Market Briefing For Tuesday, Sept. 8

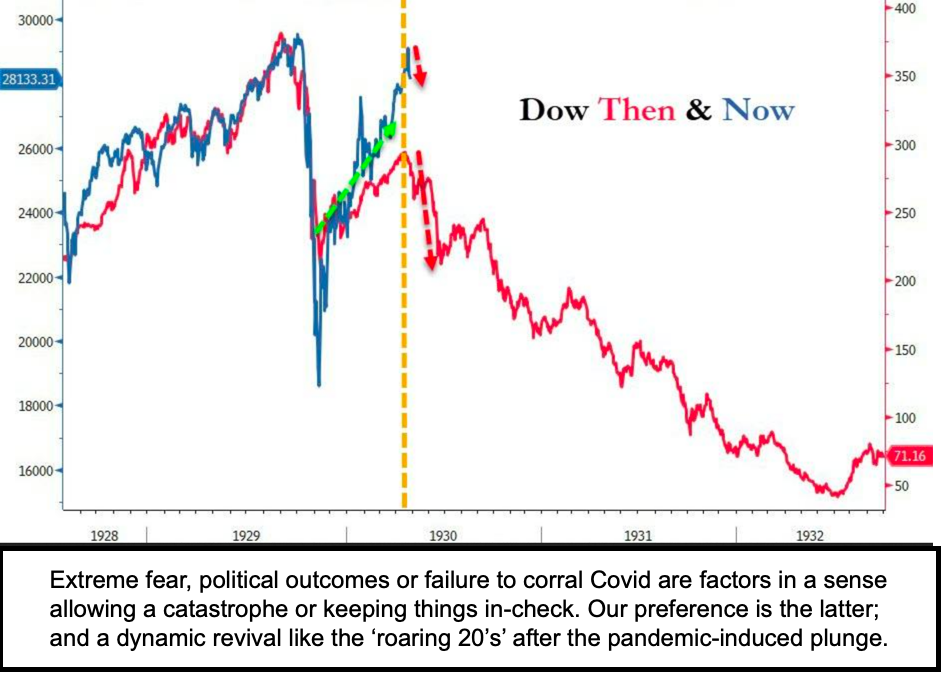

S&P 'overshoots' - triggered great caution by us going into September, which was affirmed early last, week when the Index moved over the 'standard deviation bands' upper levels, which was just a variation of warning of unsustainable upside. Simply put: the S&P briefly exceeded 'even' the 'worry wall', hence an upside capitulation, a buying-climax in much the same fashion as inverse of a selling-climax, but with one important catch, it was a narrowly-led leadership, which had spent a couple months taking total control (Generals ahead of the troops), and we thought time to 'retreat'.

That was primarily for the 'super-caps' that dominated the upside, because gains of course were concentrated in sectors that still thrived during the pandemic. Activity I'd discussed in August about the 'Robinhood' (or similar) trading groups impact, and the departure of a useful tool they had (Robintrack) showing how many clients owned a given stock from day-to-day) was part of a crescendo of late-stage speculation.

More recently you've heard about the huge open interest in out-of-the-money Calls, which might have been written (sold) by large hedge funds (Japan or elsewhere) not so much because they expect higher prices, but to generate income that lowers their cost-basis of holdings (and such strategies... whether considered manipulation or not ... are not unique and will vary among firms), most hedgers see similar algorithms.

That also means that as this market recovers, perhaps even helped in a short-trading week coming-up after Labor Day (4-day compressed trading week), many inferences so many drew about new apocalyptic cycles unfolding, might be correct 'structurally', as far as some strategies that have been employed. But it doesn't mean they expand immediately, or for that matter whether that approach was profitable, as the stresses of 'overshoot' (from those or other reasons) has been building or weeks, or longer.

Executive summary:

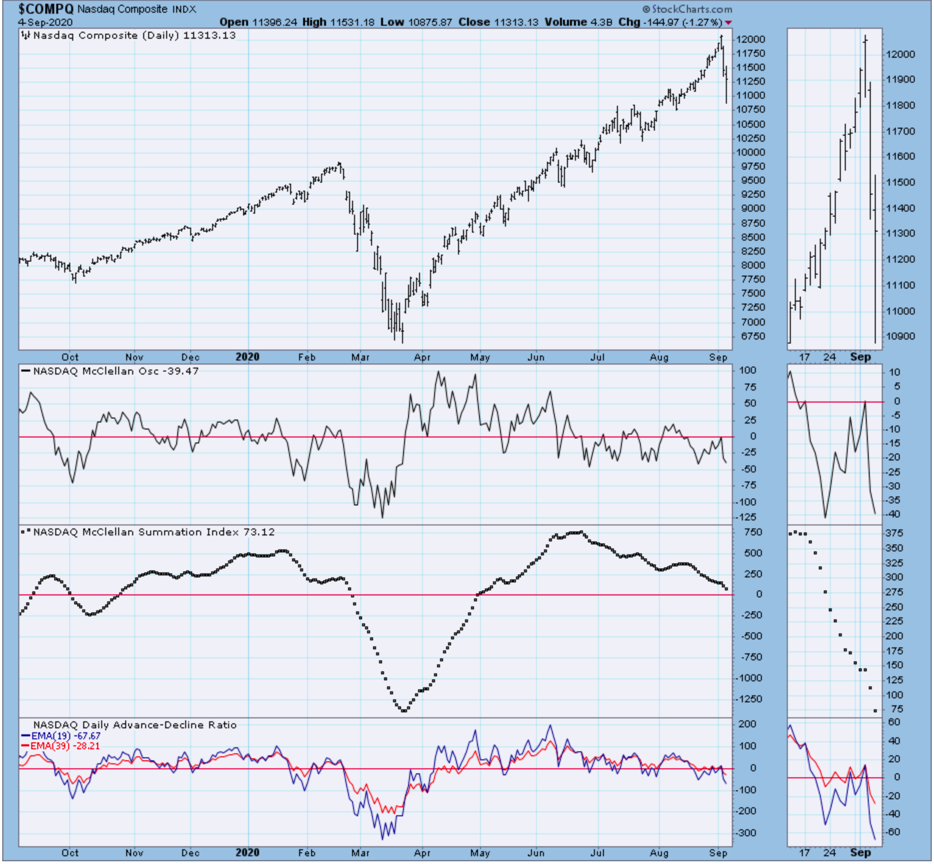

- S&P and most 'super-caps' (also Nasdaq) bounced initially on Jobs news (the bearish hourly pattern for the start, inviting selling into margin-calls an hour later).

- Then, as suspected, we got a solid turnaround which ebbed-and-flowed higher, actually briefly getting into plus territory for DJIA and probing that for the S&P.

- Aside 'pre-weekend' squaring you had an impact from the WHO warning that a viable vaccine won't be available this year impacted the market, is tough to say.

- After the Close, S&P made changes, and Tesla (TSLA) did 'not' make the inclusion cut, perhaps S&P is concern about too much volatility being introduced (hah).

- By the way it has been suggested that Tesla's newest $8000, fully-auto-pilot option, apparently doesn't work 'as advertised', though we can't be sure (in an autonomous driving car with it on, you likely 'want' to be sure).

- There is obvious friction between the U.S. (and interpolate CDC for now) and the WHO due to their homage (to a degree) to China, and now the funding dispute, so for sure no love is lost between the WHO Chief and President Trump.

- We're aware of growing discussion of the 'patenting' of coronavirus and funding of the Wuhan Lab years ago (we discussed that intensely before the US acted at all on this based on the Manitoba and Harvard arrests and deportations).

- Some of the speculation is correct (but not in the 'conspiracy' framework in which it is portrayed), but does support my suspicion since January that the virus was 'engineered' and unintentionally released, if anything working 'with' China would be logical pharmas (like Sorrento, SRNE) are indeed doing so with antibodies.

- I believe this matters, as many more people would be willing to be injected with a protective antibody already made, than have a vaccine which would have to try to coax the body to produce antibodies (in-theory the therapeutic has advantages).

- Whether or not another massive S&P sell-off is coming (Friday was not such a day), it gets interesting, especially as politicians on both sides see what seemed a bit like 'carnage' (remember our chart showing June), and perhaps act.

- Seeing that they will probably formulate another big or interim 'stimulus' Bill, said to help people 'bridge' a continued gap ahead of vaccines (but also lift stocks), I mention vaccines because that's the pressure, though it should be therapeutics or at least a T-Cell 'centric' vaccine which in-theory will have longer memory.

- The 'real' Unemployment Rate is considerably higher as many work below their abilities, although superficial numbers were encouraging, while of course lower-income mass jobs are among the most suffering economic sectors.

- A lot of issues come-together over the next few weeks, and while we did forecast a rough September and forewarned of a shakeout, don't dismiss the possibility of a more high-level range-bound market, with lots of pre-Election angst.

- With that said in some Election years, Octobers were dicier than September, the controversies and accusations are wild, and I'll leave all that mostly to media, it's a shame that the message from both sides isn't more of unity and compromise.

- As to groups, should a viable therapeutic 'suddenly' appear to be pending FDA approval, beleaguered biotechs in that 'space' could find another spate of action, and interesting this could occur 'even if' the big regular techs get defensive.

- Interest in biotech speculation other than breakthrough testing and treatments, may remain limited because of competition as well as realizing it's all a gamble that loses favor with players after 'effective' vaccines (probably several) become available, but focuses on 'treatment' biotechs if people largely reject vaccines.

- There will remain a need for therapeutics since no vaccine will be completely protective, and some are going to be very hard to distribute, which might be part of ineffectiveness in many parts of the world, again 'why' a focus on therapeutics or vaccines that combine Covid-19 along with T-Cell stimulation start appearing.

- Climate-change reminders coming to the fore along with pandemic, as historic temperature swings are coming in the Western half of the US, power outages or brownouts due to increased fire risk in the days ahead, political influence?

In-sum: it's not definitive, but while anticipating a September correction, that's not to say you won't get more significant rebounds (not simply buy-the-dip or option related) and that's seeing something we've talked about... money shifting from really the huge super-caps, and moving into a broader variety of generally mundane securities.

But it is those mundane stocks that often will benefit from 'real' economic recovery. It is a recovery that will be minimal for awhile (better superficial jobs interpretations or not), or hopefully not dragged-out so long as the Fed Chairman suggests (says look for recovery to take years, and I guess that depends on what sectors are watched).

Bottom-line: 'headline risk' continuously prevails in this market for sure, especially in an unprecedented Election Year, and not merely because of the awful divisiveness. I do think a politically-agreed-to stimulus package will be forthcoming, even though at least some believe data is improving enough that we don't need assistance (I for one think you foment the quasi-insurrection if you don't fund more of this for now).