Market Briefing For Wednesday, Jun. 16

The 'transitory' inflation camp predominates among analysts, while some of us that have seen versions of this movie before, know it's not quite so easy to divine. Even as housing and food start to come down (perhaps this Fall), we'll not likely drop anywhere near preceding pandemic era price levels.

Therefore 'sharper bumps' such as commodities have experienced won't stick entirely, but they'll also not decline dramatically. Remember the drought which is a problem, keep in mind wage levels from business to farming, have risen a lot, and a notion that accommodation is still needed dominates politicians (no allowance being made for the insanity of overstimulating and raising debt).

But for now, the Summit in Washington of the FOMC, exceeds that in Geneva between President's Biden & Putin. There's not much of a sense of successes at either, just a hope among those who think low rates forever is somehow the prescription for success. It's hard to believe they favor debasing the currency, but that's the outcome.. along with perils of excess speculation near highs.

Near-term the downside risk exists, but it depends on whether the Fed tries to outline a 'timing cycle' for tapering. Their language must not veer very much if they wish to give a 'stand pat' impression, when overtly grilled by aggressive reporters, in the news conference.

If the Fed 'does' diverge from a playbook (ECB's Christine Lagarde last week hinted at 'not' addressing reducing bond purchases for the foreseeable future) that would be problematic, since it is presumed ECB & Fed consult closely.

If the 10-year continues lower, be very cautious that it not spook markets 'as if somehow it knows' that a new round of disinflation, rather than inflation, might be on-tap. How could that occur? A geopolitical shock or 'more likely' COVID's surge, which already is hinting at excess complacency among most people.

Meanwhile . . there are concerns involving China, which might be in the midst of shifting a focus on the Wuhan Lab origination of COVID (SARS-Cov-2) with their militaristic forays into sovereign nation airspace in the 'neighborhood' (as they see it 'their' neighborhood, but the entire South China Sea clearly is not. I greatly enjoyed Jon Stewart sort of hijacking Stephen Colbert's premier show back at the Ed Sullivan Theater last night, as I chatted a bit about earlier.

I'd never understood why COVID origins became a media partisan issue, since it's absolutely not. I guess it was because Trump said it could be, months after I'd mentioned the prospect (in January and again in February of 2020), or since there's a crowd that wants to appease China no matter what. That is how you historically get into trouble with countries, tactful diplomacy but don't embrace their viewpoint, especially when the prospects are this came from the Lab. So yes, a slightly flat week ahead of the Fed became enlivened by Jon Stewart, a political comedian/satirist the likes of which sadly barely exist (if at all) today.

Will the Fed start reducing asset purchases immediately? They may have in a very slight way as I recall, and whether you believe the economy is running at a red-hot pace or not, there's probably a propensity at the Fed to 'mark time'.

Our hint for that was of course the ECB last week, but we should nevertheless hear a bit about 'tapering', whether overly by the Fed statement, or likely via a series of questions to the Chairman that will 'pound' on tapering, until he does something like Christine Lagarde did, tell people to stop asking the very same question in several different ways, and just let policymakers deliberate.

Christine refused to put a timeline on 'when' the ECB will stop stimulus at this torrid pace, but Europe may need to persist more so than the US needs too at this point. It's somewhat academic, as I see the S&P able to shuffle or even to correct, as the Summer evolves, and that may be regardless of Fed posture.

The Fed just needs to be affirmative about policy, that we're likely past what's called 'peak acceleration' of the economy coming-out of the pandemic, but of course that presumes we don't go into a new challenge/surge from COVID.

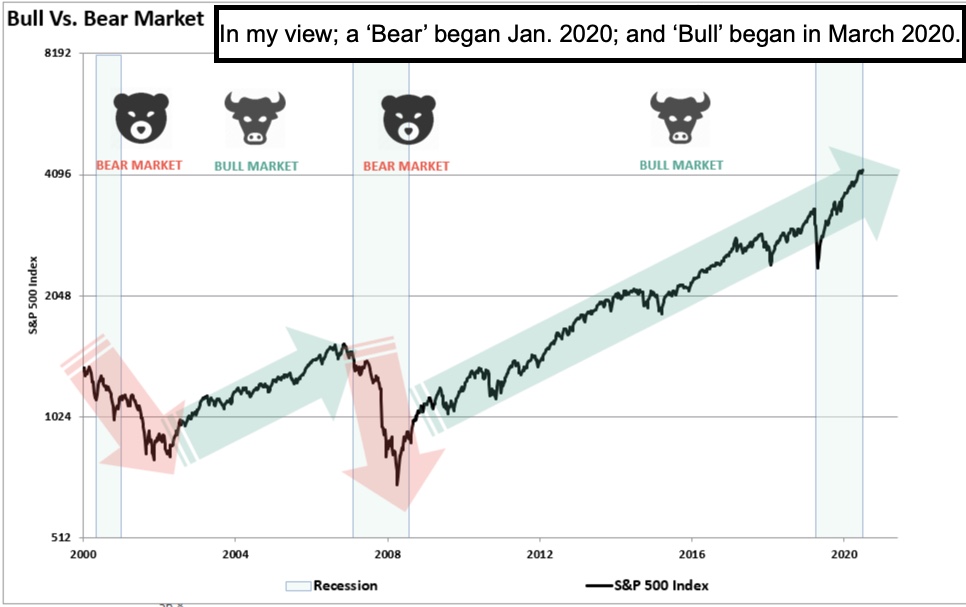

Technically, regression to S&P's mean is still a possibility this Summer, but that's not to say we couldn't get an S&P thrust if we survive FOMC decently, of course more or less along the lines of how Lagarde handled ECB's meet.

We do see China pulling back stimulus a bit, but the financial systems aren't tied to ours or Europe's, though Oil demand is going to remain firm here and in Europe, regardless. Copper probably corrects then moves up, Gold and of course Silver don't have great physical demand during COVID (traditional and other markets were gone), but the hedgers gambled (and many lost) chasing Bitcoin or other ways of playing crypto, 'as if' it was a safe hiding place (not).

If interest rates do start rising, Oil will likely be limited in further advances, but of course the supply-demand equation (and production levels) means more. It is not that I want Oil to drop (I do not), just realistic based on regular norms. If this is a 'bubble of demand increase', it will impact commodities more than Oil (OIL, BNO).

This is a period of uncertainty, of mild rotation, and of monetary jitters. While it is not a popular view, the overall debt structure and snappy recovery by most of the US economy, supports the idea of reducing (tapering) the stimulus and also pointing money at infrastructure, but not other stimulus efforts (broadly).

This is an excerpt from Gene Inger's Daily Briefing, which is distributed nightly and typically includes one or two videos as well as charts and analysis. You can subscribe more