Markets: Losing?

The second time is not a charm. The sense of déjà vu in regards to Brexit headlines and UK Prime Minister May dominates markets today as the stakes for global growth remain critical for investors. Losing 391 to 242 on her plan leaves Parliament to vote next on whether to leave the EU without a deal affectionately called a hard-Brexit. This is seen as unlikely and that leaves Thursday open for a vote to request a delay in Article 50, requiring EU acceptance as well, a process, which many see as opening the door for another referendum and UK election. The timeline effectively clouds all other event risks – like the UK Spring Budget or the US durable goods orders and maybe even the China retail sales, industrial production and fixed investment economic releases ahead. The bigger picture maybe in markets losing interest as volatility drops, as carry trades return and as waiting for bad news stories proves boring until new events emerge like a US/China trade deal unraveling or US imposing auto tariffs on the EU. The other losing story is about Boeing as the Ethiopia Air Flight 302 crash has led much of the world to ground the Max 8 plane with the US FAA standing out in its support for it’s safety. This is micro, not macro but makes clear that the big picture is not finished. The market sees hope in some US/China deal, some further China stimulus, some chance of no Brexit, some clarity from the myriad of elections ahead – Thailand, Spain and EU May elections – all in focus. The economic data releases overnight were mixed at best with better Korea jobs, worse Australian consumer confidence, weaker Japan machinery orders and better Eurozone industrial production. The lack of attention comes through in most markets with feeble ranges and volumes, making the only risk barometer of note to remain the GBP. When you look at the GBP chart you see whispers of hopes for a breaking to 1.36 as the best-case scenario of no Brexit continues to play forward on the markets. There are plenty of obstacles and reasons to doubt such an outcome but this remains the zero-sum nature of politics in the UK and the GBP where traders hope its either 1.25 and lower or 1.35 and higher in the next 48 hours.

Question for the Day: Is today really about politics or growth? The problem with Brexit on the global economy has been its chilling effect on EU and UK business investment. Uncertainty breeds contempt. The hope is for some clarity – even a bad outcome promotes some binary path forward rather than being stuck in limbo. Much of the worst pains from this uncertainty have been countered by the BOE and ECB policies. They have left money easy and talked forward their reactions to more difficult outcomes like a hard Brexit. There is the bigger issue behind uncertainty of politics beyond the UK and EU and that is the US/China trade talks. Informa’s work on uncertainty from politics on markets and growth is worth reading. Policy uncertainty is at the highest since 1997 and flows of capital are beginning to reflect this all.

The politics behind the UK Brexit are not unique and the speech to consider today comes from ECB supervisor Angeoloni. He noted that Italy’s recession was self-inflicted and a consequence of government economic policy choices. Angeloni told an event in Rome that rising bond yields in Italy were leading to tighter credit conditions and added that the economy would benefit from a drop in debt costs. This is the rub as central bankers continue to drive policy responses to politics, the risk of larger negative outcomes increases.

What Happened?

- Korea February unemployment 3.7% from 4.4% - better than 3.9% expected. The rate eases from 9-year highs back to summer 2018 levels. There were 263,000 new jobs added, the best since Jan 2018, with most of the new work in services.

- Australia March Westpac-MI consumer confidence fell 4.8% to 98.8 from 103.8 – weaker than 102.5 expected. This is the lowest level since Sep 2017. The components show house price expectations -2.7% m/m, -34.1% y/y, unemployment fears up 8.9% m/m, 7.2% y/y but house buying rose 3.5% m/m, 11.5% y/y. The outlook for economic conditions (12-month ahead) -6.9% m/m, -4.5% y/y and for 5Y ahead -5.5% m/m, -2.1% y/y.

- Japan January machinery orders -5.4% m/m, -2.9% y/y after +0.9% y/y weaker than the -1.7% m/m, -2.3% y/y expected. The Jan-Mar forecast is -0.9% compared to -3.2% for 4Q. Orders in Manufacturing -1.9% m/m after -4.4% while services -8% after +5%. The overseas orders -18.1% m/m after -18.1% m/m.

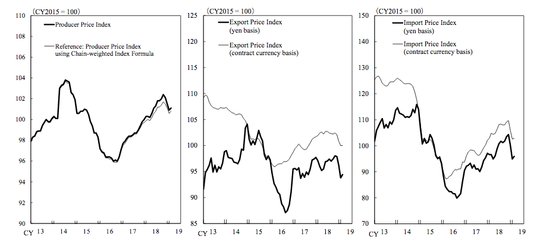

- Japan February PPI up 0.2% m/m, +0.8% y/y after -0.6% m/m, 0.6% y/y – more than the +0.1% m/m, 0.7% y/y expected. Export prices were 0% m/m, import prices rose 0.2% m/m. Oil and coal were the main drivers for higher PPI with electrical equipment (monitors/switches) the drag.

- Spain February final HICP unrevised at +0.2% m/m, 1.1% y/y after -1.7% m/m, 1% y/y – as expected. The national CPI rate +0.2% mm, 1.1% y/y after -1.3% m/m, 1% y/y – also as expected.

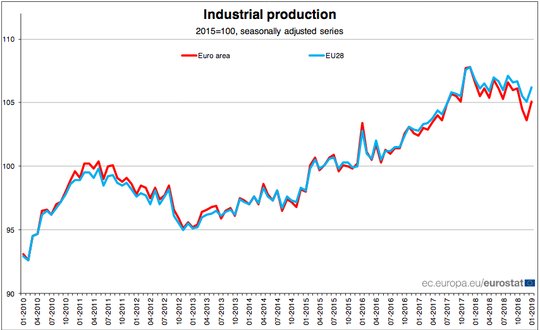

- Eurozone January industrial production jumps 1.4% m/m after -0.9% m/m – better than +1% expected. By sector, energy rose 2.4%, consumer goods 2%, durable goods 1.1%, capital goods 0.9% and intermediate goods 0.2%. The biggest national increase in the Eurozone was in Ireland 15.1%, while the weakest was Denmark -8.6%.

Market Recap:

Equities: The US S&P 500 futures are up 0.1% after a 0.3% gain yesterday. The Stoxx Europe 600 is up 0.1% while the MSCI Asia Pacific fell 0.5%.

- Japan Nikkei off 0.99% to 21,290.24

- Korea Kospi off 0.41% to 2,148.41

- Hong Kong Hang Seng off 0.39% to 28,807.45

- China Shanghai Composite off 1.09% to 3,026.95

- Australia ASX off 0.23% to 6,246.00

- India NSE50 up 0.36% to 11,342.35

- UK FTSE so far flat at 7,154

- German DAX so far off 0.15% to 11,509

- French CAC40 so far up 0.2% to 5,280

- Italian FTSE so far up 0.1% to 20,651

Fixed Income: More headlines on Brexit vs. better economic data mix to leave the E1bn 30Y Bund 1.25% sale at 0.74% with 1.47 cover with the previous sales E1.5bn with 1.23 cover and 0.72% result. That sales matters as investors talk about the Japanification of Europe and rates in 10Y being stuck at 0. The 10Y Bund yield is flat at 0.07% today while France is flat at 0.47% and UK Gilts are off 2bps to 1.18%. Periphery is mixed with Italy and its 3-7-30Y sale key focus (3Y flat at 0.72%0, 7Y up 1bps to 2.08%, 30Y up 2bps to 3.60%) – 10Y off 2bps to 2.56% while Portugal off 1pbs to 1.33%, Spain up 1bps to 1.19%, Greece off 1bps to 3.87%.

- US Bonds are mixed with curve flatting– 2Y up 1bps to 2.47%, 5Y up 1bpst to 2.42%, 10Y up 1bps to 2.62%, 30Y off 4bps to 2.99%.

- Japan JGBs rally with US into BOJ and weaker data– 2Y off 1bps -0.15%, 5Y off 1bps to -0.17%, 10Y off 1bps to -0.04%, 30Y off 2bps to 0.57%.

- Australian bonds rally on weak consumer confidence– 3Y off 6bps to 1.54%, 10Y off 6bps to 1.97% - breaking 2% is important – NZD 10Y off 5bps to 2.07% also watching 2% barrier.

- China bonds mixed with curve flatter- 2Y up 1bps to 2.79%, 5Y up 2bps to 3.04%, 10Y flat at 3.17%.

Foreign Exchange: The US dollar index 96.86 off 0.1%. In emerging markets – USD mixed with Asia: INR up 0.1% to 69.535, KRW off 0.4% to 1132.1; EMEA: RUB up 0.2% to 65.50, ZAR flat at 14.333 and TRY off 0.1% to 5.458.

- EUR: 1.1300 up 0.1%. Range 1.1277-1.1303 with better IP data, lower US yields driving – watching 1.1250-1.1380 again.

- JPY: 111.30 flat. Range 111.14-111.39 with EUR/JPY 125.75 up 0.1% despite weaker equities – focus is on BOJ, rates and 112 still.

- GBP: 1.3150 up 0.6%. Range 1.3057-1.3163 with EUR/GBP .8600 up 0.4% - all about no Brexit hopes.

- AUD: .7060 off 0.25%. Range .7049-.7082 with NZD .6840 off 0.3% - RBA rate cut expectations growing and US/China trade hopes key .7050 still a pivot with .6830 risk.

- CAD: 1.3360 flat. Range 1.3349-1.3371 with US rates driving and focus on 1.3320-50 $ support.

- CHF: 1.0055 off 0.2%. Range 1.0053-1.0085 with EUR/CHF 1.1365 off 0.1% all about risk mood and 1.00 base.

- CNY: 6.7095 flat. Range 6.7030-6.7120. PBOC fixed 6.7114 from 6.7128.

Commodities: Oil up, Gold up, Copper up 0.15% to $2.9510.

- Oil: $57.40 up 0.9%.Range $57.01-$57.50 with Brent up 0.65% to $67.10. API reported a surprise crude draw of 2.58mb when a 2.8mb build was expected, this helped oil rally into Asia despite equities – with focus on $58 and $68 resistance and IEA next, OPEC monthly.

- Gold: $1308.60 up 0.8%.Range $1300.60-$1309.40 with USD wobble, rates driving and focus next on $1320 then $1345 resistance. Silver $15.54 up 0.8%, Platinum $840.10 up 1%, and Palladium $1505.80 up 1.05%.

Economic Calendar:

- 0830 am UK Spring Budget 2019

- 0830 am US Feb PPI (m/m) -0.1%p 0.2%e (y/y) 2%p 1.9%e / core 2.6%p 2.6%e

- 0830 am US Jan durable goods orders (m/m) 1.2%p -0.7%e / ex trans 0.1%p 0.2%e

- 1000 am Mexico Jan industrial production (y/y) -2.5%p -2%e

- 1000 am US Jan construction spending (m/m) -0.6%p +0.4%e

- 1030 am US weekly EIA oil inventory 7.069mb p 1.203mb e

- 0100 pm US 30Y bond sale

- 0100 pm ECB Coure speech

View TrackResearch.com, the global marketplace for stock, commodity and macro ideas here.