Morning Call For February 27, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.15%) this morning are down -0.12% and European stocks are down -0.04% on expectations for U.S. Q4 GDP to be revised lower later today. Stock losses were limited after German lawmakers approved an extension of Greece's loan program. Asian stocks closed mixed: Japan +0.06%, Hong Kong -0.32%, China +0.18%, Taiwan closed for holiday, Australia +0.34%, Singapore -0.68%, South Korea -0.58%, India +1.65%. Japan's Nikkei Stock Index rose to a 14-3/4 year high after Jan industrial production rose more than expected by the most in 3-1/2 years. China's Shanghai Stock Index climbed to a 4-week high ahead of the annual National People's Congress meeting next week. China's yuan fell to 6.2699 per dollar, a 2-1/3 year low, after the PBOC cut its reference rate by the most in a month. Commodity prices are mixed. Apr crude oil (CLJ15+1.43%) is up +1.74% and Apr gasoline (RBJ15 +1.12%) is up +0.95% at a 2-1/2 month high. Apr gold (GCJ15 -0.10%) is down -0.20%. Mar copper (HGH15 -0.94%) is down -0.87% after weekly Shanghai copper inventories surged +50,475 MT to 205,146 MT, an 11-month high. Agriculture prices are higher. The dollar index (DXY00 -0.26%) is down -0.27%. EUR/USD (^EURUSD) is up +0.22%. USD/JPY (^USDJPY) is down -0.07%. Mar T-note prices (ZNH15 -0.11%) are down -6 ticks.

The Japan Jan jobless rate unexpectedly rose +0.2 to 3.6% when expectations were for no change at 3.4%. The Jan job-to-applicant ratio was unchanged at 1.14, weaker than expectations of 1.15.

Japan Jan overall household spending fell -5.1% y/y, weaker than expectations of -4.1% y/y and the tenth consecutive month that spending has declined.

Japan Jan national CPI rose 2.4% y/y, right on expectations. Jan national CPI ex-fresh food rose +2.2% y/y, less than expectations of +2.3% y/y and the slowest pace of increase in 10 months. Jan national CPI ex food & energy rose +2.1% y/y, right on expectations.

Japan Jan industrial production rose +4.0% m/m, stronger than expectations of +2.7% m/m and the largest increase in 3-1/2 years. Year-over-year, Jan industrial production fell -2.6% y/y, less than expectations of -3.1% y/y.

Japan Jan retail sales fell -1.3% m/m and -2.0% y/y, weaker than expectations of -0.4% m/m and -1.2% y/y.

The German Jan import price index fell -0.8% m/m and -4.4% y/y, less than expectations of -1.1% m/m and -4.6% y/y.

U.S. STOCK PREVIEW

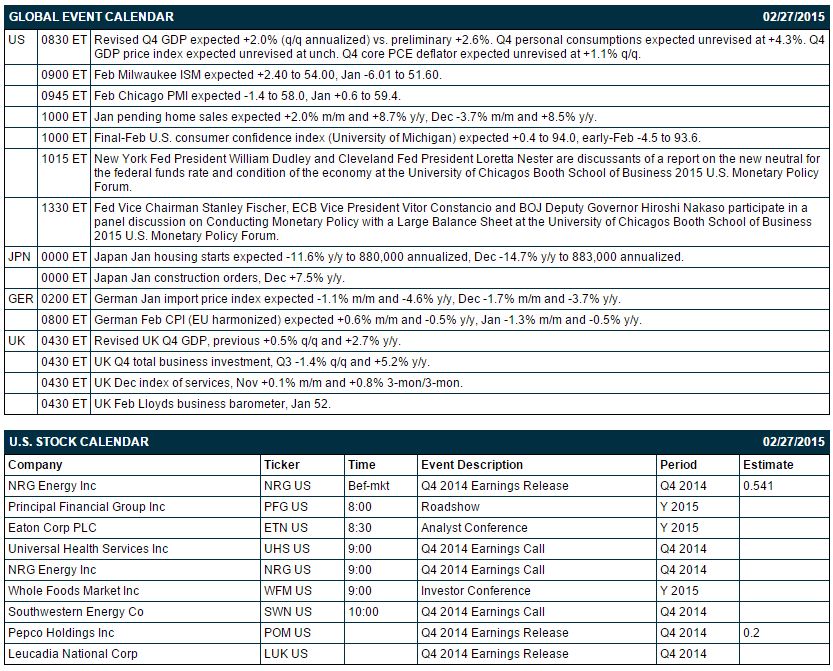

Today’s Q4 GDP report is expected to be revised substantially lower to +2.0% (q/q annualized) from +2.6% in the preliminary report due to weaker trade and inventory figures. Today’s final-Feb U.S. consumer confidence index from the University of Michigan is expected to be revised higher by +0.4 points to 94.0 from the early-Feb level of 93.6. Today’s Feb Chicago PMI is expected to show a decline of -1.4 to 58.0, more than offsetting the +0.6 point increase to 59.4 seen in January. The market is expecting today’s Jan pending home sales report to show a +2.0% m/m increase, recovering some ground after December’s -3.7% decline.

There are 3 of the S&P 500 companies that report earnings today: NRG Energy (consensus $0.54), Pepco (0.20), Leucadia National Corp. Equity conferences during the remainder of this week include: Gabelli & Company Inaugural Waste & Environmental Services Symposium on Fri.

OVERNIGHT U.S. STOCK MOVERS

CBOE Holdings (CBOE -1.63%) was downgraded to 'Neutral' from 'Buy' at BofA/Merrill Lynch.

FedEx (FDX -0.59%) was upgraded to 'Outperform' from 'Neutral' at Credit Suisse.

Universal Health (UHS +3.02%) reported Q4 EPS of $1.71, better than consensus of $1.50.

Southwestern Energy (SWN -5.79%) reported Q4 adjusted EPS of 52 cents, higher than consensus of 50 cents.

MasTec (MTZ -0.96%) reported Q4 adjusted EPS of 40 cents, above consensus of 38 cents.

Bio-Rad (BIO +0.91%) reported Q4 EPS of $1.34, higher than consensus of $1.18.

Tutor Perini (TPC -0.73%) reported Q4 EPS of 56 cents, weaker than consensus of 71 cents, and then lowered guidance on fiscal 2015 EPS to $2.20-$2.50, well below consensus of $2.89.

Mentor Graphics (MENT -2.73%) reported Q4 EPS of $1.09, better than consensus of $1.07.

Ingram Micro (IM -0.04%) reported Q4 EPS of 98 cents, less than consensus of 99 cents.

Herbalife (HLF +3.45%) reported Q4 adjusted EPS of $1.41, better than consensus of $1.22, but then lowered guidance on fiscal 2015 adjusted EPS to $4.10-$4.50, well below consensus of $5.08.

J.C. Penney (JCP +1.45%) dropped over 11% in after-hours trading after it reported Q4 adjusted EPS of 0 cents, well below consensus of 11 cents.

Monster Beverage (MNST +0.77%) gained over 4% in after-hours trading after it reported Q4 EPS of 72 cents, well above consensus of 59 cents.

Autodesk (ADSK -1.61%) reported Q4 EPS of 25 cents, above consensus of 24 cents, but then lowerd guidance on fical 2016 EPS to $1.05-$1.20, below consensus of $1.32.

Ross Stores (ROST +0.60%) jumped nearly 5% in after-hours trading after it reported Q4 EPS of $1.20, higher than consensus of $1.11, and then announced a new $1.4 billion stock repurchase program.

The Gap (GPS +0.20%) rose nearly 3% in pre-market trading after it reported Q4 EPS of 75 cents, better than consensus of 74 cents, and then announced a $1 billion share repurchase program.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.15%) this morning are down -2.50 points (-0.12%). The S&P 500 index on Thursday closed lower: S&P 500 -0.15%, Dow Jones -0.06%, Nasdaq +0.49%. Negative factors included (1) the +31,000 increase in U.S weekly initial unemployment claims, more than expectations of +7,000, (2) the +0.3% increase in Jan durable goods orders ex-transportation, weaker than expectations of +0.5%, and (3) weakness in energy producers as crude oil fell.

Mar 10-year T-notes (ZNH15 -0.11%) this morning are down -6 ticks. Mar 10-year T-note futures prices on Thursday fell back from a 2-week high and closed lower. Closes: TYH5 -14.00, FVH5 -9.25. Bearish factors included (1) the larger-than-expected +0.2% m/m increase in Jan core CPI, which may put the Fed closer to raising interest rates, and (2) supply pressures as the Treasury auctioned $29 billion of 7-year T-notes.

The dollar index (DXY00 -0.26%) this morning is down -0.261 (-0.27%). EUR/USD (^EURUSD) is up +0.0025 (+0.22%). USD/JPY (^USDJPY) is down-0.08 (-0.07%). The dollar index on Thursday rallied to a 1-month high and closed higher: Dollar index +1.079 (+1.15%), EUR/USD -0.01638 (-1.44%), USD/JPY +0.555 (+0.47%). Bullish factors included (1) the +0.2% m/m increase in U.S. Jan core CPI, stronger than expectations of +0.1%, which reduces deflation concerns and puts the Fed closer to raising interest rates, and (2) weakness in EUR/USD which fell to a 1-month low as the ECB will soon begin its QE program and start buying sovereign debt next month.

Apr WTI crude oil (CLJ15 +1.43%) this morning is up +84 cents (+1.74%) and Apr gasoline (RBJ15 +1.12%) is up +0.0181 (+0.95%) at a 2-1/2 month high. Apr crude and Apr gasoline prices on Thursday closed lower: CLJ5 -2.82 (-5.53%), RBJ5 -0.0022 (-0.11%). Bearish factors included (1) the rally in the dollar index to a 1-month high and (2) negative carry-over from Wednesday’s EIA data that showed an +8.4 million bbl increase in weekly EIA crude inventories to a record 434.1 million bbl (EIA data since 1982) and a +2.4 million bbl increase in crude supplies at Cushing, OK, the delivery point of WTI futures, to a 1-1/2 year high of 48.68 million bbl.

Disclosure: None.