Morning Call For February 12, 2015

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH15 +0.47%) this morning are up +0.41% and European stocks are up +1.23% at a 6-1/3 year high as stock markets around the world rallied after an agreement on a cease-fire in Ukraine was announced. Russian President Putin told reporters that after talks through the night with French, German and Ukrainian leaders in Belarus, a truce in eastern Ukraine is set to start on Feb 15. Greece's ASE Stock Index jumped over 5% on speculation that Greece was making progress on debt talks with its creditors. Eurozone finance ministers met yesterday and postponed decisions on the future of Greece's debt financing until they meet again next week. Asian stocks closed mostly higher: Japan +1.85%, Hong Kong +0.44%, China +0.25%, Taiwan +0.36%, Australia -0.44%, Singapore -0.74%, South Korea -0.28%, India +0.95%. Commodity prices are higher. Mar crude oil (CLH15 +3.15%) is up +2.62% and Mar gasoline (RBH15 +1.07%) is up +0.71%. Apr gold (GCJ15 +0.23%) is up +0.32%. Mar copper (HGH15 +1.71%) is up +1.79%. Agriculture prices are stronger. The dollar index (DXY00 -0.37%) is down -0.35%. EUR/USD (^EURUSD) is up +0.07%. USD/JPY (^USDJPY) is down -0.56%. Mar T-note prices (ZNH15 -0.32%) are down -12.5 ticks at a 5-week low.

Japan Jan PPI fell -1.3% m/m, over twice expectations of -0.6% m/m and the biggest monthly decline in 6 years. On an annual basis, Jan PPI rose +0.3% y/y, less than expectations of +1.1% y/y and the slowest pace of increase in 2-3/4 years.

Japan Dec machine orders jumped +8.3% m/m, more than expectations of +2.3% m/m and the largest monthly gain in 6 months. On an annual basis, Dec machine orders rose +11.4% y/y, better than expectations of +5.6% y/y and the largest annual increase in 8 months.

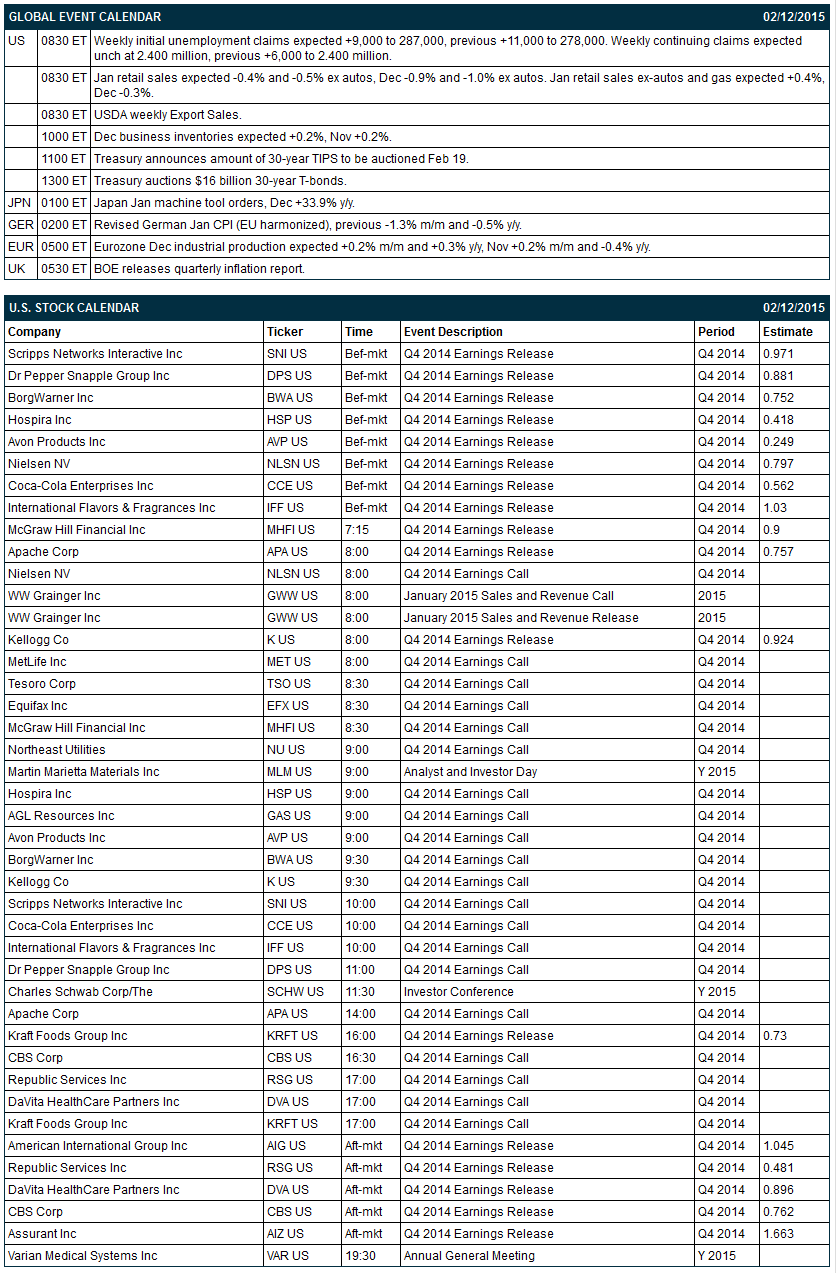

Eurozone Dec industrial production was unch m/m and fell -0.2% y/y, weaker than expectations of +0.2% m/m and +0.3% y/y.

U.S. STOCK PREVIEW

Today’s initial unemployment claims series is expected to show a +10,000 increase to 288,000, adding to last week’s increase of +11,000 to 278,000. Meanwhile, today’s continuing claims report is expected to edge higher by +1,000 to 2.401 million, adding to last week’s increase of +6,000 to 2.400 million. The Treasury today will sell $16 billion of 30-year T-bonds, concluding this week’s $64 billion coupon package. There are 17 of the S&P 500 companies that report earnings today with notable reports including: Coca-Cola Enterprises (consensus $0.56), BorgWarner (0.75), Nielsen (0.80), McGraw Hill Financial (0.90), Kellogg (0.92), Kraft Foods (0.73), AIG (1.05), CBS (0.76).

Equity conferences during the remainder of this week include: Goldman Sachs Technology & Internet Conference on Tue-Thu, Aviation Festival Asia on Wed-Thu, Bank of America Merrill Lynch Insurance Conference on Wed-Thu, Leerink Swann Global Health Care Conference on Wed-Thu, Bank of America Merrill Lynch Rates and Currencies Risk Management Conference on Wed-Thu, BB&T Capital Markets Transportation Services Conference on Wed-Thu, and Morgan Stanley Chemicals Corporate Access Day on Thu.

OVERNIGHT U.S. STOCK MOVERS

Cisco (CSCO -2.04%) jumped over 6% in pre-market trading after it reported Q2 EPS of 53 cents, better than consensus of 51 cents.

Whole Foods Markets (WFM +0.91%) rose more than 2% in pre-market trading after it reported Q1 EPS of 46 cents, higher than consensus of 45 cents.

Oceaneering (OII -0.57%) fell over 3% in after-hours trading after it reported Q4 EPS of 99 cents, right on consensus, but then lowered guidance on fiscal 2015 EPS to $3.10-$3.50, well below consensus of $3.92.

Baidu (BIDU -2.17%) dropped 9% in after-hours trading after it reported Q4 EPS of $1.61, below consensus of $1.65.

Tesla (TSLA -1.61%) slid over 7% in after-hours trading after it reported a Q4 adjusted EPS loss of -13 cents, much weaker than consensus of 31 cents.

Equifax (EFX unch) reported Q4 EPS of $1.02, higher than consensus of $1.01.

Tesoro (TSO -0.92%) reported Q4 EPS of $1.46, below consensus of $1.51.

NVIDIA (NVDA -0.67%) jumped 5% in after-hours trading after it reported Q4 EPS of 43 cents, well above consensus of 29 cents.

Northeast Utilities (NU -2.51%) reported Q4 EPS ex-items of 72 cents, higher than consensus of 69 cents.

C&J Energy (CJES -0.95%) reported Q4 adjusted EPS of 54 cents, stronger than consensus of 43 cents.

Catalent (CTLT +5.16%) reported Q2 adjusted EPS of 44 cents, well above consensus of 34 cents.

NetApp (NTAP +0.89%) slid over 5% in after-hours trading after it reported Q3 EPS of 75 cents, less than consensus of 77 cents.

MetLife (MET +0.76%) reported Q4 operating EPS of $1.38, above consensus of $1.36.

Applied Materials (AMAT -0.08%) reported Q1 adjusted EPS of 27 cents, right on consensus, although Q1 revenue of $2.36 billion was above consensus of $2.33 billion.

Insight Enterprises (NSIT +0.54%) reported Q4 adjusted EPS of 55 cents, below consensus of 58 cents.

Skechers (SKX +5.15%) reported Q4 EPS of 43 cents, right on consensus, although Q4 revenue of $569.7 million was better than consensus of $542.75 million.

MARKET COMMENTS

Mar E-mini S&Ps (ESH15 +0.47%) this morning are up +8.50 points (+0.41%). The S&P 500 index on Wednesday closed unchanged: S&P 500 unch, Dow Jones -0.04%, Nasdaq +0.38%. Stocks traded lower most of the day after an emergency meeting of Eurozone finance ministers failed to find a solution to Greece's debt problems as Germany remains steadfast in its insistence that Greece comply with the original terms of its bailout agreement. Prices rebounded in late trading, however, and closed little changed after several unnamed Eurozone officials said that the Eurozone finance ministers were closing in on an extension of Greece's rescue agreement with its creditors.

Mar 10-year T-notes (ZNH15 -0.32%) this morning are down -12.5 ticks at a 5-week low. Mar 10-year T-note futures prices on Wednesday closed unchanged. Closes: TYH5 unch, FVH5 unch. Bullish factors included (1) increased safe-haven demand as stocks fell early, and (2) strong foreign demand for the Treasury's $24 billion 10-year T-note auction after indirect bidders, a class of investors that includes foreign central banks, purchased 59.5% of the total auction, above the 12-auction average of 46.3% and the most in 3 years. T-notes shed their gains late in the day after stocks recovered.

The dollar index (DXY00 -0.37%) this morning is down -0.333 (-0.35%). EUR/USD (^EURUSD) is up +0.0008 (+0.07%). USD/JPY (^USDJPY) is down -0.67 (-0.56%). The dollar index on Wednesday rose to a 2-week high and closed higher: Dollar index +0.227 (+0.24%), EUR/USD +0.00139 (+0.12%), USD/JPY +1.017 (+0.85%). Bullish factors included (1) the ongoing Greek debt financing situation along with concern that a failure in the Ukraine/Russian peace talks may lead to an expanding conflict in Ukraine, and (2) the rally in USD/JPY to a 5-week high as a rally in stocks curbed the safe-haven demand for the yen.

Mar WTI crude oil (CLH15 +3.15%) this morning is up +$1.28 a barrel (+2.62%) and Mar gasoline (RBH15 +1.07%) is up +0.0109 (+0.71%). Mar crude oil and Mar gasoline on Wednesday closed lower: CLH5 -1.18 (-2.36%), RBH5 -0.0091 (-0.59%). Bearish factors included (1) the rally in the dollar index to a 2-week high, (2) the +4.87 million bbl increase in EIA crude inventories to a record high of 417.9 million bbl, (3) the +1.98 million bbl increase in EIA gasoline supplies to 242.7 million bbl, a 15-year high, and (4) the +1.2 million bbl increase in crude stockpiles at Cushing, OK, delivery point of WTI futures, to 42.6 million bbl, a 1-1/2 year high.

Click on picture to enlarge

Disclosure: None.