Morning Call For February 9, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.54%) this morning are down -0.60% and European stocks are down -1.59% on Greek sovereign debt concerns after Greek Prime Minister Tsipras on Sunday vowed to negotiate an end to austerity measures, which fuels concern about a confrontation with Greece's international creditors. EU finance ministers will hold an emergency meeting in Brussels on Wednesday with Greek Finance Minister Varoufakis to discuss Greece's financing needs. Also pressuring stocks was an unexpected decline in China Jan exports, which fell by the most in 10 months and heightens concern about a global economic slowdown. Asian stocks closed mostly lower: Japan +0.36%, Hong Kong -0.64%, China +1.01%, Taiwan-0.37%, Australia -0.09%, Singapore -0.39%, South Korea -0.36%, India -1.71%. Despite the largest drop in China Jan imports in 5-1/2 years, Chinese stocks rose on speculation that the government will boost stimulus measures to revive economic growth. Commodity prices are mostly higher. Mar crude oil (CLH15 +1.66%) is up +1.37% and Mar gasoline (RBH15 +1.12%) is up +0.83%. Apr gold (GCJ15 +0.35%) is up +0.53%. Mar copper (HGH15-0.35%) is down -0.04%. Agriculture prices are mixed. The dollar index (DXY00 unch) is down -0.03%. EUR/USD (^EURUSD) is down -0.05%. USD/JPY (^USDJPY) is down -0.54%. Mar T-note prices (ZNH15 +0.17%) are up +7.5 ticks.

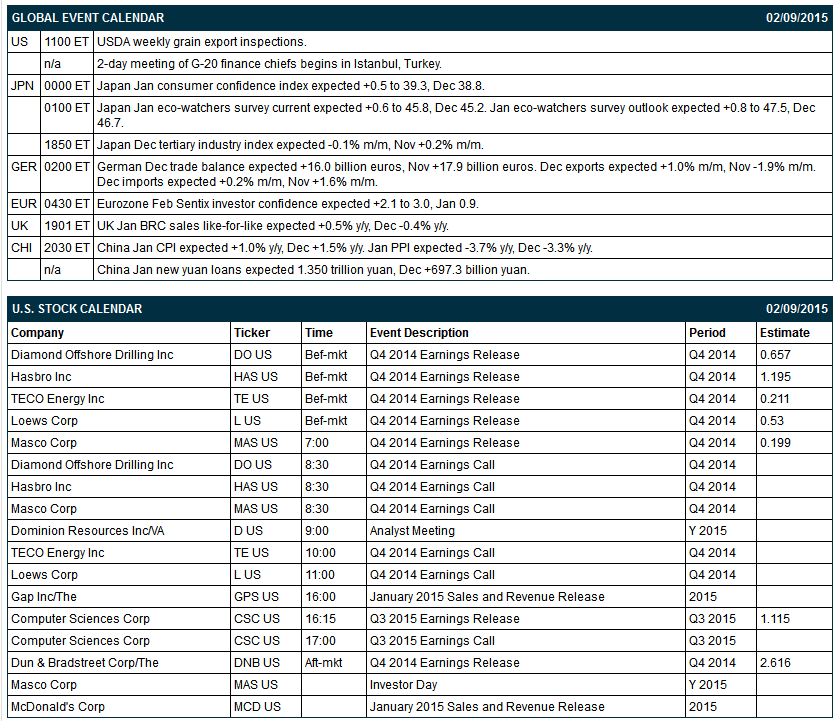

The China Jan trade balance unexpectedly expanded to a record +$60.03 billion surplus, wider than expectations of a +$48.90 billion surplus. Jan exports unexpectedly fell -3.3% y/y, weaker than expectations of +5.9% y/y and the lowest in 10 months. Jan imports sank -19.9% y/y, more than expectations of -3.2% y/y and the biggest decline in 5-1/2 years.

The Eurozone Feb Sentix investor confidence jumped +11.5 to 12.4, more than expectations of +2.1 to 3.0 and the highest in 9 months.

The German Dec trade balance unexpectedly widened to a surplus of +19.1 billion euros, wider than expectations of +16.0 billion euros. Dec exports rose +3.4% m/m, better than expectations of +1.0% m/m. Dec imports unexpectedly fell -0.8% m/m, weaker than expectations of +0.2% m/m.

The Japan Jan consumer confidence index rose +0.3 to 39.1, less than expectations of +0.5 to 39.3.

U.S. STOCK PREVIEW

There are no U.S. economic reports today. There are 7 of the S&P 500 companies that report earnings today: Diamond Offshore Drilling (consensus $0.66), Hasbro (1.20), TECO Energy (0.21), Loews (0.53), Masco (0.20), Computer Sciences (1.12), Dun & Bradstreet (2.62).

Equity conferences this week include: Stifel, Nicolaus Technology, Internet & Media Conference on Mon-Tue, BIO CEO & Investor Conference on Tue, Credit Suisse Financial Services Forum on Tue-Wed, Stifel Transportation and Logistics Conference on Tue-Wed, Goldman Sachs Technology & Internet Conference on Tue-Thu, Aviation Festival Asia on Wed-Thu, Bank of America Merrill Lynch Insurance Conference on Wed-Thu, Leerink Swann Global Health Care Conference on Wed-Thu, Bank of America Merrill Lynch Rates and Currencies Risk Management Conference on Wed-Thu, BB&T Capital Markets Transportation Services Conference on Wed-Thu, and Morgan Stanley Chemicals Corporate Access Day on Thu.

OVERNIGHT U.S. STOCK MOVERS

Alcoa (AA -2.93%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Buffalo Wild Wings (BWLD +7.12%) was downgraded to 'Hold' from 'Buy' at Miller Tabak.

Pfizer (PFE +0.55%) was upgraded to 'Outperform' from 'Market Perform' at BMO Capital.

B. Riley downgraded Skechers (SKX -0.81%) to 'Neutral' from 'Buy.'

Prudential (PRU +3.29%) was downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Abercrombie & Fitch (ANF -0.15%) was downgraded to 'Sell' from 'Hold' at Wunderlich.

TECO Energy (TE -3.26%) reported Q4 EPS of 19 cents, less than consensus of 21 cents.

Loews (L +0.02%) reported Q4 EPS of 59 cents, better than consensus of 53 cents.

Masco (MAS +1.80%) reported Q4 EPS pf 24 cents, more than consensus of 20 cents.

Hasbro (HAS -0.69%) reported Q4 EPS of $1.22, highe than consensus of $1.20.

Diamond Offshore Drilling (DO -0.68%) reported Q4 EPS of 73 cents, better than consensus of 66 cents.

Barron's reports that Hillenbrand (HI +2.81%) , which generates lots of free cash and is modestly valued, could see its shares rise 20% over the next year.

Dominion (D -3.79%) reported Q4 EPS of 84 cents, better than consensus of 83 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.54%) this morning are down -12.25 points (-0.60%). The S&P 500 index on Friday rallied up to a 1-1/4 month high but gave up its gains and closed lower: S&P 500 -0.34%, Dow Jones -0.34%, Nasdaq -0.65%. Bullish factors included (1) the +257,000 increase in U.S. Jan non-farm payrolls, more than expectations of +230,000, along with the upward revision in Dec payrolls to +329,000 from the originally reported +252,000, and (2) the +0.5% m/m increase in U.S. Jan avg hourly earnings, more than expectations of +0.3% m/m and the largest monthly increase in 6 years. Stocks fell back and closed lower on long liquidation after Philadelphia Fed President Plosser said that stronger U.S. economic data has him "at the cusp" of thinking the time to raise interest rates is now.

Mar 10-year T-notes (ZNH15 +0.17%) this morning are up +7.5 ticks. Mar 10-year T-note futures prices on Friday slid to a 1-month low and closed lower. Closes: TYH5 -1-4.5/32, FVH5 -27.25. Bearish factors included (1) the larger-than-expected increase in U.S. Jan non-farm payrolls and Jan hourly earnings, which increases the likelihood the Fed raises interest rates as soon as Jun, and (2) hawkish comments from Philadelphia Fed President Plosser who said "we're fast approaching" the point where it's hard to justify not raising rates.

The dollar index (DXY00 unch) this morning is down -0.028 (-0.03%). EUR/USD (^EURUSD) is down -0.0006 (-0.05%). USD/JPY (^USDJPY) is down-0.64 (-0.54%). The dollar index on Friday closed higher: Dollar index +1.129 (+1.21%), EUR/USD -0.01663 (-1.45%), USD/JPY +1.606 (+1.37%). Bullish factors included (1) the stronger-than-expected U.S. Jan payrolls report, which bolsters the outlook for the Fed to raise interest rates sooner rather than later, and (2) weakness in the yen after USD/JPY climbed to a 3-week high as an early rally in the S&P 500 to a 1-1/4 month high reduced the safe-haven demand for the yen.

Mar WTI crude oil (CLH15 +1.66%) this morning is up +71 cents (+1.37%) and Mar gasoline (RBH15 +1.12%) is up +0.0129 (+0.83%). Mar crude oil and Mar gasoline on Friday closed higher: CLH5 +1.21 (+2.40%), RBH5 +0.0402 (+2.64%). Bullish factors included (1) the larger-than-expected increase in U.S. Jan non-farm payrolls, a sign of economic strength, (2) signs that U.S. oil production may fall after data from Baker Hughes that showed operating U.S. oil rigs in the week ended Feb 6 fell to a 3-year low of 1140, and (3) the ongoing strike by the United Steelworkers union, which represents employees at more than 200 refineries and 10% of U.S. refining output, which may lead to reduced gasoline and distillate output.

Click on picture to enlarge

Disclosure: None.