Morning Call For March 25, 2015

June E-mini S&Ps (ESM15 -0.06%) this morning are up +0.08% on increased M&A activity as Kraft Foods jumped 16% in early pre-market trading on news that it will merge with H.J. Heinz. European stocks are down -0.51% on Greek default concerns after the ECB banned Greek banks from increasing holdings of short-term government debt. The ECB has rationed the Greek central bank's access to emergency funding since last month on concern the Greek government is funding itself via domestic lenders with central bank cash. Eurozone finance officials will hold a call today to discuss progress on Greece, amid concerns that it may run out of cash by early next month. Losses in European stocks were limited after German business confidence rose for a fifth month in March to the highest in 8 months. Asian stocks closed mixed: Japan +0.17%, Hong Kong +0.53%, China -0.82%, Taiwan -0.66%, Australia +0.07%, Singapore +0.17%, South Korea -0.08%, India -0.18%. Commodity prices are mixed. May crude oil (CLK15 -0.29%) is down -0.13% and May gasoline (RBK15 +0.46%) is up +0.50%. Apr gold (GCJ15 +0.19%) is up +0.07%. May copper (HGK15 -0.59%) is down -0.62%. Agriculture prices are mixed. The dollar index (DXY00 -0.42%) is down -0.30%. EUR/USD (^EURUSD) is up +0.52%. USD/JPY (^USDJPY) is down -0.14%. Jun T-note prices (ZNM15 +0.15%) are up +3 ticks at a 1-1/2 month high after Chicago Fed President said inflation is too low to raise interest rates this year.

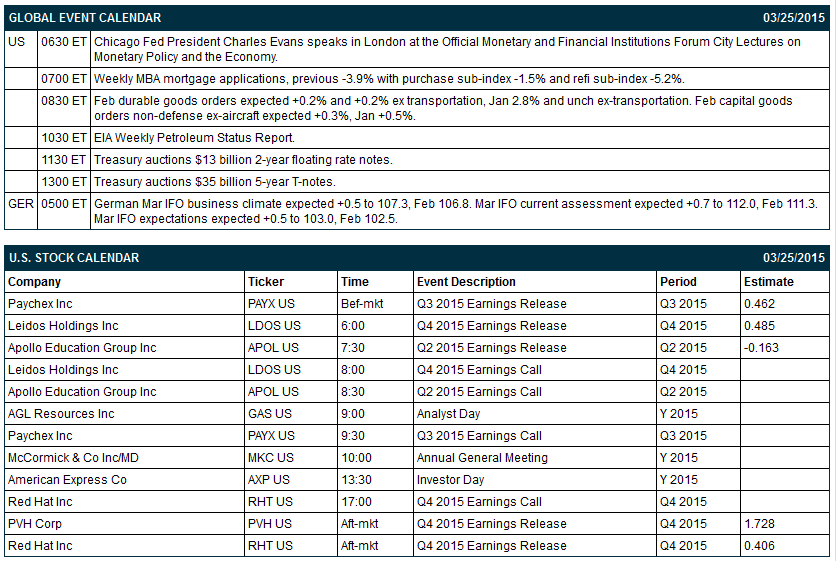

The German Mar IFO business climate rose +1.1 points to 107.9, stronger than expectations of +0.5 to 107.3 and the highest in 8 months. The Mar IFO current assessment rose +0.7 to 112.0, right on expectations. The Mar IFO expectations rose +1.4 points to 103.9, stronger than expectations of +0.5 to 103.0 and the highest in 9 months.

Chicago Fed President Evans said inflation remains too low to justify an interest rate increase this year, despite "terrific" progress in reducing U.S. unemployment. Evans said "he sees no compelling reason for us to be in a hurry to tighten financial conditions until" it's clear that inflation will reach the Fed's 2.0% target within one or two years.

Japan Feb PPI services prices rose +3.3% y/y, right on expectations.

U.S. STOCK PREVIEW

Today’s Feb durable goods orders report is expected to show an increase of +0.2% for both the headline and ex-transportation reports. The Treasury today will sell $13 billion of 2-year floating-rate notes and $35 billion of 5-year T-notes. There are 5 of the Russell 1000 companies that report earnings today: Paychex (consensus $0.46), Red Hat (0.41), PVH (1.73), Leidos Holdings (0.49), Apollo Education (-0.16).

Equity conferences during the remainder of this week include: Excellence in Data Analytics for Shared Services and Outsourcing 2015 on Tue-Wed, Telsey Advisory Group (TAG) Spring Consumer Conference on Tue-Wed, Leerink Booth Tours At American Academy of Orthopaedic Surgeons on Wed-Thu, CIBC Real Estate Conference on Thu, Nomura - Conference: Global Chemicals Industry Leaders Conference - London on Thu, Jefferies Animal Health Summit on Thu, Gabelli Specialty Chemicals Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Kraft Foods Group (KRFT -1.27%) surged 16% in pre-market trading after saying it will merge with H.J. Heinz.

Starwood (HOT -2.28%) was downgraded to 'Neutral' from 'Buy' at SunTrust.

Tesla (TSLA +1.05%) was downgraded to 'Underperform' from 'Outperform' at CLSA.

Finish Line (FINL +0.41%) was downgraded to 'Neutral' from 'Buy' at B. Riley.

Leidos (LDOS -2.20%) reported Q4 EPS of 69 cents, higher than consensus of 48 cents, but then lowered guidance on fiscal 2015 EPS to $2.20-$2.45, below consensus of $2.53.

Merck (MRK -0.17%) announced a new $10 billion share repurchase program.

ING Groep (ING +1.20%) was downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Ultragenyx (RARE -2.65%) was initiated with a 'Buy' at CRT Capital with a price target of $90.

Cepheid (CPHD -2.08%) announced it has received Emergency Use Authorization from the FDA for Xpert Ebola, a molecular diagnostic test for Ebola Zaire Virus that delivers results in less than two hours.

Wells Fargo initiated United Rentals (URI +0.25%) with an 'Outperform' rating and a $110-$115 valuation range.

Steelcase (SCS -2.16%) reported Q4 adjusted EPS of 21 cents, better than consensus of 20 cents.

Park City Group (PCYG +0.57%) filed to sell 1 million shares of common stock.

MARKET COMMENTS

Jun E-mini S&Ps (ESM15 -0.06%) this morning areup +1.75 points (+0.08%) . Tuesday's Closes: S&P 500 -0.61%, Dow Jones -0.58%, Nasdaq -0.33%. The stock market on Tuesday closed lower after the stronger-than-expected U.S. Feb new home sales report (+7.8% to a 7-year high of 539,000) bolstered concern the Fed would soon raise interest rates. Another negative for stocks was the comments from St. Louis Fed President Bullard who said the Fed risks falling "behind the curve" on inflation if normalization of monetary policy is not started soon.

Jun 10-year T-notes (ZNM15 +0.15%) this morning are up +3 ticks at a new 1-1/2 month high. Tuesday's Closes: TYM5 +8.00, FVM5 +5.50. Jun T-notes posted a 1-1/2 month high on benign inflation pressures after U.S. Feb core CPI rose +1.7% y/y, right on expectations and below the Fed's 2.0% inflation target. T-notes received additional support in late afternoon after stocks sold-off.

The dollar index (DXY00 -0.42%) this morning is down -0.289 (-0.30%). EUR/USD (^EURUSD) is up +0.0057 (+0.52%). USD/JPY (^USDJPY) is down -0.17 (-0.14%). Tuesday's closes: Dollar index +0.160 (+0.16%), EUR/USD -0.00212 (-0.19%), USD/JPY +0.025 (+0.02%). The dollar rebounded from a 2-week low and closed higher after U.S. Feb new home sales rose more than expected to the highest in 7 years, which bolsters expectations for the Fed to raise interest rates.

May WTI crude oil (CLK15 -0.29%) this morning is down -6 cents (-0.13%) and May gasoline (RBK15 +0.46%) is up +0.0090 (+0.50%). Tuesday's closes: CLK5 +0.06 (+0.13), RBK5 -0.0013 (-0.07%). May crude and gasoline posted 1-week highs but settled mixed after the dollar recovered from a 2-week low and closed higher. Gains in crude were limited on expectations that Wednesday's weekly EIA crude inventories will increase by +4.75 million bbl.

Click on picture to enlarge

Disclosure: None.