Morning Call For March 4, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.31%) this morning are down -0.32% ahead of Feb ADP employment data and ahead of the Fed Beige Book, while European stock are up +0.06% after Eurozone Jan retail sales rose more than expected. Gains in European stocks were limited after the Eurozone Feb composite PMI grew less than expected. Asian stocks closed mixed: Japan -0.59%, Hong Kong -0.96%, China +0.65%, Taiwan +0.17%, Australia-0.54%, Singapore -0.19%, South Korea -0.07%, India -0.72%. Commodity prices are mostly lower due to strength in the dollar. Apr crude oil (CLJ15+0.79%) is up +0.49% and Apr gasoline (RBJ15 -1.21%) is down -0.96%. Apr gold (GCJ15 +0.05%) is down -0.08%. May copper (HGK15 +0.30%) is down -0.19%. Agriculture prices are weaker. The dollar index (DXY00 +0.25%) is up +0.30% at a fresh 11-1/3 year high. EUR/USD (^EURUSD) is down-0.40% at a 5-week low. USD/JPY (^USDJPY) is down -0.11%. Jun T-note prices (ZNM15 +0.07%) are down -0.50 of a tick.

Eurozone Jan retail sales rose +1.1% m/m and +3.7% y/y, stronger than expectations of +0.2% m/m and +2.3% y/y with the +3.7% y/y gain the largest annual increase in nearly 9-1/2 years.

The Eurozone Feb Markit composite PMI was revised downward by -0.2 to 53.3 from the originally reported 53.5, but still is the fastest pace of expansion in 7 months.

The German Feb Markit services PMI was revised lower by -0.8 to 54.7 from the originally reported 55.5.

The UK Feb Markit/CIPS services PMI unexpectedly fell -0.5 to 56.7, weaker than expectations of +0.3 to 57.5.

The Reserve Bank of India (RBA) unexpectedly lowered the benchmark repurchase rate by -25 bp to 7.50% with RBA Governor Rajan saying "given low capacity utilization and still-weak indicators of production and credit off-take, it is appropriate for the RBA to be pre-emptive in its policy action to utilize available space for monetary accommodation."

U.S. STOCK PREVIEW

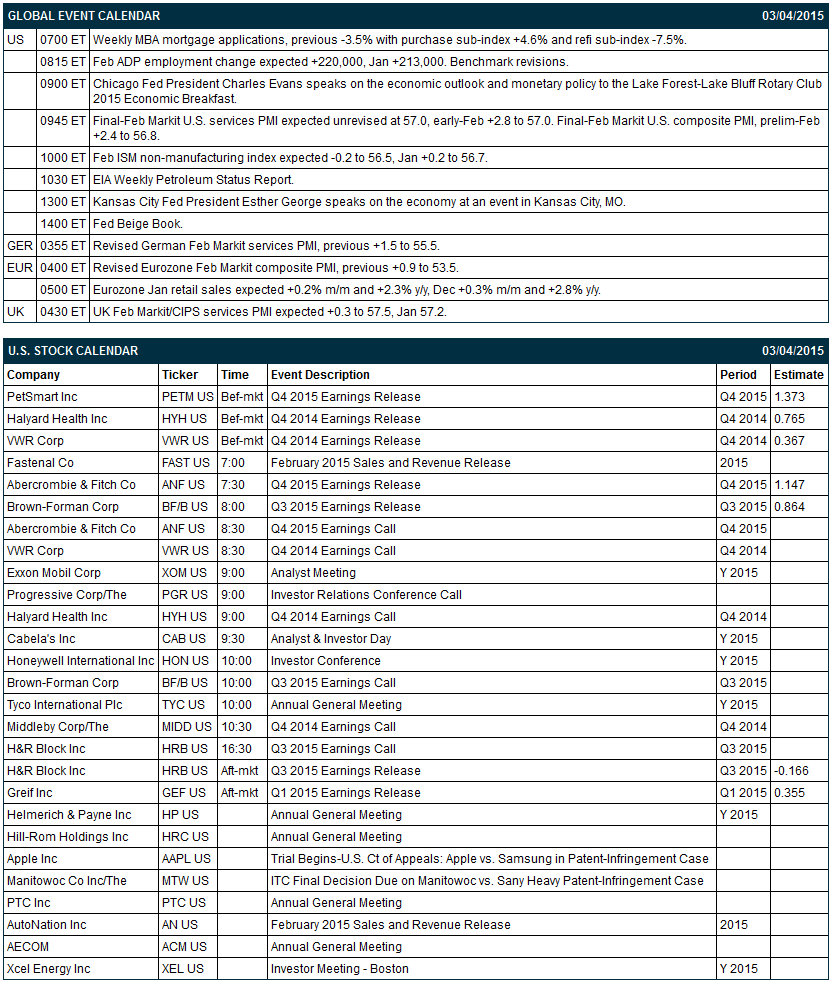

Today’s Feb ADP employment report is expected to show a respectable increase of +220,000, stronger than the +213,000 increase seen in January. Today’s Feb ISM non-manufacturing index is expected to show a small -0.2 decline to 56.5, thus reversing January’s small +0.2 point increase to 56.7. The Fed today will release its Beige Book report ahead of the March 17-18 FOMC meeting. There are 3 of the S&P 500 companies that report earnings today: H&R Block (consensus $-0.17), Brown-Forman (0.86), PetSmart (1.37).

Equity conferences during the remainder of this week include: Cowen & Co. Health Care Conference on Mon-Wed, Citigroup Global Property CEO Conference on Mon-Wed, Raymond James & Associates Institutional Investors Conference on Mon-Wed, Morgan Stanley Technology Media & Telecom Conference on Mon-Thu, Bank of America Merrill Lynch Consumer & Retail Conference on Tue-Wed, J.P. Morgan Aviation, Transportation and Industrials Conference on Tue-Thu, Mitsubishi UFJ Securities 3rd Annual Seattle Consumer Conference on Wed, Morgan Stanley European MedTech & Services Conference on Wed, Simmons Energy Conference on Wed, UBS Natural Gas, Electric Power and MLP Conference on Wed, UBS Utilities and Natural Gas Conference on Wed, UBS Global Consumer Conference on Wed-Thu, Bank of America Merrill Lynch Refining Conference on Thu, Barclays Investment Grade Energy & Pipeline Conference on Thu, Pacific Crest Emerging Technology Summit on Thu, Morgan Stanley MLP/Diversified Natural Gas, Utilities Clean Tech Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Alcoa (AA +1.54%) and Century Aluminum (CENX -1.44%) were both downgraded to 'Neutral' from 'Buy' at BofA/Merrill Lynch.

Dick's Sporting Goods (DKS +1.05%) was downgraded to 'Hold' from 'Buy' at Needham.

Best Buy (BBY +1.42%) was upgraded to 'Neutral' from 'Underperform' at Wedbush.

Halyard Health (HYH -0.92%) reported Q4 adjusted EPS of $1.59, well above consensus of 77 cents.

Trina Solar (TSL +1.19%) reported Q4 EPS of 13 cents, right on consensus, although Q4 revenue of $705.04 million was higher than consensus of $642.88 million.

AutoZone (AZO +0.36%) was upgraded to 'Neutral' from 'Underperform' at Sterne Agee.

VWR (VWR -0.76%) reported Q4 adjusted EPS of 43 cents, higher than consensus of 37 cents.

McDonald's (MCD -0.26%) was upgraded to 'Outperform' from 'Sector Perform' at RBC Capital.

ABM Industries (ABM -0.16%) reported Q1 adjusted EPS of 38 cents, better than consensus of 34 cents, and then raised guidacne on fiscal 2015 adjusted EPS view to $1.75-$1.85, above consensus of $1.75.

Air France-KLM (AFLYY +0.91%) was downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Cascade Investment reported a 7.9% stake in Strategic Hotels (BEE -1.82%) .

Engility Holdings (EGL -1.40%) reported Q4 adjusted EPS of 67 cents, less than consensus of 69 cents.

Bob Evans (BOBE +0.27%) plunged over 15% in after-hours trading after it reported Q3 EPS of 60 cents, below consensus of 70 cents, and then lowered guidance on fiscal 2015 EPS view to $1.40-$1.60 from $1.90 to $2.10, weaker than consensus of $1.97.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.31%) this morning are down -6.75 points (-0.32%). The S&P 500 index on Tuesday slipped to a 1-week low and closed lower: S&P 500 -0.45%, Dow Jones -0.47%, Nasdaq -0.54%. Bearish factors included (1) weakness in automakers after Feb auto sales came in below expectations, (2) a sell-off in transportation stocks after railroad companies tumbled, and (3) weakness in healthcare stocks as biotechnology companies slumped after their recent run up.

Jun 10-year T-notes (ZNM15 +0.07%) this morning are down -0.50 of a tick. Jun 10-year T-note futures prices on Tuesday fell to a 1-week low and closed lower. Closes: TYM5 -10.00, FVM5 -6.00. The main bearish factor was an increase in corporate supply after Activis Plc launched a $21 billion debt sale, which prompted bond dealers to hedge their purchases by selling long-term Treasuries. Losses were limited after a slide in the S&P 500 to a 1-week low boosted the safe-haven demand for T-notes.

The dollar index (DXY00 +0.25%) this morning is up +0.285 (+0.30%) at a fresh 11-1/3 year high. EUR/USD (^EURUSD) is down -0.0045 (-0.40%) at a 5-week low. USD/JPY (^USDJPY) is down -0.13 (-0.11%). The dollar index on Tuesday posted a 11-1/3 year high but shed its advance and closed lower: Dollar index -0.079 (-0.08%), EUR/USD -0.00077 (-0.07%), USD/JPY -0.402 (-0.33%). Bearish factors included (1) a rally in USD/JPY after a slide in stocks boosted safe-haven demand for the yen, and (2) the +2.9% m/m increase in German Jan retail sales, the largest monthly increase in 7 years which was supportive for EUR/USD.

Apr WTI crude oil (CLJ15 +0.79%) this morning is up +25 cents (+0.49%) and Apr gasoline (RBJ15 -1.21%) is down -0.0188 (-0.96%). Apr crude and Apr gasoline prices on Tuesday closed higher: CLJ5 +0.93 (+1.88%), RBJ5 +0.0427 (+2.25%). Bullish factors included (1) a weaker dollar, and (2) expectations for Wednesday’s EIA data to show gasoline inventories fell -1.75 million bbl and distillate stockpiles declined -2.0 million bbl. Gains in crude were muted on expectations that Wednesday’s EIA data will show crude supplies rose +4.0 million bbl to the highest since EIA data began in 1982.

Click on picture to enlarge

Disclosure: None.