Morning Call For January 2, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.38%) this morning are up +0.30% on dovish comments by ECB President and on slightly stronger-than-expected Chinese PMI figures. The Euro Stoxx 50 index this morning is down -0.29%. Asian stocks today closed higher: Hong Kong +1.07%, Australia +0.46%, Singapore +0.16%, South Korea +0.30%, India +1.38%, Turkey -0.49%. The Japanese, Chinese and Taiwan stock markets remained closed today. The dollar index (DXY00 +0.58%) this morning is up +0.51% at a new high, while EUR/USD (^EURUSD) fell to a new 4-1/2 year low this morning on dovish Draghi comments and is down -0.47%. USD/JPY (^USDJPY) is up +0.67%. Mar 10-year T-note prices (ZNH15 -0.20%) are down -8.5 ticks. Commodity prices are up by an average +0.19% this morning. Feb crude oil (CLG15 -1.86%) is up +0.28% and Feb gasoline (RBG15 -2.05%) is up +0.29%. Feb gold (GCG15 -0.55%) is down -0.17% on the stronger dollar. Mar copper (HGH15 -0.14%) is down -0.09%. Agriculture futures markets have yet to start trading this morning.

ECB President Draghi said in an interview published today that, "The risk that we don't fulfill our mandate of price stability is higher than it was six months ago." He added, "We are in technical preparations to alter the size, speed and composition of our measures at the beginning of 2015, should this become necessary, to react to a too-long period of low inflation. There's unanimity in the ECB council on that." Mr. Draghi's comments support market expectations that the ECB will announce the purchase of sovereign bonds at its next meeting on Jan 22. His comments were bearish for EURUSD this morning and supportive for Eurozone bond prices.

Russian oil production in December rose +0.3% to 10.667 million bpd, according to a division of the Russian Energy Ministry, which was a post-Soviet record high. That indicates that sanctions have not yet slowed down Russian oil production and that Russia is clearly not joining any effort by OPEC to rein in world oil production.

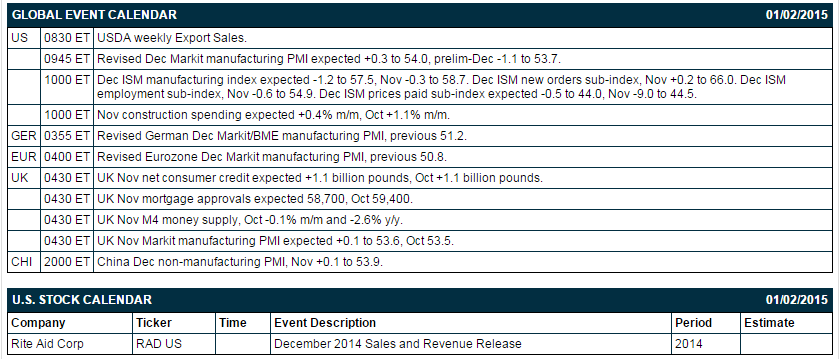

The Markit UK manufacturing PMI fell by -0.8 points to 52.5 from a revised 53.3 in November, which was substantially weaker than market expectations for an increase to 53.6. Moreover, orders and output growth sub-indexes both fell to their second lowest levels in 1-1/2 years. The report provided further evidence of the ongoing slowdown in the UK manufacturing sector.

China's Dec manufacturing PMI on Thursday was reported at -0.2 to 50.1 from 50.3 in November, which was a bit stronger than market expectations of-0.3 to 50.0. This followed Wednesday's news that the final-Dec China manufacturing PMI from HSBC was revised slightly higher by +0.1 to 49.6 from the preliminary figure of 49.5, which was stronger than market expectations for no revision at 49.5. Separately, China's Dec non-manufacturing PMI on Thursday rose +0.2 to 54.1 from 53.9 in Nov.

Germany's Markit final-Dec manufacturing PMI was left unrevised from the prelim-Dec report of 51.2, which was in line with market expectations.

U.S. STOCK PREVIEW

Today’s Dec ISM manufacturing index is expected to show a -1.2 point decline to 57.5, adding to November’s decline of -0.3 to 58.7. None of the Russell 3000 companies report earnings today. There are no equity conferences this week.

Mar E-mini S&Ps (ESH15 +0.38%) this morning are up +6.25 points (+0.30%) on dovish comments by ECB President Draghi, shaking off the weaker-than-expected UK manufacturing PMI report and Thursday's -0.2 point decline to 50.1 in China's manufacturing PMI report. The S&P 500 index on Wednesday slid to a 1-1/2 week low and closed lower: S&P 500 -1.03%, Dow Jones -0.89%, Nasdaq -1.08%. Bearish factors included (1) the +17,000 increase in U.S. weekly jobless claims to a 5-week high of 298,000, more than expectations of +10,000 to 290,000, (2) the -2.5 point decline in the Dec Chicago PMI to 58.3, weaker than expectations of -0.8 to 60.0 and the slowest pace of expansion in 5 months, and (3) a slide in energy producers after crude oil plunged to a 5-1/2 year low.

OVERNIGHT U.S. STOCK MOVERS

- Macau reported that December casino revenue fell -30.4%, affecting companies in the Macau gaming industry such as Las Vegas Sands (LVS-0.56%), MGM Resorts (MGM -0.33%), Melco Crown (MPEL -0.51%) and Wynn Resorts (WYNN -1.61%).

- Signet Jewelers (SIG +0.14%) Kate Spade (KATE +0.13%), and Sally Beauty (ABH) were named as top picks at Sterne Agee.

- LINN Energy (LINE +0.40%) provided its outlook for 2015 and announced a strategic partnership with GSO Capital Partners.

- Main Street Capital reported a 21.4% stake in Glowpoint (GLOW unch) .

- MiMedx (MDXG +3.97%) slid over 10% in after-hours trading after it announced that it has received a subpoena from the Office of Inspector General of the Department of Health and Human Services in connection with a civil investigation.

- Deerhill Management reported a 5.25% passive stake in State Investors Bancorp (SIBC +34.90%) .

- Cormorant Global Healthcare reported a 5.13% passive stake in Ardelyx (ARDX -0.74%).

MARKET COMMENTS

Mar 10-year T-notes (ZNH15 -0.20%) this morning are down -8.5 ticks on reduced safe-haven demand with this morning's higher trade in E-mini S&Ps. Mar 10-year T-note futures prices on Wednesday posted a 1-week high and closed higher: TYH5 +7.00, FVH5 +5.00. Bullish factors included (1) increased safe-haven demand on Greek sovereign debt concerns after the 10-year Greek bond yield rose to a 1-1/2 year high of 9.75%, (2) the larger-than-expected increase in U.S. weekly initial unemployment claims, and (3) stock weakness that boosted safe-haven demand for T-notes.

The dollar index (DXY00 +0.58%) this morning is up +0.460 points (+0.51%) and EUR/USD (^EURUSD) is down -0.0057 (-0.47%) on today's euro-bearish comments by ECB President Draghi supporting expectations the ECB will announce a QE program when it next meets on Jan 22. USD/JPY (^USDJPY) is up +0.80 (+0.67%). The dollar index on Wednesday closed higher. Closes: Dollar index +0.278 (+0.31%), EUR/USD -0.00582 (-0.48%), USD/JPY +0.206 (+0.17%). Bullish factors included (1) weakness in EUR/USD which fell to a 2-1/3 year low after comments from ECB Chief Economist Praet signaled the ECB may be closer to implementing QE when he said the Eurozone could see “negative inflation during a substantial part of 2015” amid a slide in crude prices, and (2) overall bullish momentum for the dollar on speculation the Fed is close to raising interest rates while the ECB and BOJ may ease further.

Feb WTI crude oil this morning is up +0.15 (+0.28%) and Feb gasoline is up +0.0043 (+0.29%) on some short-covering. The markets were able to shake off bearish news that Russia's Dec oil production reached a new record high and that the storage oil tank fire at Libya's Es Sider Port has been extinguished. Feb crude and Feb gasoline prices on Wednesday slumped to 5-1/2 year lows and closed mixed. Closes: CLG5 -0.85 (-1.57%), RBG5 +0.0010 (+0.07%). Bearish factors included (1) the +1.995 million bbl surge in crude oil supplies at Cushing, OK, the delivery point of WTI futures, to a 9-3/4 month high of 30.8 million bbl, and (2) the +2.95 million bbl increase in EIA gasoline stockpiles to a 10-month high of 229 million bbl. Gasoline recovered from its low and closed slightly higher after Phillips 66 reported a process upset at its 146,000 bpd refinery in Borger, TX.

Disclosure: None.