Morning Call For May 28, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 -0.14%) this morning are down -0.13% and European stocks are down -0.56% after G-7 finance ministers meeting in Dresden, Germany said that Greece needs to get serious about striking a deal on rescue aid. German Finance Minister Schaeuble rebuffed Greece's claim that a deal is imminent when he said "negotiations between the ECB, European Commission, IMF and the Greek government still haven't come very far." Asian stocks closed mixed: Japan +0.39%, Hong Kong -2.23%, China -6.50%, Taiwan +0.20%, Australia -0.21%, Singapore -0.21%, South Korea -0.04%, India -0.21%. Japan's Nikkei Stock Index climbed to a fresh 15-year high as exporters rallied on a weak yen which tumbled to a 12-1/3 year low against the dollar. China's Shanghai Composite Stock Index plunged 6.5% after some Chinese brokerages increased their margin requirements. Another negative for Chinese stocks was the action by the PBOC to drain tens of billions of yuan from the financial system by selling repurchase agreements to targeted financial institutions, which signals the PBOC does not intend to cut interest rates further in the near-term.

Commodity prices are mixed. Jul crude oil (CLN15 -0.12%) is up +0.30% and Jul gasoline (RBN15 +0.69%) is up +0.85%. Metals prices are mixed. Jun gold (GCM15 +0.10%) is up +0.13 and Jul copper (HGN15 -0.02%) is down -0.02%. Agricultural prices are higher.

The dollar index (DXY00 +0.04%) is down -0.17%. EUR/USD (^EURUSD) is up +0.17%. USD/JPY (^USDJPY) is up +0.39% at a 12-1/3 year high.

Jun T-note prices (ZNM15 unch) are unchanged.

San Francisco Fed President Williams said he "expects the Fed will be raising rates later this year" and that he sees above trend growth for the rest of the year with full-year GDP growth probably about 2.0%. He added that he sees interest rates "moving up in 2015, '16 and '17 and coming close to long-run estimates, which are between 3.5% and 4.0%."

U.S. STOCK PREVIEW

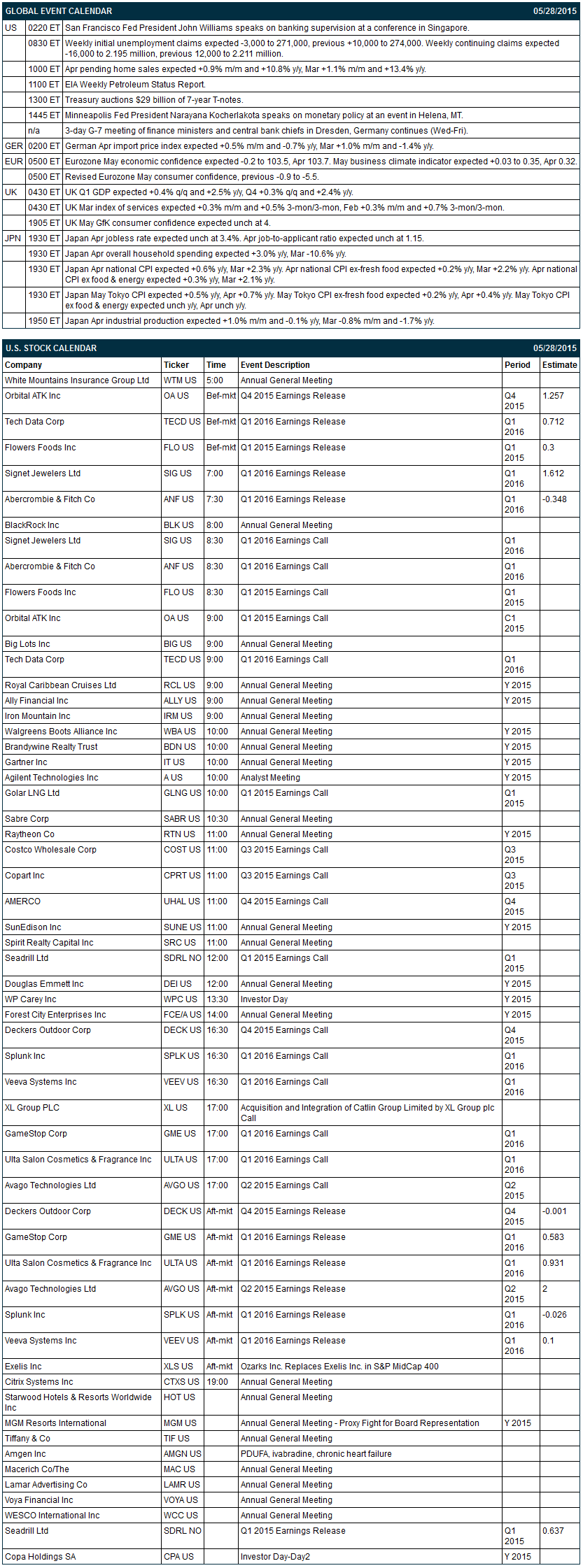

Key U.S. reports today include: (1) weekly initial unemployment claims (expected -3,000 to 271,000 after last week's +10,000 to 274,000) and continuing claims (expected -16,000 to 2.195 million after last week's -12,000 to 2.211 million), (2) Apr pending home sales (expected +0.9% m/m and +10.8% y/y after March's +1.1% m/m and +13.4% y/y), (3) the Treasury's auction of $29 billion of 7-year T-notes, (4) a speech by San Francisco Fed President John Williams on banking supervision at a conference in Singapore, (5) a speech by Minneapolis Fed President Narayana Kocherlakota on monetary policy at an event in Helena, MT, and (6) the second day of the 3-day G-7 meeting in Dresden, Germany.

There are 12 of the Russell 1000 companies that report earnings today with notable reports including: Abercrombie (Consensus -$0.35), Signet Jewelers (1.61), GameStop (0.58), Ulta Salon (0.93), Avago Technologies (2.00), Seadrill (0.64).

U.S. IPO's scheduled to price today include: KNOT Offshore Partners (KNOP), Celadon Group (CGI).

Equity conferences during the remainder of this week include: Citi Global Consumer Conference on Wed-Thu, Cowen and Company Technology Media & Telecom Conference on Wed-Thu, US Ethane & LPG Export Asia 2015 on Wed-Thu, Sanford C. Bernstein Strategic Decisions Conference on Wed-Fri, KeyBanc Capital Markets Industrial, Automotive & Transportation Conference on Thu, American Society of Clinical Oncology Meeting on Fri.

OVERNIGHT U.S. STOCK MOVERS

Flowers Foods (FLO +0.65%) reported Q1 EPS of 29 cents, below consensus of 30 cents.

Chipotle (CMG -1.55%) was upgraded to 'Buy' from 'Hold' at Miller Tabak who raised their price target on the stock to $725 from $715.

The Fresh Market (TFM +0.09%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Genworth (GNW +1.31%) was upgraded to 'Equal Weight' from 'Underweight' at Morgan Stanley.

Molson Coors (TAP -0.92%) was upgraded to 'Overweight' from 'Equal Weight' at Morgan Stanley.

Tech Data (TECD +2.31%) reported Q1 non-GAAP EPS of 80 cents, higher than consensus of 71 cents.

Avago Technologies Ltd. (AVGO +7.76%) reported Q2 EPS of $2.13, better than consensus of $2.00.

Actavis (ACT +2.24%) announced that its VIBERZI drug was approved by the FDA as a twice-daily, oral treatment for adults suffering from irritable bowel syndrome with diarrhea.

Transocean (RIG -0.05%) reports that CFO Esa Ikaheimonen is stepping down as Executive Vice President and CFO effective immediately.

Amerco (UHAL +0.16%) reported Q4 EPS of $2.43, below consensus of $2.48.

RetailMeNot (SALE -0.73%) was initiated with a 'Buy' at Topeka with a price target of $28.

Aegean Marine (ANW +0.58%) reported Q1 EPS of 25 cents, higher than consensus of 24 cents, although the company said Q1 revenue was $1.02 billion, below consensus of $1.37 billion "due to the drop in the price of oil."

Rally Software (RALY -1.03%) surged over 40% in after-hours trading after CA Technologies ({=CA agreed to acquire the company for $19.50 per share or about $480 million.

EnerSys (ENS +2.23%) reported Q4 EPS ex-items of $1.15, better than consensus of $1.14, but Q4 revenue of $629.9 million was below consensus of $635.06 million.

Pier 1 Imports (PIR -2.23%) was initiated with a 'Buy' at Cantor with a price target of $17.

SpartanNash (SPTN +0.06%) reported Q1 EPS of 44 cents, better than consensus of 41 cents, although Q1 revenue of $2.31 billion was below consensus of $2.32 billion.

MARKET COMMENTS

June E-mini S&Ps (ESM15 -0.14%) this morning are down -2.75 points (-0.13%). Wednesday's closes: S&P 500 +0.92%, Dow Jones +0.67%, Nasdaq +1.63%. The S&P 500 on Wednesday closed higher on some Greek optimism and on carry-over support from a rally in Asian stock markets after Japan's Nikkei Stock Index climbed to a 15-year high and China's Shanghai Composite rose to a 7-1/3 year high.

June 10-year T-notes (ZNM15 unch) this morning are unch. Wednesday's closes: TYM5 -0.50, FVM5 -0.75. Jun T-notes on Wednesday closed slightly lower on reduced safe-haven demand as Greek default concerns eased a bit. T-notes also fell on supply pressures as the Treasury auctions $103 billion of T-notes this week.

The dollar index (DXY00 +0.04%) this morning is down -0.168 (-0.17%). EUR/USD (^EURUSD) is up +0.0019 (+0.17%). USD/JPY (^USDJPY) is up +0.48 (+0.39%) at a 12-1/3 year high. Wednesday's closes: Dollar Index +0.072 (+0.07%), EUR/USD +0.00317 (+0.29%), USD/JPY +0.551 (+0.45%). The dollar index on Wednesday posted a 1-month high on (1) Richmond Fed President Lacker's comment that there are risks for the Fed moving too late on interest rates, and (2) technical buying with USD/JPY posting a 7-3/4 year high. EUR/USD recovered from a 1-month low on speculation Greece was moving closer to a deal with its creditors.

July WTI crude oil (CLN15 -0.12%) this morning is up 17 cents (+0.30%). July gasoline (RBN15 +0.69%) is up +0.0165 (+0.85%). Wednesday's closes: CLN5 -0.52 (-0.90%), RBN5 -0.0334 (-1.68%). Jul crude and gasoline on Wednesday closed lower with Jul gasoline at a 1-month low due to the rally in the dollar index to a 1-month high and on plans by Iraq, the second-biggest producer in OPEC, to increase its crude exports in Jun by +800,000 bpd to 3.75 million bpd. Crude oil saw some support from expectations that Thursday's weekly EIA data will show that crude inventories fell -2.0 million bbl for the fourth consecutive weekly decline.

Click on picture to enlarge

Disclosure: None.