More Returns

The long-line of unwanted gifts returned after the holidays has already happened in the US and Europe, but for China its another story. The return of China to markets has been greeted with rising hopes for the US/China talks in Beijing, more stimulus from the government and more global growth spillovers. The push ahead for risk met a few headline glitches with the UK being the focus for less rather than more as its GDP fell in December and its monthly data highlighted the concerns that led the BOE to flip on its forecasts and rate path. More returns in equities don’t mean more pain in bonds as this is a week for geopolitical uncertainty ending with the risk of a US government shutdown Friday, starting today with these headlines:

- China Lunar New Year retail sales rose 8.5% y/ to CNY1.005trn linked to foods, electronics gifts – but still lowest rate since 2011. Sales in 2018 were up 10.2%. Tourism was up 8.2% to CNY513.9bn after a 12.1% gain in 2018 with trips up 7.6% to 415mn. The China Economic Information Daily suggested 1Q GDP is set to reach 6%with 2019 full year 6.3%.

- Thailand election panel disqualifies Princess as PM candidate. This puts an end to a short-lived campaign and backs up the King’s intervention.

- UK May rejects Brexit customs union compromise, dashing hopes for Labour Party support.

The UK was clearly the news focus and least interesting trade in FX again. The EUR/USD dip below 1.13 despite US politics underscores the problems with rates driving FX. The GBP/USD relationship is still worth watching given the failure of the recent breakout. On the day, the FX markets were all about safe-haven reversals with Japan on holiday and a test of the 110.20-40 resistance underway. For CHF it was a mini-flash crash as 1.0070 led to a stopfest test of 1.01 which quickly reversed. The world of FX and thin markets may be telling us something larger and more important about risk-on and off for today watching .9925 for troubled returns.

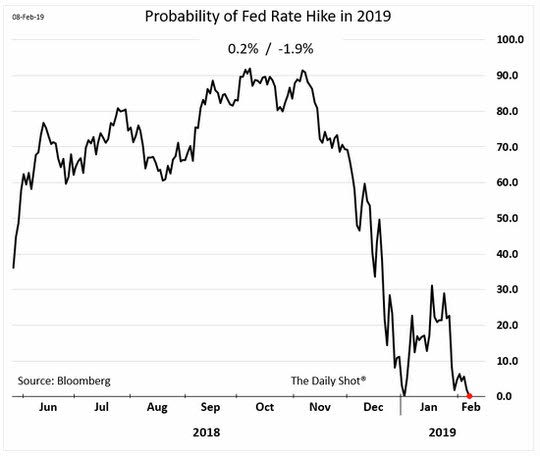

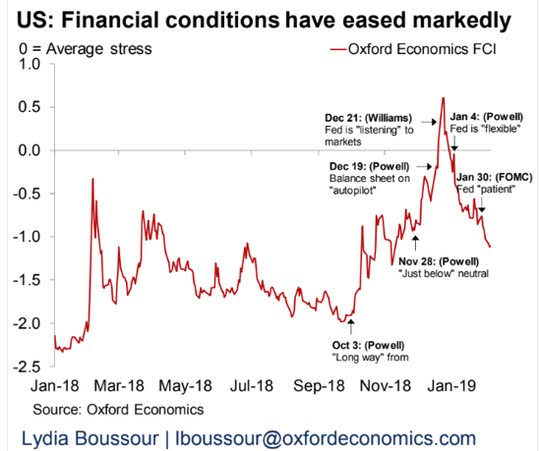

Question for the Day:Is the market confusing the patience of the FOMC with financial conditions? The return of China to markets mattered more than the news today. The push up in China shares helps spur talk that the US and China will come to a deal before the March 1 deadline. Whether that happens is clearly in play and the driver for volatility. The risk-off and on games are not easy to play and the only thing that really changed from last week was mood with the view that financial conditions drove the FOMC to shift to a patient stance but perhaps the markets are over estimating the willingness of Powell to push equities dramatically higher.

The off-set of a S&P500 gain is that the financial conditions move too much and make the FOMC uncomfortable. This is going to be the key for moderating markets this week.

What Happened?

- China January FX Reserves rise $15.2bn to $3.088trn after $11bn gain – more than the$9.3bn expected – biggest jump in a year. The gain was mostly due to non-dollar currency gains and asset price appreciation. The CNY gained 2.6% against the USD in January. The value of China’s gold reserves rose to $79.319 billion from $76.331 billion at the end of December.

- Sweden December industrial production rose 1.8% m/m, 2.6% y/y after revised +1.1% y/y - best since August. The manufacturing output rose 2.7% y/y from 1.3% y/y, while mining fell 2.6% after -1%.

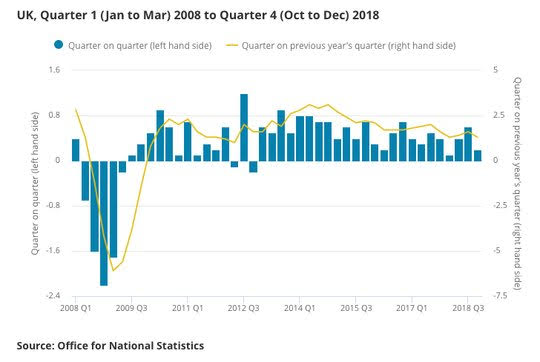

- UK 4Q preliminary GDP 0.2% q/q 1.3% y/y after 0.6% q/q, 1.6% y/y – weaker than the 1.4% y/y expected. The monthly December GDP -0.4% m/m, 1% y/y after +0.2% m/m, 1.5% y/y – also weaker than the 0% m/m, 1.4% y/y expected – bringing the 3M average down to 0.2% from 0.3% q/q. Business investment -1.4% q/q after -1.2% q/q. Trade also hurt growth while private and government consumption supported it. For all of 2018, GDP was 1.4% - the slowest growth rate since 2009.

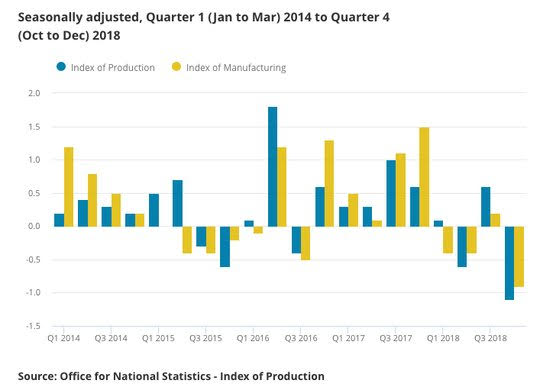

- UK December industrial production -0.5% m/m, -0.9% y/y after revised -0.4% m/m, -1.3% y/y (pre -1.5%) – weaker than the +0.2% m/m, -0.4% y/y expected. The manufacturing output -0.7% m/m, -2.1% y/y after revised -0.1% m/m, -1.2% y/y (pre -1.1%) – also weaker than -1.1% y/y expected – with weakness in 9 of 13 subsectors led by pharmaceuticals. The separate construction output also weaker -2.4% y/y after revised 1.8% y/y (pre 3% y/y) – worse than +1.5% y/y expected.

- UK December trade deficit narrows to GBP0.32bn from GBP0.36bn- with imports slowing. Imports fell 1.6% to GBP55.85bn and Exports fell 1% to GBP52.62bn, but for the 4Q the deficit widened to GBP10.4bn from GBP9.5bn – mostly due to imports up GBP1.5bn to GBP169.3bn with cars, chemicals and materials. Total exports were GBP159bn. For all of 2018 the trade deficit rose to GBP32.3bn.

Market Recap:

Equities: The US S&P500 futures are up 0.3% after 0.07% gain Friday. The Stoxx Europe 600 is up 0.75% with Italy leading. The MSCI Asia Pacific rose 0.7% with Japan on holiday, China returning to market bid.

- Japan Nikkei closed for holiday

- Korea Kospi up 0.17% to 2,180.73

- Hong Kong Hang Seng up 0.71% to 28,143.84

- China Shanghai Composite up 1.36% to 2,653.90

- Australia ASX off 0.12% to 6,128.60

- India NSE50 off 0.50% to 10,888.80

- UK FTSE so far up 0.55% to 7,111

- German DAX so far up 0.8% to 10,992

- French CAC40 so far up 0.9% to 5,006

- Italian FTSE so far up 1.6% to 19,662

Fixed Income: Risk on and bonds off – but not enough to matter much – German 10-year Bund yields up 3bps to 0.11%, French OATs up 2bps to 0.56%, Gilts up 3bps to 1.18% while periphery recovers, Italy off 7bps to 2.91%, Spain off 1bps to 1.24%, Portugal flat at 1.67% and Greece off 1bps to 4.00%.

- US Bonds are lower waiting for data/Fed speakers– 2Y up 1bps to 2.47%, 5Y up 2bps to 2.46%, 10Y up 1bps to 2.65% and 30Y up 1bps to 2.99%.

- Australian bonds mixed with risk-on, curve flattening– 3Y up 3bps to 1.64%, 10Y off 1bps to 2.09%.

- China bonds return bid– 2Y off 2bps to 2.63%, 5Y off 5bps to 2.87%, 10Y off 3bps to 3.09%.

Foreign Exchange: The US dollar index is up 0.1% to 96.73. In EM USD mostly bid – EMEA: ZAR off 0.8% to 13.731, RUB off 0.3% to 65.659, TRY off 0.3% to 5.264; ASIA: INR flat at 71.164, KRW off 0.1% to 1124.4.

- EUR: 1.1315 flat. Range 1.1297-1.1330 with 1.13 still pivot for 1.1180 and rates driving.

- JPY: 110.15 up 0.4%.Range 109.76-110.28 with EUR/JPY 124.65 up 0.35%. Holiday thin market puts 110.20-40 resistance into play.

- GBP: 1.2930 off 0.1%.Range 1.2894-1.2940 with EUR/GBP .8755 up 0.05% - focus is still about Brexit and UK May politics. 1.28-1.3050 keys

- AUD: .7085 flat. Range .7081-.7108 with China return not enough for bounce – NZD .6750 up 0.15% - with government poll key.

- CAD: 1.3275 flat.Range 1.3264-1.3297 with focus on oil, data, rates. 1.32-1.3350 keys.

- CHF: 1.0030 up 0.3%.Range .9982-1.0099 – Asia flash crash triggered 1.0070 stops - EUR/CHF 1.1350 up 0.15%.

- CNY: 6.7880 up 0.65%.Range 6.742-6.7920 with focus on 6.75 and 6.78 breaks for 6.83 next.

Commodities: Oil lower, gold lower, Copper up 0.45% to $2.8170

- Oil: $52.31 off 0.8%.Range $51.82-$52.78 with oil lower despite OPEC push as global growth remains in doubt - $52 pivot for $50 or $54. Brent off 0.2% to $61.97 with $62 the same for $60 or $64.

- Gold: $1311.30 off 0.55%. Range $1309.60-$1318.70 with safe-haven demand lower and $1305 still key base. Silver off 0.5% to $15.73, platinum off 1% to $794.70 and Palladium off 0.4% to $1365.50

Economic Calendar:

- 1100 am US Jan consumer inflation expectations 3%p 3%e

- 1115 am Fed Bowman speech

- 1130 am US sells 3M and 6M bills

View TrackResearch.com, the global marketplace for stock, commodity and macro ideas here.