Morning Call For Aug. 1, 2014

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU14 -0.58%) this morning are down -0.57% at a 1-3/4 month low and European stocks are down -1.42% at a 4-month low as the global stock market rout continues for a second day. The Eurozone Jul manufacturing PMI was revised downward to match its slowest pace of expansion in 8 months, while developments in Latin America will be closely monitored after Argentina missed a deadline Thursday to pay $539 million in interest. The International Swaps & Derivatives Association said it will decide later this morning if credit-default swaps linked to Argentina debt have been triggered by a failure-to-pay credit event. Asian stocks closed lower: Japan -0.63%, Hong Kong -0.91%, China -0.89%, Taiwan -0.53%, Australia-1.36%, Singapore -0.88%, South Korea -0.42%, India -1.60%. China's Shanghai Stock Index initially rallied up to a 7-1/2 month high after Chinese Jul manufacturing activity expanded at the fastest pace in 2-1/4 years, but stock prices fell back and closed lower as the global stock market selloff overshadowed the better-than-expected manufacturing data. Commodity prices are mostly lower. Sep crude oil (CLU14 -0.67%) is down -0.84% at a 5-3/4 month low on fund selling and demand concerns. The CEO of the CVR Refinery in Coffeyville, Kansas, said that the refinery may be closed for four weeks because of damage from a fire. The refinery uses crude from Cushing, Oklahoma, and a prolonged shutdown of the refinery will curb demand and lead to increased stockpiles at Cushing. Sep gasoline (RBU14 -0.16%) is down -0.34%. Dec gold (GCZ14 +0.14%) is up +0.23%. Sep copper (HGU14 -0.50%) is down -0.39%. Agriculture and livestock prices are mostly lower. The dollar index (DXY00 +0.04%) is up +0.01%. EUR/USD (^EURUSD) is up +0.04%. USD/JPY (^USDJPY) is up +0.15%. Sep T-note prices (ZNU14 -0.09%) are down -5 ticks.

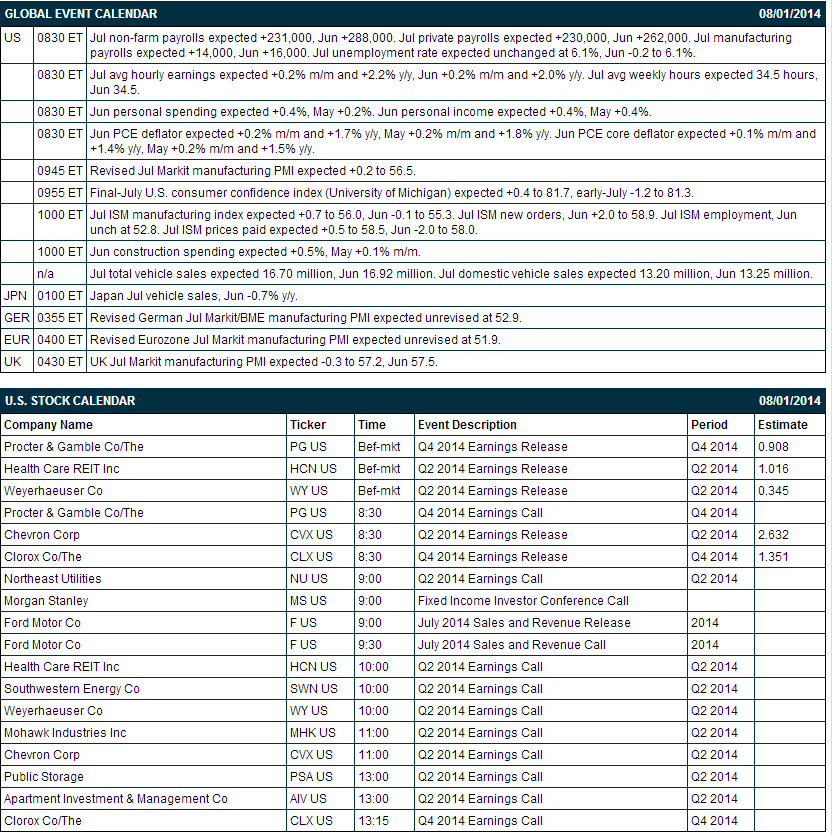

The China Jul manufacturing PMI rose +0.7 to 51.7, stronger than expectations of +0.4 to 51.4 and the fastest pace of expansion in 2-1/4 years.

The German Jul Markit/BME manufacturing PMI was revised downward to 52.4 from the originally reported 52.9.

The Eurozone Jul Markit manufacturing PMI was revised lower to match Jun's 8-month low of 51.8 from the originally reported 51.9.

The UK Jul Markit manufacturing PMI fell -1.8 from a downward revised 57.2 in Jun (originally reported 57.5) to 55.4, weaker than expectations of -0.3 to 57.2 and the slowest pace of expansion in a year.

U.S. STOCK PREVIEW

The market is expecting today’s July payrolls to show a solid increase of +231,000, which would be the sixth consecutive month of payroll increases in excess of +200,000. The market is expecting today’s July unemployment rate to be unchanged from June’s 6-year low of 6.1%, the lowest level since July 2008. The market is expecting today’s July ISM manufacturing index to show a +0.7 point increase to 56.0, more than overcoming June’s -0.1 point decline to 55.3. Today’s June PCE deflator, which is the Fed’s preferred inflation measure, is expected to ease slightly to +1.7% y/y from +1.8% in May. Meanwhile, the June core PCE deflator is expected to ease to +1.4% y/y from +1.5% in May. Today’s final-July U.S. consumer confidence index from the University of Michigan is expected to show an increase of +0.4 to 81.7 from the early-July level of 81.3. Today’s July total vehicle sales report is expected to ease to 16.70 million units from 16.92 million units in June.

There are 5 of the S&P 500 companies that report earnings today: Procter & Gamble (consensus $0.91), Health Care REIT (1.02), Weyerhaeuser (0.35), Chevron (2.63), Clorox (1.35). There are no equity conferences today.

OVERNIGHT U.S. STOCK MOVERS

Procter & Gamble (PG -1.07%) reported Q4 EPS of 95 cents, better than consensus of 91 cents.

Live Nation (LYV -2.68%) reported Q2 EPS of 11 cents, below consensus of 15 cents.

Boyd Gaming (BYD -2.40%) reported Q2 adjusted EPS of 5 cents, weaker than consensus of 8 cents.

DaVita (DVA -1.23%) reported Q2 adjusted EPS of 95 cents, stronger than consensus of 89 cents.

Insight Enterprises (NSIT -4.47%) reported Q2 EPS ex-items of 74 cents, better than consensus of 72 cents.

ON Semiconductor (ONNN -2.84%) reported Q2 EPS of 20 cents, better than consensus of 19 cents.

Fluor (FLR -2.89%) reported Q2 EPS of $1.02, higher than consensus of 99 cents.

Mohawk (MHK -1.54%) reported Q2 EPS ex-items of $2.21, better than consensus of $2.20.

Genpact (G -0.17%) reported Q2 adjusted EPS of 27 cents, better than consensus of 26 cents.

Montpelier Re (MRH +0.10%) was downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Tesla (TSLA -2.46%) climbed 4% in after-hours trading after it reported Q2 EPS of 11 cents, nearly three times consensus of 4 cents.

Western Union ({=WU reported Q2 EPS of 36 cents, right on consensus, although Q2 revenue of $1.41 billion was slightly below consensus of $1.42 billion.

Outerwall (OUTR +2.40%) reported Q2 core EPS of $1.42, higher than consensus of $1.36.

LinkedIn (LNKD -3.55%) jumped over 5% in after-hours trading after it reported Q2 adjusted EPS of 51 cents, better than consensus of 39 cents, and then raised guidance on fiscal 2014 adjusted EPS to approximately $1.80, higher than consensus of $1.64.

Expedia (EXPE -2.77%) rose over 4% in after-houre trading after it reported Q2 EPS of $1.03, much higher than consensus of 76 cents.

Edison International (EIX -1.76%) reported Q2 adjusted EPS of $1.08, well above consensus of 83 cents.

MARKET COMMENTS

Sep E-mini S&Ps (ESU14 -0.58%) this morning are down -11.00 points (-0.57%) at a 1-3/4 month low. The S&P 500 index on Thursday plunged to a 1-1/4 month low and closed sharply lower: S&P 500 -2.00%, Dow Jones -1.88%, Nasdaq -2.10%. Negative factors included (1) Argentine debt concerns after S&P said Argentina was in default after it missed an interest payment on $13 billion of debt, (2) the unexpected -10.0 point decline in the Chicago Jul PMI to a 13-month low of 52.6, weaker than expectations of +0.4 to 63.0, and (3) concern that labor costs may be on the rise after the +0.7% in the Q2 employment cost index, higher than expectations of +0.5% and the fastest growth rate in 5-3/4 years.

Sep 10-year T-notes (ZNU14 -0.09%) this morning are down -5 ticks. Sep 10-year T-note futures prices on Thursday posted a 3-week low but pared most of their losses and closed just slightly lower. Bearish factors included (1) technical selling with the 3-week low, and (2) the +0.7% increase in the U.S. Q2 employment cost index, the most in 5-3/4 years. T-notes recovered from their worst levels after the a plunge in stocks boosted safe-haven demand for T-notes. Closes: TYU4 -1.50, FVU4 +1.00.

The dollar index (DXY00 +0.04%) this morning is up +0.009 (+0.01%). EUR/USD (^EURUSD) is up 0.0006 (+0.04%) and USD/JPY (^USDJPY) is up +0.15 (+0.15%). The dollar index on Thursday rose to a 10-1/2 month high and closed higher. Bullish factors included (1) increased safe-haven demand after the S&P 500 plunged to a 1-1/4 month low, and (2) weakness in EUR/USD on speculation the ECB may expand stimulus measures after Eurozone Jul CPI unexpectedly weakened to +0.4% y/y, lower than expectations of unch at +0.5% y/y and the slowest growth rate in 4-3/4 years. Closes: Dollar index +0.024 (+0.03%), EUR/USD -0.00067 (-0.05%), USD/JPY unch.

Sep WTI crude oil (CLU14 -0.67%) this morning is down -82 cents (-0.84%) at a 5-3/4 month low and Sep gasoline (RBU14 -0.16%) is down -0.0094(-0.34%). Sep crude and gasoline prices on Thursday closed sharply lower with Sep crude at a 2-week low and Sep gasoline at a 3-1/2 month low: CLU4 -2.10 (-2.09%), RBU4 -0.0345 (-1.23%). Bearish factors included (1) the rally in the dollar index to a 10-1/2 month high, and (2) negative carry-over from Wednesday’s EIA data that showed a +789,000 bbl increase in EIA distillate inventories to a 10-month high and a +365,000 bbl increase in gasoline inventories to a 4-month high.

Disclosure: None