Morning Call For March 12, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.21%) this morning are up +0.28% led by a rally in U.S. bank stocks after 29 banks passed stress tests Wednesday and several lenders boosted their share buyback programs. European stocks are down -0.05% after Eurozone Jan industrial production unexpectedly declined. Yields on European government bonds fell to record lows, with the yield on Germany's 10-year bund sliding to an all-time low of 0.186%, after ECB Executive Board member Coeure said the ECB has bought 9.8 billion-euros of assets during the first three days of its QE program with an average maturity of 9 years. Asian stocks closed mostly higher: Japan +1.43%, Hong Kong +0.34%, China +1.93%, Taiwan +0.76%, Australia +0.98%, Singapore -0.15%, South Korea -0.75%, India +0.95%. Japan's Nikkei Stock Index rose to the highest in 14-3/4 years, led by strength in exporters, as the yen held near a 7-1/2 year low against the dollar. China’s Shanghai Stock Index climbed to a 6-week high on signs that monetary easing is spurring demand for loans after data showed China Feb aggregate financing, China's broadest measure of new credit, rose more than expected. Commodity prices are mostly higher. Apr crude oil (CLJ15 +0.91%) is up +0.50%. Apr gasoline (RBJ15 +1.45%) is up +1.16%. Apr gold (GCJ15 +0.73%) is up +0.82%. May copper (HGK15 +2.84%) is up +2.57%. Agriculture prices are mostly higher. The dollar index (DXY00 -0.77%) is down -0.66%. EUR/USD (^EURUSD) is up +0.62%. USD/JPY (^USDJPY) is down -0.31%. Jun T-note prices (ZNM15 +0.22%) are up +11 ticks.

China Feb new yuan loans were 1.020 trillion yuan, more than expectations of 1.000 trillion yuan, Feb aggregate financing, China's broadest measure of new credit, was 1.35 trillion yuan ($215.5 billion), above expectations of 1.00 trillion yuan.

ECB Executive Board member Coeure said the ECB has bought 9.8 billion-euros of assets during the first three days of its QE program with an average maturity of 9 years, which is "very important" because it will affect the yield curve. He also said the ECB's QE program could go beyond Sep 2016 "if needed."

Eurozone Jan industrial production unexpectedly fell -0.1% m/m, weaker than expectations of +0.2% m/m. On an annual basis, Jan industrial production rose +1.2% y/y, stronger than expectations of +0.1% y/y.

The Japan Feb consumer confidence index rose +1.6 to 40.7, stronger than expectations of +0.4 to 39.5 and the highest in 6 months.

The Japan Q1 BSI all-industry business conditions was 1.9, weaker than expectations of 6.0 and the lowest since Q1 of 2013. The Q1 BSI large manufacturing business conditions fell to 2.4 from 8.1 in Q4.

The Japan Jan tertiary industry index rose +1.4% m/m, stronger than expectations of +0.5% m/m and the largest increase in 10 months.

U.S. STOCK PREVIEW

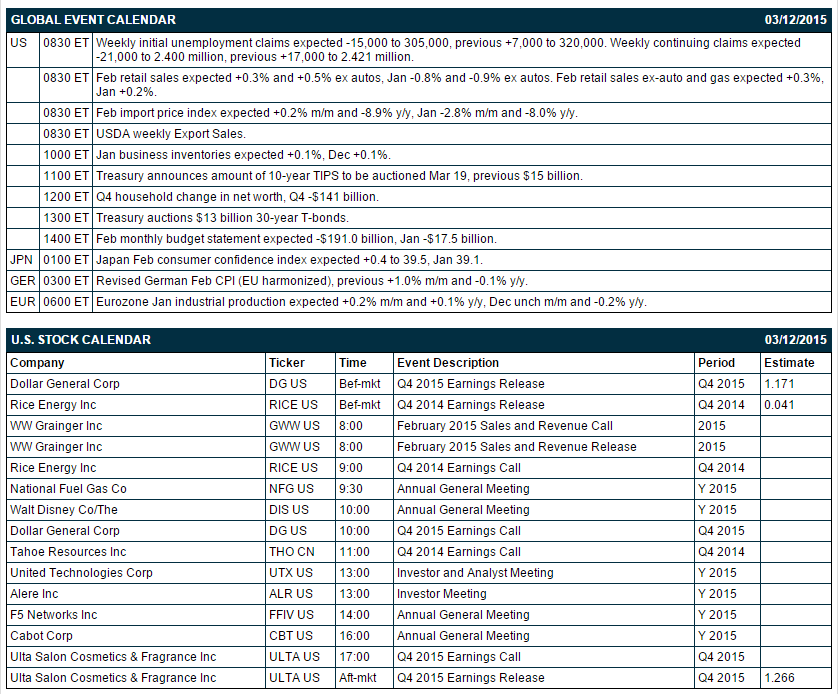

Today’s Feb retail sales report is expected to show a fairly strong +0.5% increase ex-autos but increases of only +0.3% for both the headline report and the ex-gasoline report. Today's initial unemployment claims report is expected to show a decline of -15,000 while continuing claims are expected to show a decline of -21,000. Today’s Feb import price index is expected to show a small +0.2% m/m rebound after the plunge of -2.8% m/m seen in January. The Treasury today will sell $13 billion of 30-year T-bonds, concluding this week’s $58 billion coupon package.

There are three of the Russell 1000 companies that report earnings today: Dollar General (consensus $1.17), Rice Energy (0.04), Ulta Salon (1.27). Equity conferences during the remainder of this week include: Barclays Capital Health Care Conference on Tue-Thu, Deutsche Bank Regional Banks Summit on Thu, Nomura - Conference: US Software Conference - New York on Thu.

OVERNIGHT U.S. STOCK MOVERS

Citigroup (C +2.15%) rose 3% in pre-market trading after it announced a $7.8 billion share buyback plan.

Morgan Stanley (MS +0.20%) gained over 2% in pre-market trading after it announced a $3.1 billion share repurchase plan.

Lumber Liquidators (LL +10.65%) lowered guidance on Q1 revenue to $253.6 million-$265.6 million, below consensus of $275.98 million.

The Children's Place (PLCE -0.41%) reported Q4 adjusted EPS of 94 cents, higher than consensus of 93 cents, but then said it sees fiscal 2015 same-store-sales flat to up 1% as it lowered guidance on fiscal 2015 adjusted EPS to $3.15-$3.30, below consensus of $3.41.

Men's Wearhouse (MW +0.33%) rose over 5% in after-hours trading after it reported a Q4 adjusted EPS loss of -3 cents, a smaller loss than consensus of -7 cents.

State Street (STT +1.51%) announced a $1.8 billion share buyback program.

JP Energy (JPEP +2.19%) reported a Q4 EPS loss of -51 cents, weaker than consensus of a 1 cent profit.

JPMorgan Chase (JPM +0.47%) announced a $6.4 billion share repurchase program.

Bank of America (BAC +2.03%) announced a $4 billion share repurchase program.

The Federal Reserve objected to the capital plans of Deutsche Bank Trust Corporation (DB +1.35%) and Banco Santander's (SAN +0.15%) Santander Holdings USA on qualitative concerns.

Scientific Games (SGMS -1.56%) reported a Q4 EPS loss of -55 cents, a smaller loss than consensus of -60 cents.

1-800-Flowers.com (FLWS +2.18%) was initiated with a 'Buy' at B. Riley with a price target of $15.

JetBlue (JBLU +0.94%) reported its traffic in February increased 10.0% from February 2014.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +0.21%) this morning are up +5.75 points (+0.28%). The S&P 500 index on Wednesday slid to a 1-month low and closed lower: S&P 500 -0.19%, Dow Jones -0.16%, Nasdaq -0.55%. Bearish factors included (1) concern about a Chinese economic slowdown after China Feb industrial production rose only +6.8% year-to-date, weaker than expectations of +7.7% and at the slowest pace of increase in 5-3/4 years, and (2) weakness in energy producers after crude oil fell to a 5-week low.

Jun 10-year T-notes (ZNM15 +0.22%) this morning are up +11 ticks. Jun 10-year T-note futures prices on Wednesday closed higher. Closes: TYM5 +2.00, FVM5 -0.25. Bullish factors included (1) carry-over support from a rally in German bund prices to all-time highs, and (2) strong foreign demand for the Treasury’s $21 billion 10-year T-note auction where indirect bidders, a proxy for foreign buyers, bought 58.6% of the notes at auction, way above the 10-auction average of 47.1%.

The dollar index (DXY00 -0.77%) this morning is down -0.663 (-0.66%). EUR/USD (^EURUSD) is up +0.0065 (+0.62%). USD/JPY (^USDJPY) is down-0.38 (-0.31%). The dollar index on Wednesday posted a new 11-1/2 year high and closed higher: Dollar index +1.177 (+1.19%), EUR/USD -0.01504(-1.41%), USD/JPY +0.317 (+0.26%). Bullish factors included (1) weakness in EUR/USD which slid to a new 11-3/4 year low as the ECB bought European government bonds on the third day of its QE program, and (2) heightened Greek default concerns which boosted the safe-haven demand for the dollar after the 10-year Greek bond yield rose to a 1-month high.

Apr WTI crude oil (CLJ15 +0.91%) this morning is up +24 cents (+0.50%) and Apr gasoline (RBJ15 +1.45%) is up +0.0211 (+1.16%). Apr crude oil and gasoline prices on Wednesday settled mixed with Apr crude at a 5-week low and Apr gasoline at a 2-1/2 week low: CLJ5 -0.12 (-0.25), RBJ5 +0.0081 (+0.45%). Bearish factors included (1) continued strength in the dollar as the dollar index rose to a new 11-1/2 year high, and (2) the +4.51 million bbl increase in weekly EIA crude inventories to 448.9 million bbl, the highest since EIA data began in 1982. Gasoline recovered its losses and closed higher on supply concerns due to the partial closure of the Houston Ship Channel for a third day because of a crash that has slowed output at 5 refineries with 1.34 million bpd of capacity.

Disclosure: None.