Morning Call - 11/11/2014

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ14 +0.17%) this morning are up +0.07% at a fresh record high on optimism the U.S. economy can weather a global slowdown and the end of the Fed's bond purchases. European stocks are up +0.47% as Vodafone Group Plc led telecommunications companies higher on better-than-expected quarterly earnings results. Asian stocks closed mixed: Japan +2.05%, Hong Kong +0.27%, China -0.28%, Taiwan -0.18%, Australia -0.12%, Singapore -0.27%, South Korea -0.08%, India +0.13%. Japanese exporters led a rally in the Nikkei Stock Index to its best level in 7 years after the yen sank to a new 7-year low against the dollar, which boosts the earnings prospects of Japanese exporters. China's Shanghai Stock Index pushed up to a nearly 3-year high before the start of an exchange link with Hong Kong next week. Profit-taking set in near the highs, however, and the Shanghai Stock Index shed its advance and closed lower. Commodity prices are mostly lower. Dec crude oil (CLZ14 -0.27%) is down -0.49%. Dec gasoline (RBZ14 -0.64%) is down -0.84%. Dec gold (GCZ14 -0.47%) is down -0.42%. Dec copper (HGZ14 -0.73%) is down -0.86%. Agriculture prices are mostly lower. The dollar index (DXY00 +0.11%) is up +0.16%. EUR/USD (^EURUSD) is unchanged. USD/JPY (^USDJPY) is up +0.88% at a 7-year high amid reports from Japan's Yomiuri newspaper that Japanese Prime Minister Abe is considering postponing a planned sales-tax increase and preparing to call a snap election next month to shore up support for his fiscal policies. Dec T-note prices (ZNZ14 -0.05%) are down -1.5 ticks. The U.S. cash Treasury market is closed today for Veterans Day.

ECB Executive Board member Mersch said that the Eurozone recovery has lost momentum and that the ECB will begin to buy asset-backed securities next week as part of a stimulus plan. He added that "there hasn't been a decision yet by the ECB to buy government bonds but it is a theoretical option if the situation deteriorates."

The UK Oct BRC sales like-for-like sales monitor was unchanged y/y, an improvement from the -2.1% y/y decline in Sep and better than expectations of-0.5% y/y.

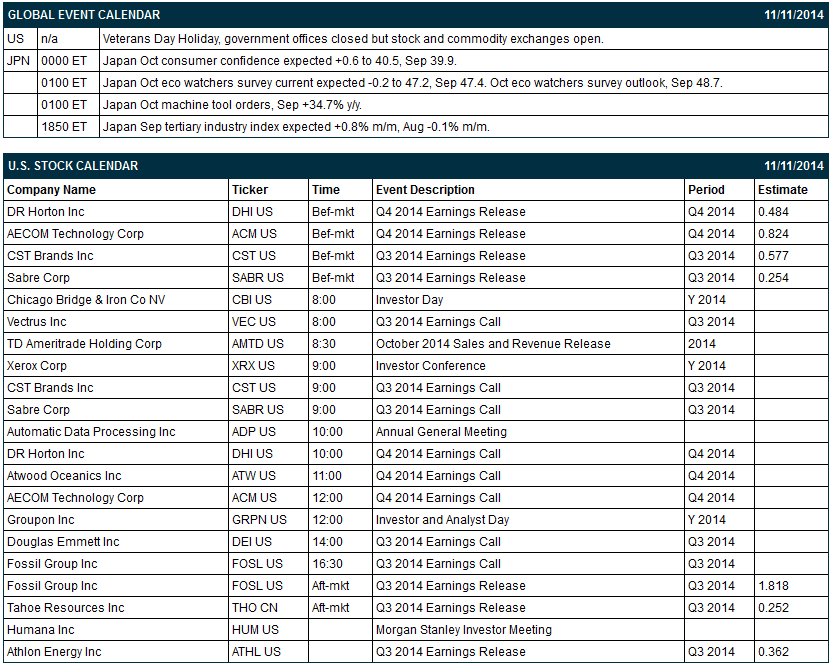

Japan Oct consumer confidence unexpectedly fell -1.0 point to 38.9, weaker than expectations of +0.6 to 40.5 and the lowest in 6 months.

The Japan Oct eco watchers survey current fell -3.4 to 44.0, a larger decline than expectations of -0.2 to 47.2 and the lowest in 6 months. The Oct eco watchers survey outlook fell -2.1 to 46.6, the lowest in 7 months.

Japan Oct machine tool orders rose +31.2% y/y, less than the +34.7% y/y increase in Sep, but still the thirteenth consecutive month that machine tool orders have increased year-over-year.

Japan Oct bankruptcies fell -16.57% y/y, an improvement from the +0.85% y/y increase in Sep and the largest decline in 5 months.

U.S. STOCK PREVIEW

There are no U.S. economic reports today. The U.S. government is closed today for the Veterans Day holiday. There are 2 of the S&P 500 companies that report earnings today: DR Horton (consensus $0.48), Fossil Group (1.82).

Equity conferences today include: Robert W. Baird & Co. Inc Industrial Conference on Mon-Tue, Airshow China 2014-Media Days on Mon-Tue, RBC Technology, Internet, Media & Telecommunications Conference on Mon-Tue, Cowen and Company Global Metals, Mining and Materials Conference on Tue, Needham Next-Gen Storage/Networking Conference on Tue, Morgan Stanley Global Chemicals & Agriculture Conference on Tue-Wed, Stephens Inc Fall Investment Conference on Tue-Wed, Jefferies Global Energy Conference on Tue-Wed, Credit Suisse Health Care Conference on Tue-Thu, J.P. Morgan Ultimate Services Investor Conference on Wed, Mexico Investors Forum 2014 on Wed, Pacific Crest Consumer Innovations Technology Investor Forum on Wed, Bank of America Merrill Lynch Banking & Financial Services Conference on Wed-Thu, Wells Fargo Securities Technology, Media & Telecom Conference on Wed-Thu, Goldman Sachs Global Industrials Conference on Wed-Thu, Bank of America Merrill Lynch Global Energy Conference on Wed-Fri, Edison Electric Institute Financial Conference on Thu, UBS Building & Building Products CEO Conference on Thu, SunTrust Robinson Humphrey Financial Technology, Business & Government Services on Thu, NOAH Conference 2014 on Thu, Goldman Sachs Technology and Internet Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Darden (DRI +1.51%) was upgraded to 'Buy' from 'Hold' at KeyBanc.

DR Horton (DHI +1.30%) reported Q4 EPS of 45 cents, less than consensus of 48 cents.

Capital One (COF +0.77%) was downgraded to 'Neutral' from 'Buy' at Nomura.

Juniper (JNPR -1.87%) was upgraded to 'Buy' from 'Neutral' at Nomura.

Prudential Financial reported a 14.9% passive stake in Wayfair (W +8.04%) .

Select Equity Group reported a 10.8% passive stake in MRC Global (MRC -2.09%) .

Enstar Group (ESGR +1.27%) reported Q3 EPS of $1.37, weaker than consensus of $1.71.

Raging Capital reported a 10.2% passive stake in Townsquare Media (TSQ -0.64%) .

Morgan Stanley reported a 8.6% passive stake in 500.com (MS +5.44%) .

Glenview Capital reported a 6.03% passive stake in Cadence Design (CDNS +0.86%) .

Woodward (WWD +0.45%) reported Q4 EPS of 77 cents, below consensus of 78 cents.

Cumulus Media (CMLS -3.24%) reported Q3 EPS of 1 cent, well below consensus of 7 cents.

Halcon Resources (HK +0.31%) fell over 7% in after-hours trading after it reported Q3 EPS of 3 cents, only half as much as consensus of 6 cents.

Caesar's (CZR -4.63%) slumped over 7% in after-hours trading after it reported a Q3 EPS loss of -$6.29, a much bigger loss than consensus of -$1.47.

Rackspace (RAX -0.29%) rose over 3% in after-hours trading after it reported Q3 EPS of 18 cents, better than consensus of 16 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ14 +0.17%) this morning are up +1.50 points (+0.07%) at a record high. The S&P 500 index on Monday rose to a fresh record high and closed higher: S&P 500 +0.31%, Dow Jones +0.23%, Nasdaq +0.37%. Bullish factors included (1) carry-over support from a rally in China’s Shanghai Stock Index to a 2-1/2 year high after China Oct exports rose +11.6% y/y, better than expectations of +10.6% y/y, and after regulators set a date for an exchange link between Shanghai and Hong Kong bourses that will allow trading on each other’s stock exchanges and give foreign investors unprecedented access to China’s equity markets, and (2) carry-over strength from a rally in European equity markets after the Eurozone Nov Sentix investor confidence unexpectedly climbed +1.8 to -11.9, better than expectations of -0.1 to -13.8.

Dec 10-year T-notes (ZNZ14 -0.05%) this morning are down -1.5 ticks. Dec 10-year T-note futures prices on Monday retreated from a 1-1/2 week high and closed lower: TYZ4 -12.50, FVZ4 -7.75. Bearish factors included (1) reduced safe-haven demand for T-notes after the S&P 500 climbed to a new all-time high and (2) supply pressures due to the Nov quarterly refunding as the Treasury auctions $66 billion of T-notes and T-bonds this week.

The dollar index (DXY00 +0.11%) this morning is up +0.139 (+0.16%). EUR/USD (^EURUSD) is unch. USD/JPY (^USDJPY) is up +1.01 (+0.88%) at a new 7-year high. The dollar index on Monday closed higher. Closes: Dollar index +0.168 (+0.19%), EUR/USD -0.00331 (-0.27%), USD/JPY +0.288 (+0.25%). The main bullish factor for the dollar is speculation that the Fed will still raise interest rates even after Friday’s payroll report showed a smaller-than-expected increase in U.S. Oct non-farm payrolls. Bearish factors for the dollar included (1) the unexpected increase in the Eurozone Nov Sentix investor confidence, which was EUR/USD supportive, and (2) the rally in the S&P 500 to a new record high.

Dec WTI crude oil (CLZ14 -0.27%) this morning is down -38 cents (-0.49%) and Dec gasoline (RBZ14 -0.64%) is down -0.0176 (-0.84%). Dec crude and Dec gasoline on Monday fell back from 1-week highs and closed lower. Closes: CLZ4 -1.25 (-1.59%), RBZ4 -0.0341 (-1.60%). Bearish factors included (1) dollar strength, and (2) concern that OPEC is in no hurry to cut output to reverse a slide in crude prices after Kuwait Oil Minister Ali Al-Omair said “I don’t expect there will be any cut in oil production” when the cartel meets later this month.

Disclosure: None