Morning Call For April 8, 2015

OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps this morning are little changed as the market awaits today's FOMC meeting minutes. The Euro Stoxx 50 index is down -0.39% after yesterday's rally. European energy stocks are trading higher on M&A optimism after today's blockbuster deal in oil and gas with Shell buying BG Group to gain access in particular to LNG in Australia and deep-water oil in Brazil. Asian stocks today closed mostly higher: Japan +0.76%, Hong Kong +3.80%, China +0.84%, Taiwan -0.73%, Australia +0.59%, Singapore -0.14%, South Korea +0.63%, India +0.67%, Turkey +0.24%.

The dollar index is down -0.43 points (-0.44%) on a turn-around after the sharp 2-session rally. EUR/USD is up +0.0055 (+0.51%) and USD/JPY is down -0.57 (-0.47%). Jun 10-year T-note prices up 5.5 ticks going into today's 10-year T-note auction.

Commodity prices are down -0.12% this morning due to lower energy prices. May crude oil is down -1.17 (-2.17%), May gasoline is down -0.0460 (-2.47%), and May natural gas is down -0.049 (-1.83%). The market is expecting today's weekly EIA report to show a +3.0 million bbl increase in crude oil inventories, a -2.0 million bbl decline in gasoline inventories, a +800,000 bbl increase in distillate inventories, and a +0.6 point increase in the refinery utilization rate to 90.0%. The market is hoping for U.S. oil production to decline for the second straight week.

Precious metals prices are little changed this morning with Jun gold up +0.1 (+0.01%) and May silver up +0.010 (+0.06%). May copper is down -0.012 (-0.43%). Grain prices are narrowly mixed this morning as the market awaits Thursday's WASDE report: May corn +0.25 (+0.07%), May soybeans +0.50 (+0.05%), May wheat -0.50 (-0.10%). Softs are trading higher this morning.

The Bank of Japan today left its monetary policy unchanged, which was in line with market expectations. The BOJ left its target unchanged of expanding the monetary base at an annual rate of 80 trillion yen ($670 billion). BOJ Governor Kuroda said that the Japanese economy now faces less risk than last year when the BOJ expanded its stimulus measures.

Today's U.S. MBA mortgage applications report showed an overall +0.4% increase with the purchases sub-index up +6.8% but the refinancing sub-index down -3.3%.

U.S. STOCK PREVIEW

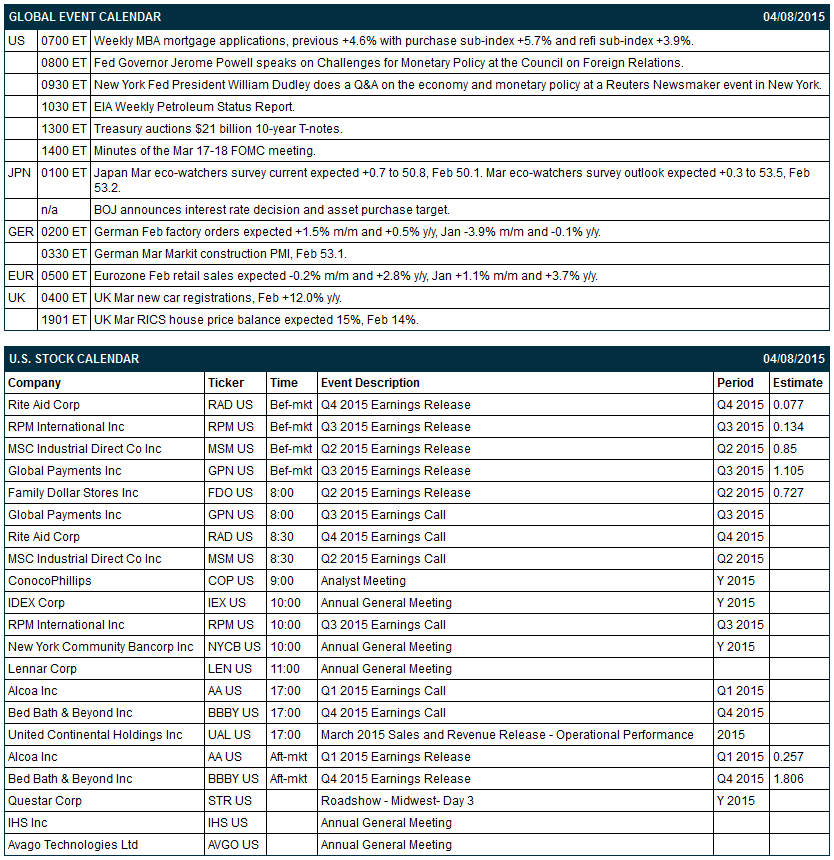

Key news today includes (1) the weekly MBA mortgage applications report (last week +4.6% with purchase sub-index +5.7% and refi sub-index +3.9%), (2) the minutes from the Mar 17-18 FOMC meeting, (3) the Treasury's auction of $21 billion of 10-year T-notes, (4) a speech by Fed Governor Jerome Powell on the “Challenges for Monetary Policy” at the Council on Foreign Relations, and (5) a Q&A on the economy and monetary policy by New York Fed President William Dudley at a Reuters Newsmaker event in New York.

There are seven of the Russell 1000 companies that report earnings today: Alcoa (consensus $0.26), Rite Aid (0.08), RPM International (0.13), MSC Industrial Direct (0.85), Global Payments (1.11), Family Dollar Stores (0.73), Bed, Bath & Beyond (1.81).

There are no U.S. IPO's that scheduled to price or trade today.

Equity conferences this week include: Internet of Things (IoT) Asia 2015 on Wed-Thu, and JP Morgan Spring Fling Conference on Thu

June E-mini S&Ps this morning are little changed as the market awaits today's FOMC meeting minutes. Tuesday's closes: S&P 500 -0.21%, Dow Jones -0.03%, Nasdaq -0.14%. The stock market on Tuesday fell on concerns that the strong JOLTS job openings report (+168,000 to a new 14-year high) might bring forward a Fed rate hike, as well as concern about a weak Q1 earnings season that starts today. On the positive side, the continued rally in oil prices boosted petroleum stocks.

OVERNIGHT U.S. STOCK MOVERS

- Shell (RDSN LN) announced an agreement to take over BG Group (BG LN) for about $70 billion in cash and shares in the largest oil and gas deal in at least a decade, with particularly attractive assets in Australian LNG and Brazilian deep water oil.

- Rite Aid (RAD -1.70%) reported Q4 EPS ex-items at 12 cents, better than the consensus of 7 cents.

- IMAX ({=IMAX) and Disney (DIS -0.19%) renewed their exhibition agreement with a new multi-picture deal.

- Kinder Morgan (KMI +0.05%) was downgraded to Buy from Conviction Buy at Goldman Sachs.

- New Residential (NRZ +2.99%) was added to the Top Picks list at FBR Capital.

- Dave & Buster's (PLAY -1.45%) rallied 1% in after-hours trading on better than expected earnings results.

- Regulus Therapeutics (RGLS -2.68%) rallied 10% in after-hours trading after one of its products was selected as clinical candidate by AstraZeneca (AZN +0.24%)

- OHR Pharmaceutical (OHRP +8.37%) rallied 2% in after-hours trading after a report that Broadfin purchased a 6.1% stake in the company.

- Pentair (PNR -1.87%) fell 4% in after-hours trading after lowering its Q1 guidance.

MARKET COMMENTS

Jun 10-year T-note prices up 5.5 ticks going into today's 10-year T-note auction. June 10-year T-notes on Tuesday closed mildly lower on the much stronger-than-expected JOLTS job openings report and the continued rally in crude oil prices, which is boosting inflation expectations. T-notes are also seeing supply pressure during this week's sale of $58 billion of 3-year, 10-year and 30-year securities.

The dollar index is down -0.43 points (-0.44%) on a turn-around after the sharp 2-session rally. EUR/USD is up +0.0055 (+0.51%) and USD/JPY is down -0.57 (-0.47%). Tuesday's closes: Dollar index +1.15 (+1.19%), EUR/USD -0.0108 (-0.99%), USD/JPY +0.74 (+0.62%). The dollar index on Tuesday closed sharply higher on the much stronger-than-expected JOLTS job openings report. In addition, the continued rally in crude oil prices is boosting inflation expectations, which could cause the Fed to accelerate its rate hike.

May crude oil is down -1.17 (-2.17%), May gasoline is down -0.0460 (-2.47%), and May natural gas is down -0.049 (-1.83%). Tuesday's closes: CLK5 +1.11 (+2.13%), RBK5 -0.0119 (-0.65%). May crude oil prices on Tuesday rallied sharply on ideas that U.S. oil production might finally be slowing due to the plunge in the number of operating U.S. oil rigs. U.S. oil production fell last week and the market suspects that production may fall again in Wednesday's EIA report. Crude oil prices are also seeing support as the Iranian nuclear agreement is meeting with heavy opposition from Israel and with political opposition in Washington. On the negative side, the market is expecting Wednesday’s weekly EIA report to show a +3.0 mln bbl gain in U.S. crude oil inventories.

Click on picture to enlarge

Disclosure: None.