Morning Call For Nov. 18, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 -0.04%) this morning are down -0.07%, although European stocks are up +0.89% after German investor confidence rose more than expected to a 4-month high. Asian stocks closed mixed: Japan +2.18%, Hong Kong -1.13%, China -1.00%, Taiwan -0.28%, Australia-0.24%, Singapore +0.76%, South Korea +0.95%, India -0.05%. Japanese stocks closed higher after Prime Minister Abe suspended a national sales tax increase, called for an early election, and ordered his minsters to start preparing a mew stimulus package. Commodity prices are mixed. Dec crude oil (CLZ14 -0.12%) is up +0.30%. Dec gasoline (RBZ14 -0.31%) is unch. Dec gold (GCZ14 +1.34%) is up +1.48% at a 2-week high after ECB Executive Board member Mersch suggested the ECB could purchase assets including bullion to counter low inflation. Dec copper (HGZ14 -1.33%) is down-1.35%. Agriculture prices are mixed. The dollar index (DXY00 -0.30%) is down -0.34%. EUR/USD (^EURUSD) is up +0.52%. USD/JPY (^USDJPY) is up +0.03% at a 7-year high after Japanese Prime Minister Abe called for an early election and suspended a planned sales-tax increase. Dec T-note prices (ZNZ14 +0.06%) are up +1 tick.

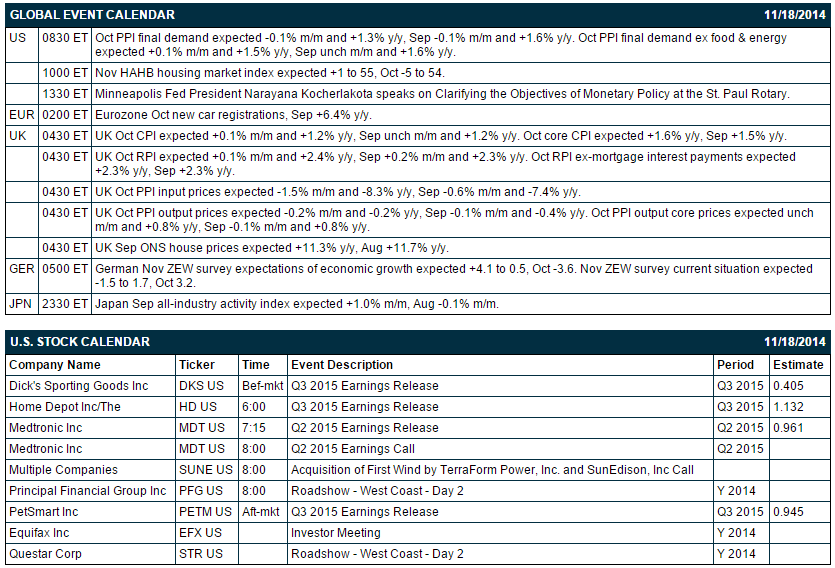

The German Nov ZEW survey expectations of economic growth rose +15.1 to 11.5, better than expectations of +4.1 to 0.5 and the highest in 4 months. The Nov ZEW survey current situation unexpectedly rose +0.1 to 3.3, better than expectations of -1.5 to 1.7.

ECB Executive Board member Mersch said that the ECB could "theoretically" but sovereign debt, gold, exchange-traded funds, and even real estate to counter a longer period of low inflation.

Eurozone Oct new car registrations rose +6.5% y/y, the largest increase in 7 months and the 14th consecutive month that sales have increased.

A research report from the San Francisco Fed said that monetary policy "appears to be far from causing excessive inflation" and price increases are likely to remain slow through the end of 2016 and that it's more probable that inflation will remain below the Fed's 2% inflation target than rise above it.

China Oct home prices fell in 69 of 70 cities tracked by the National Bureau of Statistics, unch from Sep and the most since Jan 2011 when the government changed the way it compiles the data.

UK Oct CPI rose +0.1% m/m, right on expectations, and rose +1.3% y/y, slightly more than expectations of +1.2% y/y. Oct core CPI rose +1.5% y/y, less than expectations of +1.6% y/y and matched the smallest pace of increase in 5-3/4 years.

UK Sep ONS house prices unexpectedly rose +12.1% y/y from a +11.7% y/y increase in Aug, more than expectations of +11.2% y/y and the largest increase in 7 years.

U.S. STOCK PREVIEW

Today’s Oct final-demand PPI index is expected to ease to +1.3% y/y from Sep’s +1.6% y/y and for the core PPI to ease to +1.5% y/y from Sep’s +1.6%. Today's Nov NAHB housing market index is expected to show a +1 point increase to 55, recovering a bit after the sharp -5 point decline to 54 seen in October. There are 5 of the Russell 1000 companies report earnings today: Home Depot (consensus $1.13), Dick's Sporting Goods (0.41), Medtronic (0.96), TJX (0.85), Petsmart (0.95).

Equity conferences today include: Bernstein Energy Efficiency Conference on Tue, FirstEnergys Energy Growth Conference on Tue, Morgan Stanley Global Consumer & Retail Conference on Tue-Wed, Stifel Healthcare Conference on Tue-Wed, UBS Global Technology Conference on Tue-Wed, Los Angeles Auto Show-Press & Trade Days on Tue-Thu, Citi Financial Technology Conference on Wed, Jefferies Global Healthcare Conference on Wed, World Internet Conference on Wed, Keefe, Bruyette, & Woods Securities Brokerage & Market Structure Conference on Wed, Vertical Research Partners Paper and Packaging Conference on Wed, Barclays Global Automotive Conference on Wed-Thu, Citigroup Global Financial Conference on Wed-Thu, Goldman Sachs Global Metals & Mining/Steel Conference on Thu, Wells Fargo Securities E-Cig Conference on Thu, Morgan Stanley European Technology, Media & Telecoms Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Macy's (M -0.71%) was downgraded to 'Neutral' from 'Buy' at BofA/Merrill Lynch.

JA Solar (JASO +0.91%) reported Q3 EPS of 21 cents, higher than consensus of 18 cents.

Sony (SNE -1.84%) was upgraded to 'Buy' from 'Hold' at Deutsche Bank.

Wells Fargo (WFC +0.17%) was downgraded to 'Market Perform' from 'Outperform' at BMO Capital.

Discovery (DISCA -2.98%) was upgraded to 'Neutral' from 'Sell' at Citigroup.

Manitowoc (MTW -2.03%) was upgraded to 'Buy' from 'Hold' at Jefferies.

Home Depot (HD -0.21%) reported Q3 EPS of $1.15, better than consensus of $1.13.

Gabelli reported a 6.52% stake in Chiquita Brands (CQB +0.14%) .

Point72 reported a 5.1% passive stake in RCS Capital (RCAP +0.83%) .

Agilent (A -0.79%) reported Q4 EPS of 88 cents, less than consensus of 89 cents.

Urban Outfitters (URBN -0.06%) fell over 5% in after-hours trading after it reported Q3 EPS of 35 cents, below consensus of 41 cents.

Glenview Capital reported a 5.53% passive stake in Teradyne (TER -1.52%) .

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 -0.04%) this morning are down -1.50 points (-0.07%). The S&P 500 index on Monday opened lower but rallied back and settled little changed: S&P 500 +0.07%, Dow Jones +0.07%, Nasdaq -0.27%. Bearish factors included (1) global growth concerns after Japan Q3 GDP unexpectedly contracted for a second quarter, which puts Japan into recession, and (2) the unexpected -0.1% decline in U.S. Oct industrial production, weaker than expectations of +0.2%. Stocks recovered on increased M&A activity after Halliburton agreed to acquire Baker Hughes for $34.6 billion and Actavis Plc reached a deal to buy Allergan for $66 billion.

Dec 10-year T-notes (ZNZ14 +0.06%) this morning are up +1 tick. Dec 10-year T-note futures prices on Monday erased early gains and closed lower: TYZ4 -7.00, FVZ4 -3.25. Bearish factors included (1) the rebound in stocks which recovered from early losses and reduced the safe-haven demand for Treasuries, and (2) speculation the Fed will still raise interest rates next year despite uneven U.S. economic data and a slowdown in the global economy.

The dollar index (DXY00 -0.30%) this morning is down -0.298 (-0.34%). EUR/USD (^EURUSD) is up +0.0065 (+0.52%). USD/JPY (^USDJPY) is up +0.03 (+0.03%). The dollar index on Monday rebounded from a 1-week low and closed higher. Closes: Dollar index +0.401 (+0.46%), EUR/USD +0.00492 (+0.39%), USD/JPY +0.503 (+0.43%). Bullish factors included (1) weakness in the yen as USD/JPY soared to a new 7-year high after Japan Q3 unexpectedly contacted for a second quarter and put Japan into recession, and (2) weakness in EUR/USD which fell back from a 2-week high and closed lower after ECB President Draghi said the Eurozone economic outlook is "increasingly sobering."

Dec WTI crude oil (CLZ14 -0.12%) this morning is up +23 cents (+0.30%) and Dec gasoline (RBZ14 -0.31%) is unch. Dec crude and Dec gasoline on Monday closed lower. Closes: CLZ4 -0.18 (-0.24%), RBZ4 -0.0162 (-0.79%). Negative factors included (1) Japanese demand concerns after Japan Q3 GDP unexpectedly contracted for a second quarter, which puts Japan, the world's third-largest oil consumer, into recession, (2) the unexpected decline in U.S. Oct industrial production, and (3) a recovery in the dollar after the dollar index rebounded from a 1-week low and closed higher.

Disclosure: None