Morning Call For Aug. 21, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 +0.15%) this morning are up +0.18% at a record high and European stocks are up +0.72% at a 2-1/2 week high on economic optimism along with signs of increased M&A activity. AstraZeneca Plc, the UK's second-largest drug maker, rose over 2% after people familiar with the matter said Pfizer executives would prefer to buy AstraZeneca rather than a different pharmaceutical company. Manufacturing activity in the Eurozone and China grew at a slower pace than expected as rising political tensions threaten global economic growth. The Eurozone Aug Markit manufacturing PMI fell -1.0 to a 13-month low of 50.8 and bolstered the outlook for the ECB to expand stimulus. Asian stocks closed mixed: Japan +0.85%, Hong Kong -0.66%, China -0.50%, Taiwan -0.37%, Australia +0.08%, Singapore +0.01%, South Korea -1.60%, India +0.17%. Japan's Nikkei Stock Index rose to a 2-1/2 week high as exporters rallied on improved earnings prospects after the yen fell to a 4-1/2 month low against the dollar. Commodity prices are mixed. Oct crude oil (CLV14 -0.75%) is down -0.68% at a fresh 7-1/4 month low on demand concerns after Chinese and Eurozone manufacturing activity slowed more than expected. Oct gasoline (RBV14 -0.45%) is down -0.33%. Dec gold (GCZ14 -1.07%) is down -0.99%at a 2-month low as the dollar index surged to an 11-1/2 month high after the minutes of the Jul 29-30 FOMC meeting raised the possibility the Fed may hike interest rates sooner than anticipated. Sep copper (HGU14 -0.68%) is down -0.79%. Agriculture and livestock prices are mixed with Oct hogs down -1.19% at a fresh 6-1/4 month low. The dollar index (DXY00 +0.02%) is up +0.02% at an 11-1/2 month high on the heels of the hawkish minutes of the Jul 29-30 FOMC meeting. EUR/USD (^EURUSD) is up +0.05% as it recovers from an 11-1/4 month low. USD/JPY (^USDJPY) is up +0.05% at a 4-1/2 month high as the rally in stocks undercuts the safe-haven demand for the yen. Sep T-note prices (ZNU14 -0.07%) are down -2 ticks at a 1-week low.

The Eurozone Aug Markit manufacturing PMI fell -1.0 to 50.8, a bigger drop than expectations of -0.5 to 51.3 and the slowest pace of expansion in 13 months. The Aug Markit composite PMI slipped -1.0 to 52.8, a bigger drop than expectations of -0.4 to 53.4 and matched June's level as the slowest pace of expansion in 8 months.

The German Aug Markit/BME manufacturing PMI fell -0.4 to 52.0, a smaller decline than expectations of -0.9 to 51.5. The Aug Markit services PMI fell-0.3 to 56.4, a smaller decline than expectations of -0.8 to 55.5.

The China Aug HSBC flash manufacturing PMI fell -1.4 to 50.3, a larger decline than expectations of -0.2 to 51.5.

UK retail sales data were mixed with Jul retail sales ex autos up +0.5% m/m and +3.4% y/y, close to expectations of +0.4% m/m and +3.5% y/y, while Jul retail sales including autos rose +0.1% m/m and +2.6% y/y, weaker than expectations of +0.4% m/m and +3.1% y/y.

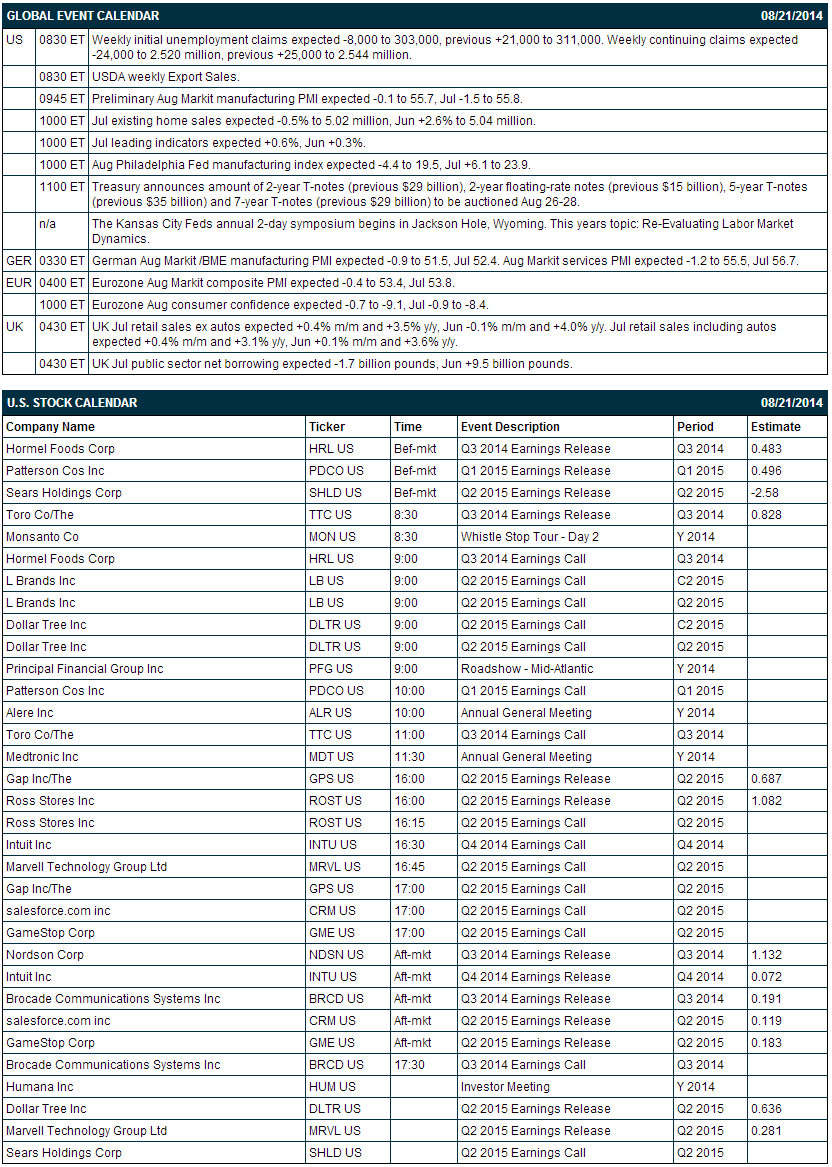

UK Jul public sector net borrowing fell -1.1 billion pounds, a smaller decline than expectations of -1.7 billion pounds.

The Japan Aug Markit/JMMA manufacturing PMI rose +1.9 to 52.4, stronger than expectations of +1.0 to 51.5 and the fastest pace of expansion in 5 months.

U.S. STOCK PREVIEW

The market is expecting today’s weekly initial unemployment claims report to show a decline of -8,000 to 303,000, reversing about one-half of last week’s rather large +21,000 increase to 311,000. The market is looking for today’s July existing home sales report to show a decline of -0.5% to 5.02 million, giving back some of the +2.6% increase to 5.04 million seen in June. The market is expecting today’s Aug Philadelphia Fed manufacturing index to show a -4.4 point decline to 19.5, reversing most of the +6.1 point increase to a 3-1/2 year high of 23.9 seen in July. The market consensus is that today’s July U.S. leading indicators index will show a strong increase of +0.6%, adding to the +0.3% increase seen in June.

There are thirteen S&P 500 companies that reports earnings today: Hormel Foods (consensus $0.48), Patterson Cos. (0.50), Sears Holdings (-2.58), Toro (0.83), The Gap (0.69), Ross Stores (1.08), Nordson (1.13), Intuit (0.07), Brocade (0.19), salesforce.com (0.12), GameStop (0.18), Dollar Tree (0.64) and Marvell Technology (0.28). Equity conferences this week include: Enercom, Inc Oil & Gas Conference on Mon-Thu.

OVERNIGHT U.S. STOCK MOVERS

Hormel Foods ({=HRL reported Q3 EPS of 51 cents, higher than consensus of 48 cents.

Patterson Cos. (PDCO +0.10%) reported Q1 EPS of 50 cents, right on expectations.

Dollar Tree (DLTR +0.53%) reported Q2 EPS of 61 cents, weaker than consensus of 64 cents.

Sears Holdings (SHLD +1.27%) reported a Q2 EPS loss of -$5.39, a much wider loss than consensus of -$2.63.

Bon-Ton Stores (BONT -1.20%) reported a Q2 EPS loss of -$1.86, a larger loss than consensus of -$1.54.

Madison Square Garden (MSG +3.44%) was downgraded to 'Hold' from 'Buy' at Stifel.

Baird raised its price target on Lowe's (LOW +1.57%) to $60 from $57 and kept its 'Outperform' rating on the stock.

Sally Beauty (SBH +0.98%) rose nearly 2% in after-hours trading after the company authorized a new $1.0 billion share repurchase program.

American Eagle (AEO +11.99%) was upgraded to 'Buy' from 'Neutral' at SunTrust.

L Brands (LB -0.38%) reported Q2 EPS of 63 cents, better than consensus of 62 cents.

CACI (CACI +0.23%) reported Q4 EPS of $1.49, stronger than consensus of $1.43.

Synopsys (SNPS +0.51%) reported Q3 EPS of 65 cents, higher than consensus of 60 cents.

Hewlett-Packard (HPQ -1.01%) reported Q3 adjusted EPS of 89 cents, right on consensus, although Q3 revenue of $27.6 billion was better than consensus of $27.01 billion.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 +0.15%) this morning are up +3.50 points (+0.18%) at a new record high. The S&P 500 index on Wednesday rose to a 3-week high and settled higher: S&P 500 +0.25%, Dow Jones +0.35%, Nasdaq +0.01%. Bullish factors for stocks included (1) signs of strength in the global economy after Japan Jul exports rose +3.9% y/y, slightly better than expectations of +3.8% y/y, and (2) speculation that Fed Chair Yellen will reiterate at Friday's annual Fed conference in Jackson Hole, Wyoming that the Fed intends to keep interest rates at record lows even as economic growth show signs of accelerating. Stocks came off of their best levels after the minutes of the Jul 29-30 FOMC meeting raised the possibility that monetary stimulus may end sooner than anticipated.

Sep 10-year T-notes (ZNU14 -0.07%) this morning are down -2 ticks at a 1-week low. Sep 10-year T-note futures prices on Wednesday closed lower on reduced safe-haven demand after the S&P 500 rallied to a 3-week high and after the minutes of the Jul 29-30 FOMC meeting raised the possibility the Fed may hike interest rates sooner than expected. Closes: TYU4 -9.5, FVU4 -8.2.

The dollar index (DXY00 +0.02%) this morning is up +0.014 (+0.02%) at a fresh 11-1/2 month high. EUR/USD (^EURUSD) is up +0.0006 (+0.05%) and USD/JPY (^USDJPY) is up +0.05 (+0.05%) at a 4-1/2 month high. The dollar index on Wednesday posted an 11-1/4 month high and closed higher. Bullish factors included (1) the hawkish minutes of the Jul 29-30 FOMC meeting that showed policy makers may raise interest rates sooner than anticipated, and (2) weakness in EUR/USD which fell to an 11-1/4 month low on deflation concerns after German Jul PPI fell -0.1% m/m and -0.8% y/y, a faster pace of decline than expectations of unch m/m and -0.7% y/y. Closes: Dollar index +0.343 (+0.42%), EUR/USD -0.00609 (-0.46%), USD/JPY +0.84 (+0.82%).

Oct WTI crude oil (CLV14 -0.75%) this morning is down -64 cents (-0.66%) at a 7-1/4 month low and Oct gasoline (RBV14 -0.45%) is down -0.0086(-0.33%). Oct crude and gasoline prices on Wednesday closed higher: CLV4 +0.59 (+0.64%), RBV4 +0.0154 (+0.60%). Bullish factors for crude prices included (1) the -4.474 million bbl decline in weekly EIA crude inventories, more than expectations of -1.15 million bbl, and (2) the unexpected +1.8 point increase in the weekly refinery utilization rate, more than expectations of a -0.4 decline. Gains were limited after the dollar index posted an 11-1/4 month high and after crude supplies at Cushing, OK, the delivery point of WTI futures, rose +1.75 million bbl.

Disclosure: None