectations of -0.1 to 50.6 and the slowest pace of expansion in 14 months.

The Eurozone Sep Markit composite PMI fell -0.2 to 52.3, weaker than expectations of no change at 52.5 and the slowest pace of expansion in 9 months.

The German Sep Markit/BME manufacturing PMI fell -1.1 to 50.3 a bigger decline than expectations of -0.2 to 51.2 and the slowest pace of expansion in 15 months.

The China Sep HSBC manufacturing PMI unexpectedly rose +0.3 to 50.5, better than expectations of -0.2 to 50.0.

UK Aug public sector net borrowing increased by +10.9 billion pounds, more than expectations of +10.2 billion pounds.

U.S. STOCK PREVIEW

The market is expecting today’s July FHFA house price index to rise by +0.4% m/m, matching the +0.4% m/m rise seen in June. The market is expecting today’s Sep Richmond Fed manufacturing index to show a -2 point decline to 10, reversing part of August’s increase of +5 points to 12. The Treasury today will auction $29 billion of 2-year T-notes. There are four of the Russell 1000 companies that report earnings today: CarMax (consensus $0.67), Bed Bath & Beyond (1.14), Copart (0.41), Carnival Corp (1.44).

Equity conferences during the remainder of this week include: Jefferies West Coast Electronic Payments Summit on Tue, UBS Chemicals Conference on Tue, Citi Industrial Conference on Mon-Tue, Capital Link Global Shipping, Marine Services & Offshore Forum on Tue, World LNG Series:Asia Pacific Summit on Tue-Thu, Avondale's Dallas Airlines Day on Wed, and 8th Rocky Mountain Utility Efficiency Exchange on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

CarMax (KMX -1.42%) reported Q2 EPS of 70 cents, better than consensus of 67 cents.

Dresser-Rand (DRC +2.58%) was downgraded to 'Hold' from 'Buy' at KeyBanc.

Clorox (CLX +7.35%) was downgraded to 'Sell' from 'Neutral' at B. Riley.

Bed Bath & Beyond (KMX -0.25%) was downgraded to 'Market Perform' from 'Outperform' at William Blair.

Fluor (FLR -2.46%) was downgraded to 'Market Perform' from 'Outperform' at Wells Fargo.

Cree (CREE -1.92%) was upgraded to 'Equal Weight' from 'Underweight' at Stephens.

Siemens (SIEGY -0.85%) was downgraded to 'Equal Weight' from 'Overweight' at Barclays.

Dick's Sporting Goods (DKS -1.61%) was downgraded to 'Market Perform' from 'Outperform' at William Blair.

Herbalife (HLF -10.31%) rose nearly 3% in after-hours trading after sources close to the matter said that billionaire activist investor Carl Icahn has not sold out of his stake in the company

AEGON (AEG unch) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs.

Ascena Retail (ASNA -2.36%) slumped over 10% in after-hours trading after it reported Q4 adjusted EPS of 13 cents, well below consensus of 18 cents, and then lowered guidance on fiscal 2015 adjusted EPS to 90 cents-$1.00, weaker than consensus of $1.25.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 -0.33%) this morning are down -5.00 points (-0.25%). The S&P 500 index on Monday closed lower: S&P 500 -0.80%, Dow Jones -0.62%, Nasdaq -0.95%. Negative factors included (1) carry-over weakness from a slide in global stocks after China’s finance minister dampened speculation his government will boost economic stimulus when he said that growth in China faces downward pressure and that there won’t be major changes in policy in response to individual economic indicators, (2) the unexpected drop in U.S. Aug existing home sales which fell -1.8% to 5.05 million, weaker than expectations of +1.0% to 5.20 million.

Dec 10-year T-notes (ZNZ14 +0.11%) this morning are up +4 ticks. Dec 10-year T-note futures prices on Monday closed higher. Bullish factors included (1) the unexpected decline in U.S. Aug existing home sales, (2) increased safe-haven demand for T-notes after stocks plunged, and (3) reduced inflation expectations as the 10-year T-note breakeven inflation rate dropped to a 14-1/2 month low. Closes: TYZ4 +9.00, FVZ4 +6.50.

The dollar index (DXY00 -0.37%) this morning is down -0.296 (-0.35%). EUR/USD (^EURUSD) is up +0.0037 (+0.29%) and USD/JPY (^USDJPY) is down-0.38 (-0.35%). The dollar index on Monday posted a new 4-year high and closed higher. Bullish factors included (1) a slide in EUR/USD to a 14-1/4 month low after Eurozone Sep consumer confidence fell more than expected to a 7-month low and after ECB President Draghi told the EU Parliament that the risks surrounding the expected expansion in the Eurozone “are clearly on the downside.” EUR/USD recovered, though, and closed higher after New York Fed President Dudley said that if the dollar “were to strengthen a lot” there would be consequences for economic growth. Closes: Dollar index +0.017 (+0.02%), EUR/USD +0.00194 (+0.15%), USD/JPY -0.199 (-0.18%).

Nov WTI crude oil (CLX14 +0.78%) this morning is up +43 cents (+0.47%) and Nov gasoline (RBX14 +0.95%) is up +0.0091 (+0.37%). Nov crude and gasoline prices on Monday closed lower: CLX4 -0.78 (-0.85%), RBXX4 -0.0369 (-1.46%). Bearish factors included (1) the rally in the dollar index to a fresh 4-year high, (2) Chinese demand concerns after China’s Finance Minister said China’s economic growth faces downward pressure, and (3) U.S. demand concerns after the unexpected decline in U.S. Aug existing home sales.

Disclosure: None