Market Briefing For Wednesday, June 8, 2022

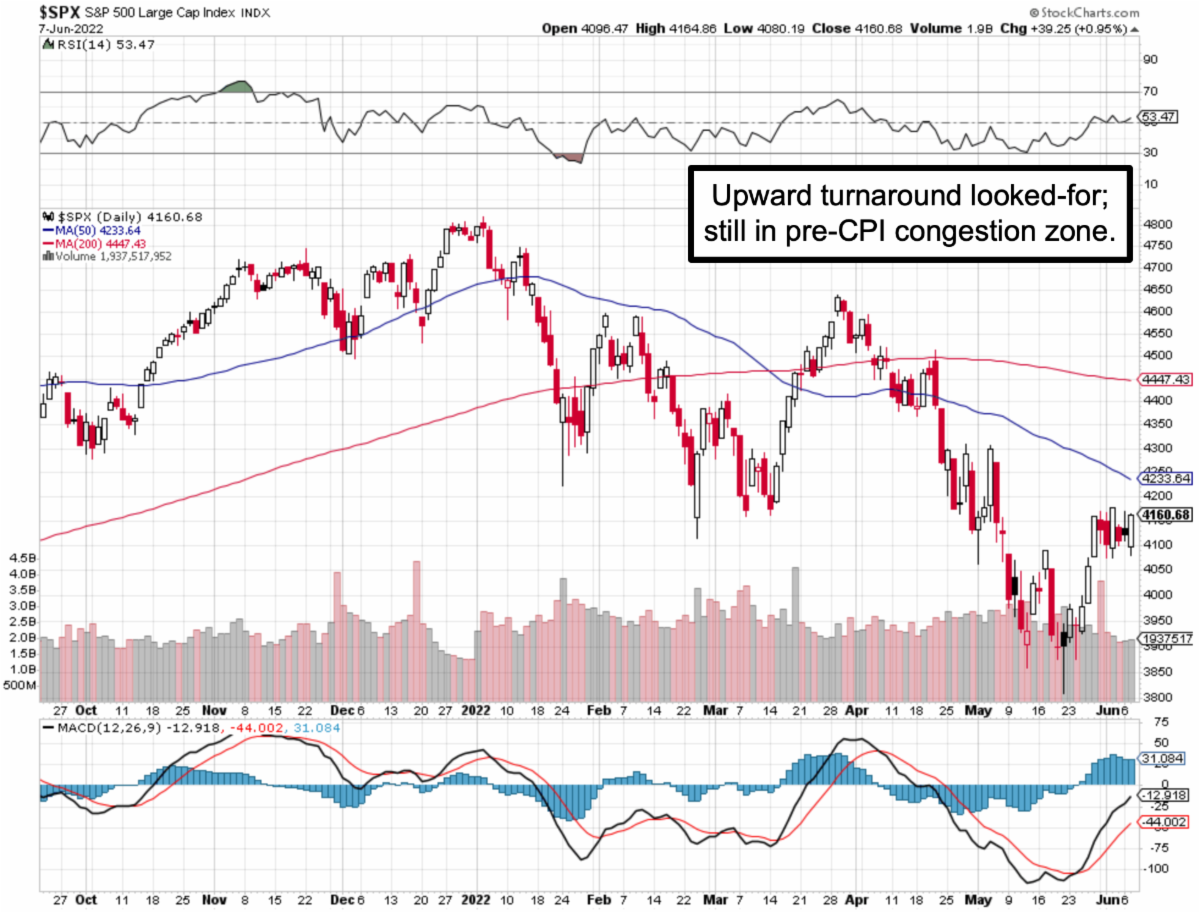

The 'stage was set' for an important rebound or relief rallies about 3 weeks ago as forecast and you have a bit better circumstances now. What I mean by that is that the washout began with a short-covering turnaround at the target on the downside near S&P 3800. And, aside the couple efforts to consolidate (such as Friday's sell-off), the broad market (not just S&P) has held decently.

Investors are sufficiently 'uncomfortable' that it actually assists S&P holding at this point, though mostly it's trading range action ahead of CPI on Friday, and it's smack in the middle of our 4100-4200 S&P target the projected rebound.

In this case you're not going to have any drop in interest rates, real wages will remain less impressive than people perceive, due to the huge inflation, and so the market is behaving decently, given the global variables, which includes an expectation (I mentioned last week) of ECB hiking rates, even though there is clearly a Euromean 'stagflation' condition (likely here too, unacknowledged).

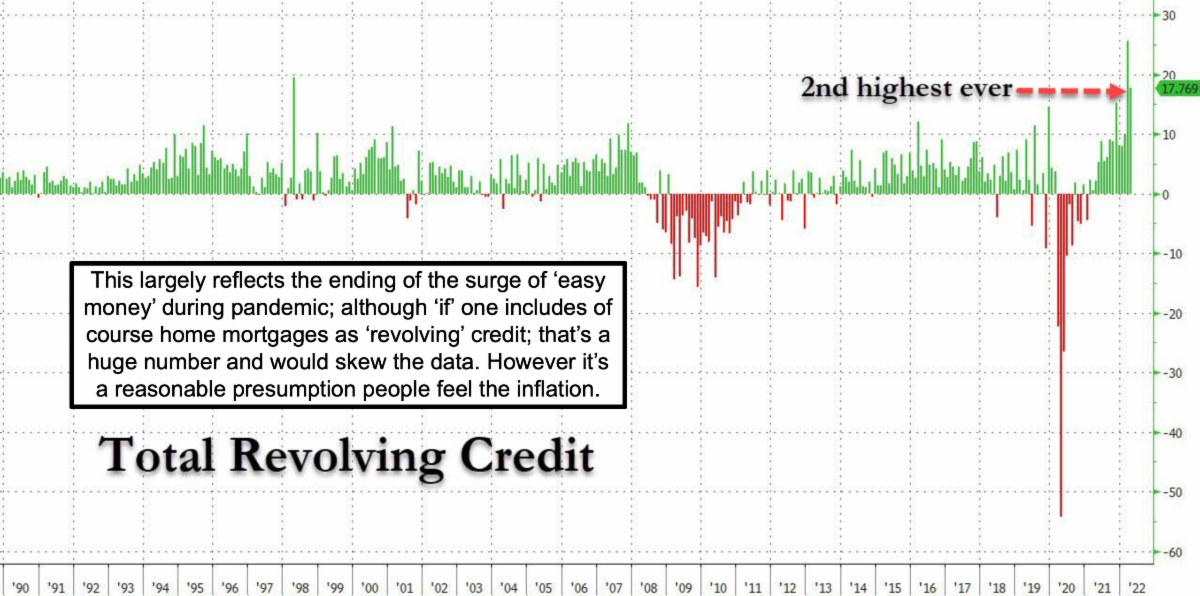

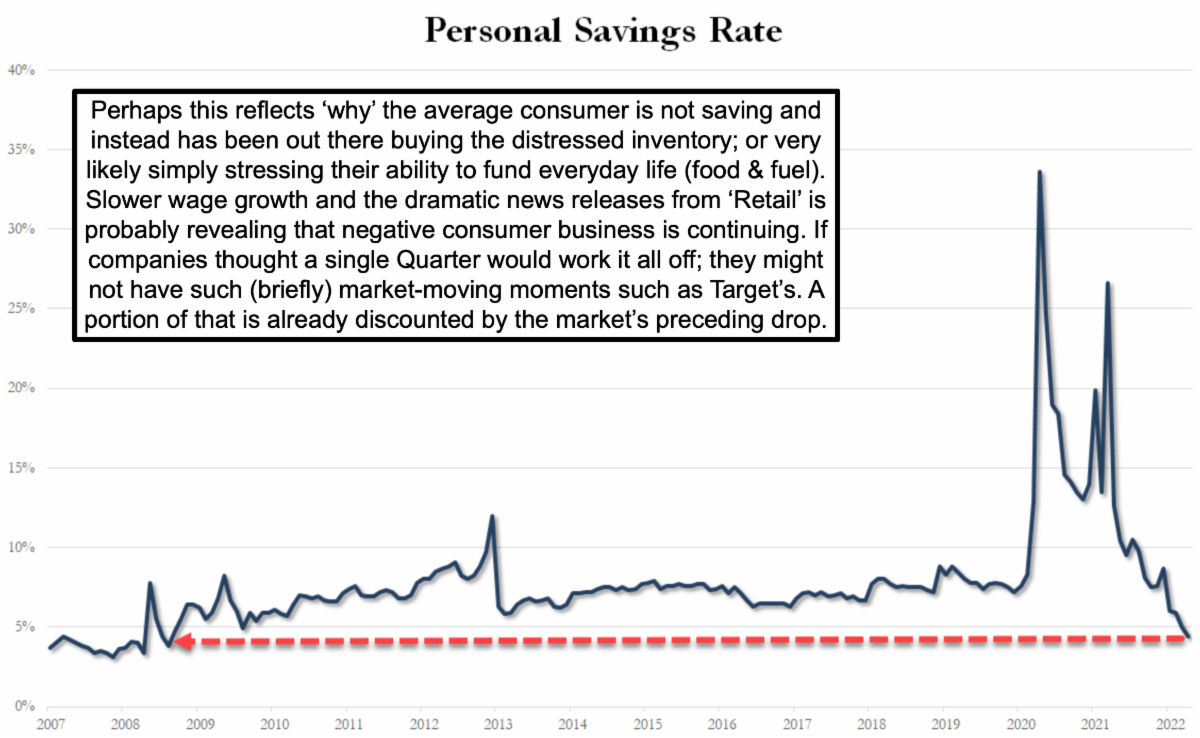

If anything, the 'profit margin squeeze' (which I talked about again yesterday), this time impacted Target (TGT), where they focused on switching to consumables or food, rather than durables (like TV's or Sporting Goods), given higher gains in inventories that we've mentioned (much restocking more than needed in all the depleted areas, and less so where needed). Perhaps investors tend to be surprised that Target management hadn't planned this better, I don't hold any view of that retailer particularly, but as it does cater to lower economic groups generally, it probably does reflect consumers impacted by inflation having the obvious need to focus spending on essentials and not so much discretionary or other items. That tends to suggest not just inflation, but diminished savings.

Lastly in this neutral session with a positive bias, we see Oil quite firm, and so that alone will tend to perpetuate the inflation aspects, as the CPI will show. If CPI is to be fairly assessed, analysts will be looking to see (as I suspect) very slight easing in certain commodity costs, and consumer durables, while foods and fuels will likely still firm. Anything shy of an 8.5% annualized rate will likely be welcome 'as if' that implies 'peak inflation'.

In reality inflation is higher but it is not in the way Government will likely report it. Housing (for renters) is crazy high, so it's hard to understand why anyone is renting rather than owning, unless they simply could not structure it last year or even early this year. Government will of course minimize 'food & fuel', both being the core to inflation this year, hence 'X food and energy' means little.

In-sum:

We're likely to have a higher rate environment persisting, which really is more 'normal' in the modern era, whereas the period of extended low rates, especially during the pandemic, was the anomaly.

That's a big point: the market (after the dust settles on COVID and Russia) will be into a period of post-war / post-COVID recovery and growth (including huge rebuilding projects in Ukraine and armaments in Europe like it or not) lasting a few years. That is generally being overlooked by today's negative crowd. With huge debt structures, which we bemoan too, they're not as bad a percentage of GDP as might be the case, hence the politicians can get away with it more than they should (to be sure), but that's why the Fed knows there is a need to lighten the balance sheet and so on. Yes it's a goal to get a neutral level. This is not exactly the horrid 'growth scare' many talk about, 'if' the Fed can thread the needle. As I suggested weeks ago: maybe not a soft landing, nor hard in a conventional way, but as soft term it, perhaps a 'soft-ish' landing is in store.

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more