Morning Call For December 3, 2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.01%) this morning are down -0.02% ahead of the Nov ADP employment report, while European stocks are up +0.10% as signs of slower growth in the Eurozone bolstered the case for more stimulus after the Eurozone Nov Markit composite PMI was revised lower to its slowest pace of expansion in 16 months. The Russian ruble fell back from a record low of 54.9090 per dollar after the Bank of Russia said it sold $700 million of dollars on Dec 1, its first intervention since moving to a free float 3-weeks ago. Asian stocks closed mostly higher: Japan +0.32%, Hong Kong -0.95%, China +1.49%, Taiwan +1.55%, Australia +0.77%, Singapore -0.57%, South Korea +0.10%, India unchanged. Japan's Nikkei Stock Index jumped to a 7-1/3 year high as a plunge in the yen to a 7-1/3 year low against the dollar boosts the earnings prospects of Japanese exporters. China's Shanghai Stock Index rose to a 3-1/3 year high on speculation the PBOC will loosen monetary policy further to support economic growth. Commodity prices are mixed. Jan crude oil (CLF15 +0.30%) is up +0.48%. Jan gasoline (RBF15 -0.67%) is down -0.55%. Feb gold (GCG15 +0.26%) is up +0.11%. Mar copper (HGH15 -0.54%) is down -0.61%. Agriculture prices are weaker. The dollar index (DXY00 +0.22%) is up +0.27% at a new 5-1/2 year high. EUR/USD (^EURUSD) is down -0.48% at a 2-1/4 year low on speculation the ECB will expand stimulus measures when it meets tomorrow. USD/JPY (^USDJPY) is up +0.19% at a fresh 7-1/3 year high. Mar T-note prices (ZNH15 -0.09%) are down -3.5 ticks.

The Eurozone Nov Markit composite PMI was revised lower to 51.1 from the originally reported 51.4, the slowest pace of expansion in 16 months.

Eurozone Oct retail sales rose +0.4% m/m and +1.4% y/y, a smaller increase than expectations of +0.5% m/m and +1.6% y/y.

The UK Nov Markit/CIPS services PMI rose +2.4 to 58.6, a larger increase than expectations of +0.3 to 56.5.

The China Nov non-manufacturing PMI rose +0.1 to 53.9, the first increase in 3 months.

The Japan Nov Markit services PMI rose +1.9 to 50.6.

U.S. STOCK PREVIEW

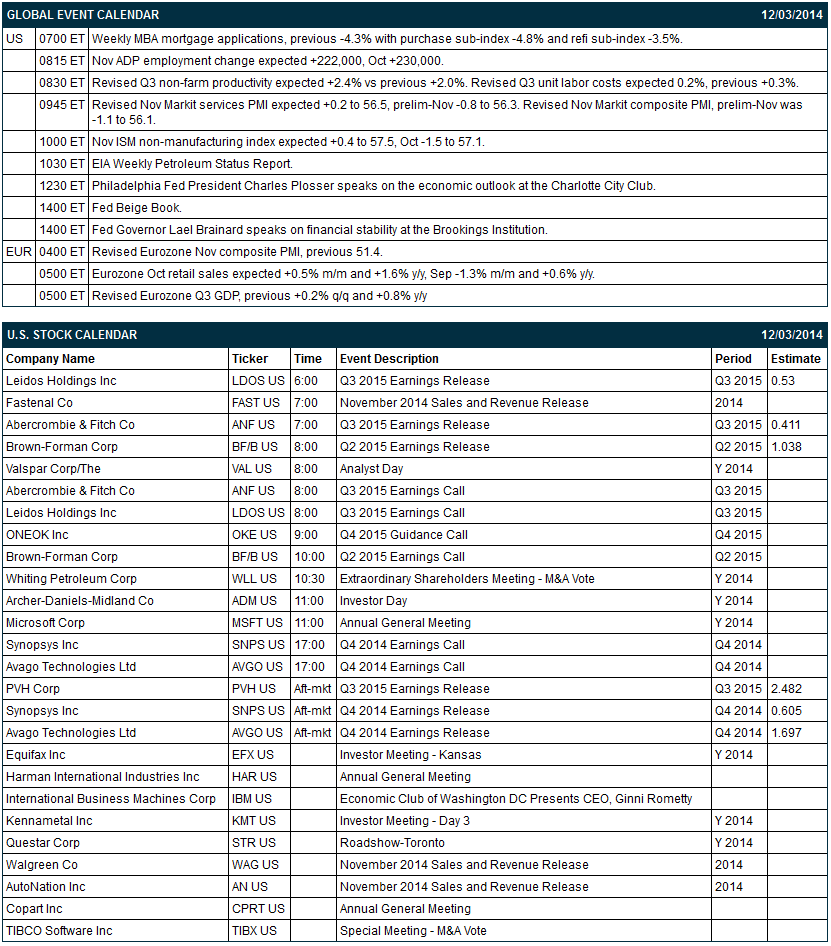

Today’s Nov ADP employment report is expected to show another solid increase of +225,000, which would be close to October’s rise of +230,000. Today’s Nov ISM non-manufacturing index is expected to show a +0.4 increase to 57.5, recovering a bit after the fairly large -1.5 point decline to 57.1 seen in October. Today’s Fed Beige Book should be generally upbeat about the U.S. economy given the recent economic data. There are 6 of the Russell 1000 companies that report earnings today: Abercrombie & Fitch (consensus $0.41), Brown-Forman (1.04), PVH (2.48), Avago Technologies (1.70), Synopsys (0.61), Leidos Holdings (0.53).

Equity conference this week include: NASDAQ OMX Investor Program on Mon-Wed, Bank of America Merrill Lynch Leveraged Finance Conference on Tue-Wed, Big Data & Analytics for Banking Summit on Tue-Wed, Citi Basic Materials Conference on Tue-Wed, Piper Jaffray Health Care Conference on Tue-Wed, Credit Suisse Global Industrials Conference on Tue-Wed, Credit Suisse Technology Conference on Tue-Thu, Goldman Sachs Global Automotive Conference on Thu, and SEMICON Japan 2014 on Thu.

OVERNIGHT U.S. STOCK MOVERS

Abercrombie & Fitch (ANF -1.10%) dropped over 5% in pre-market trading after it said it sees Q4 Same-Store-Sales down by mid-to-high single-digit percentage as it lowered guidance on fiscal 2014 adjusted EPS to $1.50-$1.65, below consensus of $1.74.

DISH (DISH -2.42%) was downgraded to 'Sell' from 'Hold' at Wunderlich.

Vale (VALE -4.58%) was upgraded to 'Buy' from 'Hold' at Canaccord.

CBOE Holdings (CBOE +0.63%) was downgraded to 'Sell' from 'Neutral' at Citigroup.

Leidos (LDOS +0.75%) reported Q3 EPS of 65 cents, well above consensus of 53 cents.

British Petroleum (BP +2.23%) was upgraded to 'Overweight' from 'Equal Weight' at Barclays.

J.C. Penney (JCP -1.86%) fell nearly 3% in pre-market trading after Golman Sachs downgraded the stock to 'Sell' from 'Neutral."

comScore reports that Cyber Monday desktop online spending reached $2.04 billion, up +17% versus a year ago and the heaviest online spending day in history.

OmniVision (OVTI +6.35%) reported Q2 non-GAAP EPS of 60 cents, well above consensus of 51 cents.

Point72 Asset Management reported a 5.1% passive stake in Catalyst Pharmaceutical (CPRX +4.18%) .

Ascena Retail (ASNA -0.69%) jumped over 5% in after-hours trading after it reported Q1 adjusted EPS of 28 cents, better than consensus of 26 cents.

Bob Evans (BOBE +2.84%) reported Q2 adjusted EPS of 36 cents, higher than consensus of 33 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.01%) this morning are down -0.50 of a point (-0.02%). The S&P 500 index on Tuesday closed higher: S&P 500 +0.64%, Dow Jones +0.58%, Nasdaq +0.42%. Bullish factors included (1) carry-over support from a rally in China’s Shanghai Stock Index to a 3-1/3 year high on speculation the PBOC may be preparing the markets for additional stimulus after it refrained from draining funds from the financial system for the second time in the last five days, and (2) the +1.1% m/m increase in U.S. Oct construction spending, better than expectations of +0.6% m/m and the most in 5 months.

Mar 10-year T-notes (ZNH15 -0.09%) this morning are down -3.5 ticks. Mar 10-year T-note futures prices on Tuesday closed lower: TYH5 -18.50, FVH5-10.75. Negative factors included (1) the larger-than-expected +1.1% increase in Oct construction spending, the most in 5 months, which could push the Fed closer to raising interest rates, and (2) reduced safe-haven demand for T-note as stocks rallied.

The dollar index (DXY00 +0.22%) this morning is up +0.237 (+0.27%) at a 5-1/2 year high. EUR/USD (^EURUSD) is down -0.0059 (-0.48%) at a 2-1/4 year low. USD/JPY (^USDJPY) is up +0.23 (+0.19%) at a 7-1/3 year high. The dollar index on Tuesday climbed to a 4-1/2 year high and closed higher. Closes: Dollar index -0.410 (-0.46%), EUR/USD +0.00187 (+0.15%), USD/JPY -0.270 (-0.23%). Bullish factors included (1) the larger-than-expected increase in U.S. Oct construction spending, which bolsters the case for the Fed to raise interest rates, and (2) the surge in USD/JPY to a 7-1/3 year high on stronger interest rate differentials for the dollar versus the yen on the prospects for the BOJ to expand stimulus while the Fed stands pat.

Jan WTI crude oil (CLF15 +0.30%) this morning is up +32 cents (+0.48%) and Jan gasoline (RBF15 -0.67%) is down -0.0100 (-0.55%). Jan crude and Jan gasoline on Tuesday closed lower. Closes: CLF5 -2.12 (-3.07%), RBF5 -0.0636 (-3.38%). Bearish factors included (1) a rally in the dollar index to a 4-1/2 year high, (2) an agreement by the Iraqi government and Kurdish authorities that will allow the Kurds to export 300,000 bpd of crude into Turkey, and (3) expectations for weekly EIA crude inventories to rise by +1.75 million bbl on Wednesday.

Disclosure: None