Morning Call For May 15, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 +0.12%) this morning are up +0.12% at a new record high and European stocks are up +0.41% as a rally in global bond markets gives stocks a boost. Roche Holding AG is up nearly 3% in pre-market trading after a study showed its experimental immunotherapy for lung cancer doubled the likelihood of survival in some patients, and United Parcel Service climbed 1% in pre-market trading after Goldman Sachs upgraded the stock to 'Buy' from 'Hold.' Asian stocks closed mixed: Japan +0.83%, Hong Kong +1.96%, China -1.59%, Taiwan -0.33%, Australia +0.68%, Singapore +0.21%, South Korea -0.89%, India +0.43%. Japanese stocks settled higher after the yen weakened on expectations the BOJ may further expand stimulus on deflation concerns when Japan Apr producer prices fell -2.1% y/y, the most in 2-3/4 years.

Commodity prices are mostly lower. Jun crude oil (CLM15 -0.43%) is -0.52% and Jun gasoline (RBM15 -0.64%) is down -0.59%. Metals prices are weaker. Jun gold (GCM15 -0.88%) is down -0.91%. Jul copper (HGN15 -0.80%) is down -0.94%. Copper prices retreated despite signs of smaller Chinese supplies after weekly Shanghai copper inventories fell -10,147 MT to a 2-3/4 month low. Agriculture prices are higher.

The dollar index (DXY00 +0.35%) is up +0.37%. EUR/USD (^EURUSD) is down -0.43% after ECB President Draghi said Thursday that the ECB's QE program will be carried out "in full." USD/JPY (^USDJPY) is up +0.55%.

Jun T-note prices (ZNM15 +0.12%) are up +7.5 ticks.

The PBOC has asked the IMF to include the Chinese yuan in its reserve basket of currencies, which now include the dollar, euro, yen and pound. PBOC Governor Zhou Xiaochuan said last month that China is making the yuan more freely usable in order to be included in the IMF's Special Drawing Rights (SDR) basket, which the IMF will review later this year. The dollar has a 41.9% weighting in the SDR basket, the euro 34.4%, the pound 11.3% and the yen 9.4%. According to HSBC Holdings Plc, the yuan's share in the SDR could be 14%, reflecting the importance of China in global exports. An inclusion of the yuan into the SDR basket could fuel a sharp increase in global diversification into yuan assets.

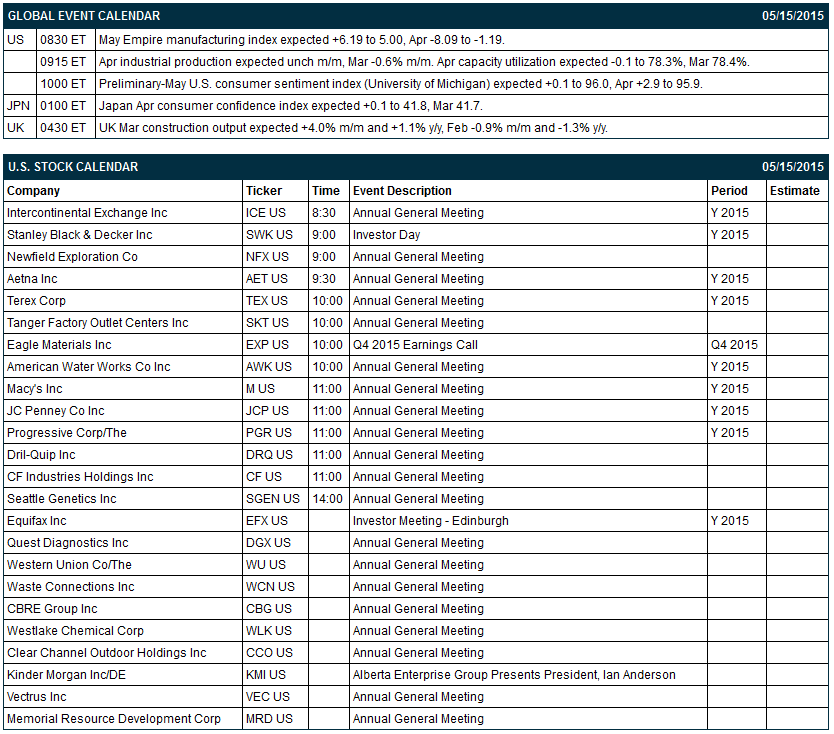

U.S. STOCK PREVIEW

Key U.S. reports today include: (1) April industrial production (expected unch m/m after March's -0.6% m/m), (2) May Empire manufacturing index (expected +6.19 to 5.00 after April's -8.09 to -1.19), and (3) preliminary-May U.S. consumer sentiment index from the University of Michigan (expected +0.1 to 96.0 after April's +2.9 to 95.9).

None of the Russell 100 companies report earnings today.

U.S. IPO's scheduled to price today include: Gelesis (GLSS).

Equity conferences today include: none.

OVERNIGHT U.S. STOCK MOVERS

Yum! Brands (YUM +0.13%) was upgraded to 'Overweight' from 'Neutral' at JPMorgan Chase.

JPMorgan Chase (JPM +0.81%) reported April Net Credit Losses of 2.34% vs. 2.61% last month and April delinquencies of 1.18% vs. 1.23% last month.

Gabelli reported a 7.22% stake in Borderfree (BRDR unch) .

Voya Financial (VOYA +0.33%) was initiated with a 'Conviction Buy' at Goldman Sachs with a price target of $50.

United Parcel Service (UPS +1.25%) climbed 1% in pre-market trading after Goldman Sachs upgraded the stock to 'Buy' from 'Hold.'

Hertz (HTZ +0.20%) reported Q1 revenue of $2.44 billion, below consensus of $2.53 billion.

Darling (DAR +1.00%) reported Q1 adjusted EPS of 9 cents, above consensus of 7 cents.

Dillard's (DDS -1.85%) reported Q1 EPS of $2.66, weaker than consensus of $2.78.

King Digital (KING -4.34%) reported Q1 adjusted EPS of 61 cents, higher than consensus of 53 cents.

Mosaic (MOS +0.31%) rose over 1% in after-hours trading after it announced a new $1.5 billion share repurchase authorization and also increased its dividend to 27.5 cents from 25 cents.

Nordstrom (JWN -2.65%) reported Q1 EPS of 66 cents, weaker than consensus of 71 cents, and then lowered guidance in fiscal 2015 EPS to $3.65-$3.80, at the low end of consensus of $3.79.

Applied Materials (AMAT -0.35%) reported Q2 EPS of 29 cents, above consensus of 28 cents.

Symantec (SYMC +2.29%) reported Q4 adjusted EPS of 43 cents, below consensus of 44 cents, and then lowered guidance on fiscal 2016 EPS to $1.80-$1.90, below consensus of $1.90.

MARKET COMMENTS

June E-mini S&Ps (ESM15 +0.12%) this morning are up +2.50 points (+0.12%) at a record high. Thursday's closes: S&P 500 +1.08%, Dow Jones +1.06%, Nasdaq +1.55%. The S&P 500 on Thursday posted a 2-1/2 week high and closed higher on some strength in the U.S. labor market after weekly jobless claims unexpectedly fell -1,000 to 264,000, better than expectations of +8,000 to 273,000. In addition, the weak April final-demand PPI report of -1.3% y/y indicates a weak inflation picture that may delay a Fed rate hike.

Jun 10-year T-notes (ZNM15 +0.12%) this morning are up +7.5 ticks. Thursday's closes: TYM5 +13.00, FVM5 +8.50. Jun 10-year T-notes on Thursday closed higher on the weak U.S. Apr core final-demand PPI report of +0.8% y/y, the lowest figure since the series started in 2010. In addition, there was some relief buying after the $64 billion quarterly refunding operation concluded.

The dollar index (DXY00 +0.35%) this morning is up +0.345 (+0.37%). EUR/USD (^EURUSD) is down -0.0049 (-0.43%). USD/JPY (^USDJPY) is up +0.66 (+0.55%). Thursday's closes: Dollar Index -0.160 (-0.17%), EUR/USD +0.00552 (+0.49%), USD/JPY +0.019 (+0.02%). The dollar index on Thursday fell to a 3-3/4 month low and closed lower on the weak U.S. April PPI report, which could delay a Fed rate hike. EUR/USD rose to a 2-3/4 month high on reduced Greek default concerns as the 10-year Greek 10-year bond yield fell to a 1-1/2 week low of 10.26% on Greek Finance Minister Varoufakis' claim that his government agrees with its creditors on most issues. However, EUR/USD fell back after ECB President Draghi said the ECB plans to implement its 1.1-trillion euro bond-buying program "in full."

Jun WTI crude oil (CLM15 -0.43%) this morning is down -31 cents (-0.52%) and Jun gasoline (RBM15 -0.64%) is down -0.0121 (-0.59%). Thursday's closes: CLM5 -0.62 (-1.02%), RBM5 +0.0170 (+0.83%). Jun crude oil and gasoline on Thursday settled mixed on the prospects for weaker crude oil demand and reduced gasoline production after Wednesday's EIA report showed the U.S. refinery utilization rate fell sharply by -1.8 points to 91.2%.

Click on picture to enlarge

Disclosure: None.