Morning Call For February 18, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 -0.06%) this morning are down -0.06% and European stocks are up +0.70% at a 6-1/2 year high on speculation Greece and its creditors may be moving toward a compromise. A rally in European bank stocks is leading the markets higher after a person familiar with the matter said Greece may seek a 6-month extension of a loan agreement as soon as today. Asian stocks closed higher: Japan +1.18%, Hong Kong +0.19%, China, Taiwan and South Korea closed for holiday, Australia +0.98%, Singapore +0.58%, India +0.63%. Japan's Nikkei Stock Index climbed to a 7-1/2 year high after the BOJ maintained record stimulus following its 2-day policy meeting and after BOJ Governor Kuroda pledged to adjust monetary policy if needed. Commodity prices are mixed. Mar crude oil (CLH15 -1.70%) is down -1.44% and Mar gasoline (RBH15 -1.20%) is down-0.71%. Apr gold (GCJ15 -0.26%) is down -0.29% at a 6-week low on optimism that Greece will ease a standoff with its creditors and before the minutes of the Jan 27-28 FOMC meeting that may signal the Fed is closer to raising interest rates. Mar copper (HGH15 +0.02%) is down -0.08%. Agriculture prices are mixed. The dollar index (DXY00 +0.24%) is up +0.29%. EUR/USD (^EURUSD) is down -0.34%. USD/JPY (^USDJPY) is up +0.07%. Mar T-note prices (ZNH15 -0.05%) are down -2.5 ticks at a 6-week low.

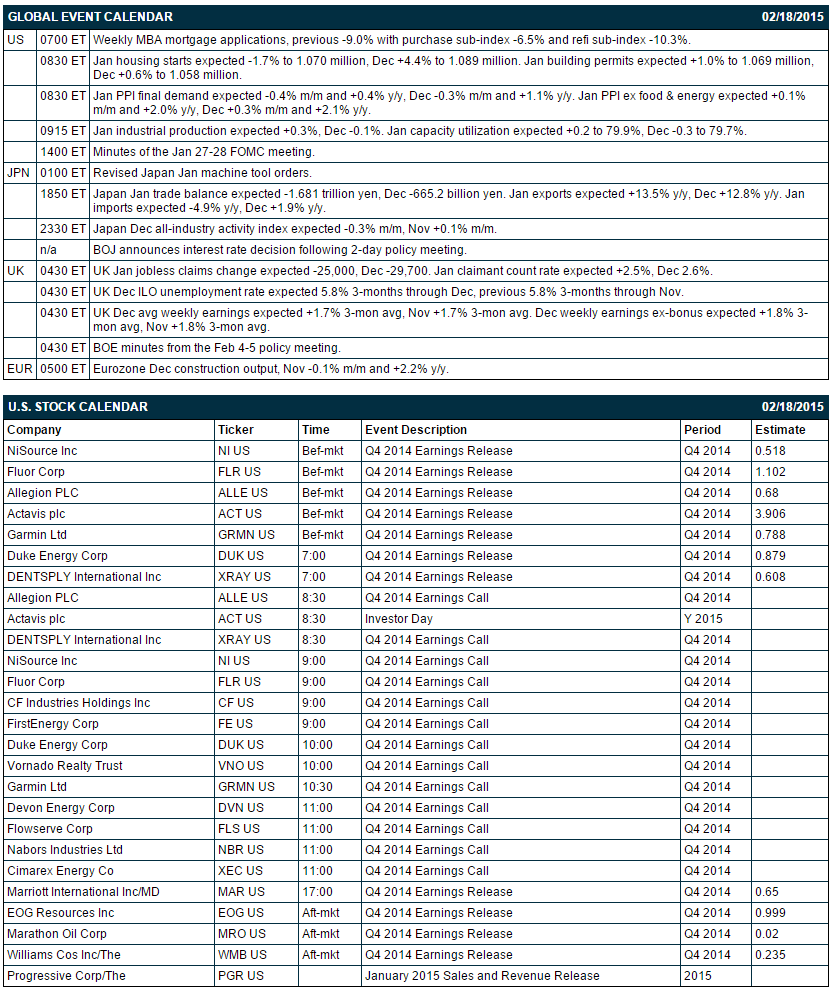

UK Jan jobless claims fell -38,600, more than expectations of -25,000 and the most in 7 months. The Jan claimant count rate fell -0.1 to 2.5%, right on expectations and the lowest in 6-3/4 years.

The UK Dec ILO unemployment rate unexpectedly fell -0.1 to 5.7% in the 3-months through Dec, better than expectations of unch at 5.8% and the lowest in 6-1/2 years.

Dec avg weekly earnings rose +2.1% 3-mon avg, more than expectations of +1.7% 3-mon avg and the most in 1-1/2 years. Dec avg weekly earnings ex-bonus rose +1.7% 3-mon avg, less than expectations of +1.8% 3-mon avg.

Eurozone Dec construction output fell -0.8% m/m and -3.5% y/y, with the -3.5% y/y drop the largest annual decline in 1-1/2 years.

U.S. STOCK PREVIEW

Today’s Jan housing starts report is expected to show a -1.7% decline to 1.070 million, giving back a little of December’s +4.4% increase to 1.089 million. Today’s Jan final-demand PPI index is expected to fall to +0.4% y/y from +1.1% in December. Meanwhile, today’s Jan core PPI index is expected to edge lower to +2.0% y/y from +2.1% in December. Today’s Jan industrial production report is expected to show an increase of +0.3%, recovering somewhat after the -0.1% decline seen in December. The FOMC today will release the minutes from the recent Jan 27-28 FOMC meeting, which was a relatively uneventful meeting.

There are 1 of the S&P 500 companies that report earnings today with notable reports including: Marathon Oil (consensus $0.02), Williams Companies (0.24), Marriott (0.67), Duke Energy (0.88), Garmin (0.79), Fluor (1.10). Equity conferences this week include: Consumer Analysts Group of New York Conference on Tue-Thu, and Barclays Industrial Select Conference on Wed-Thu.

OVERNIGHT U.S. STOCK MOVERS

Duke Energy (DUK -0.56%) reported Q4 EPS of 87 cents, below consensus of 88 cents.

Allegion PLC (ALLE -0.17%) reported Q4 EPS of 76 cents, better than consensus of 68 cents.

Exxon Mobil (XOM -0.34%) fell over 2% in pre-market trading after Berkshire Hathaway announced it had exited its $3.7 billion investment in the company.

Owens & Minor (OMI -1.00%) reported Q4 adjusted EPS of 49 cents, below consensus of 50 cents, and then lowered guidance on fiscal 2015 EPS to $1.90-$1.95, at the low end of consensus of $1.95.

Valmont (VMI +0.85%) reported Q4 adjusted EPS of $1.62, less than consensus of $1.65.

Terex ({=TEX reported Q4 adjusted EPS of 72 cents, higher than consensus of 68 cents.

CF Industries (CF -0.89%) fell over 2% in after-hours trading after it reported Q4 EPS of $4.82, below consensus of $5.08.

Norwegian Cruise Line (NCLH -0.71%) reported Q4 adjusted EPS of 36 cents, less than consensus of 37 cents.

KAR Auction (KAR -0.11%) reported Q4 adjusted EPS of 40 cents, better than consensus of 29 cents.

Flowserve (FLS +0.46%) reported Q4 EPS of $1.16, above consensus of $1.13.

Analog Devices (ADI +3.09%) reported Q1 EPS of 63 cents, better than consensus of 61 cents.

Jack in the Box (JACK +1.19%) rose over 3% in after-hours trading after it reported Q1 EPS of 93 cents, higher than consensus of 87 cents, and then raised guidance on fiscal 2015 EPS to $2.85-$2.97, above consensus $2.84.

AMC Entertainment (AMC +0.91%) reported Q4 EPS of 30 cents, well above consensus of 20 cents.

Agilent (A +0.92%) reported Q1 EPS of 41 cents, right on consensus, but then lowered guidance on fiscal 2015 EPS to $1.67- $1.73, on the low side of consensus at $1.73.

Fossil (FOSL +0.89%) reported Q4 EPS of $3.00, below consensus of $3.07, and then lowered guidance on fiscal 2015 EPS to$5.45-$6.05, well below consensus of $7.54.

Rackspace (RAX -0.28%) reported Q4 EPS of 26 cents, above consensus of 19 cents.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 -0.06%) this morning are down -1.25 points (-0.06%). The S&P 500 index on Tuesday posted a new record high and closed higher: S&P 500 +0.16%, Dow Jones +0.16%, Nasdaq +0.03%. Bullish factors included (1) reduced Greek default concerns after an unconfirmed report that Greece’s government may request an extension of its loan agreement for 6 months, something it previously said it would not do, and (2) a rally in health-care stocks. Stocks had opened lower on bearish factors that included (1) the -2.17 point decline in the Feb Empire manufacturing index, weaker than expectations of -1.95 to 8.00, and (2) the unexpected -2 point decline in the Feb NAHB housing market index to 55, weaker than expectations of +1 to 58 and a 4-month low.

Mar 10-year T-notes (ZNH15 -0.05%) this morning are down -2.5 ticks at a 6-week low. Mar 10-year T-note futures prices on Tuesday tumbled to a 1-1/4 month low and closed lower. Closes: TYH5 -31.50, FVH5 -15.50. Bearish factors included (1) hawkish comments from Cleveland Fed President Mester who said that she sees June as a “viable option” for when to begin raising interest rates, and (2) fund selling of T-notes after a report that Greece will ask for a 6-month extension of its loan agreement, which reduced Greek default concerns and curbed safe-haven demand for T-notes.

The dollar index (DXY00 +0.24%) this morning is up +0.273 (+0.29%). EUR/USD (^EURUSD) is down -0.0039 (-0.34%). USD/JPY (^USDJPY) is up +0.08 (+0.07%). The dollar index on Tuesday fell to a 1-week low and closed lower: Dollar index -0.140 (-0.15%), EUR/USD +0.00576 (+0.51%), USD/JPY +0.763 (+0.4%). Bearish factors included (1) strength in EUR/USD which rallied to a 1-week high after the German Feb ZEW survey expectations of economic growth rose to a 1-year high, and (2) weaker-than-expected U.S. economic data on Feb Empire manufacturing and the Feb NAHB housing market index that may prompt the Fed to delay interest rate hikes.

Mar WTI crude oil (CLH15 -1.70%) this morning is down -77 cents (-1.44%) and Mar gasoline (RBH15 -1.20%) is down -0.0113 (-0.71%). Mar crude and Mar gasoline on Tuesday settled mixed: CLH5 +0.75 (+1.42%), RBH5 -0.0361 (-2.22%). Bullish factors included (1) the fall in the dollar index to a 1-week low, and (2) the rally in the S&P 500 to a new all-time high. Bearish factors included expectations that Thursday’s weekly EIA data will show crude supplies rose +3.0 million bbl to a record high of 420 million bbl.

Disclosure: None.