Market Briefing For Tuesday, June 18

We suggest not being lulled into excess complacency by the flat-lining of the S&P (and basically other Indexes as well) over the past couple of weeks even though that is the general pattern rightly anticipated for the market.

As we get into the FOMC Meeting Tuesday (with a decision on Wednesday) there is no change in our view of a Fed jittery about economic sluggishness that we've forewarned coming for over a year now. That gives them 'cover' if they so choose to at least express a dovish perspective; or taking the.. 'let's see more data and how trade goes' .. approach to doing nothing, while they might hint at movement 'in July' if things continue deteriorating.

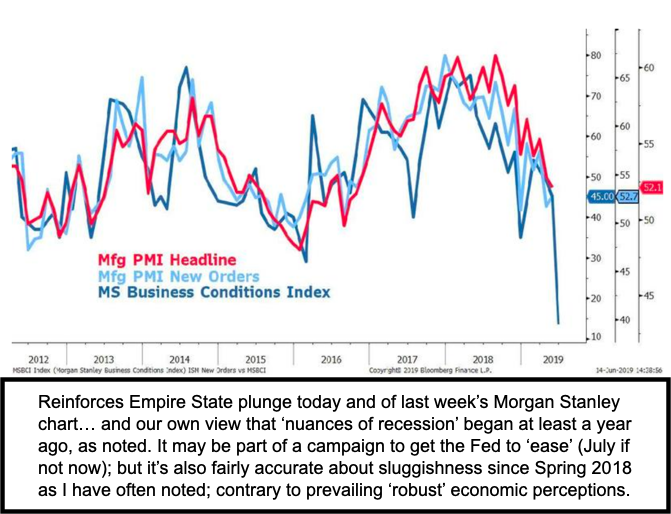

Having discussed all this over the past couple weeks as an 'on-hold' pattern for the S&P especially (plus or minus the 2900 area; and not much above), I won't belabor the same particulars tonight; but simply remind everyone of a belief that the fear of 'recession' is misplaced; since we're already in one.

As it can't be 'formally' identified until after certain levels reverse, we looked at a series of 'nuances' which began well over a year ago. Now look at chart reflections (whether the Morgan Stanley one the other day; or Citi's or even just the Empire State or business optimism), and you'll see that deterioration began in 2018 as I've contended, and not something on the threshold that a quick rate cut by the Fed would somehow obviate.

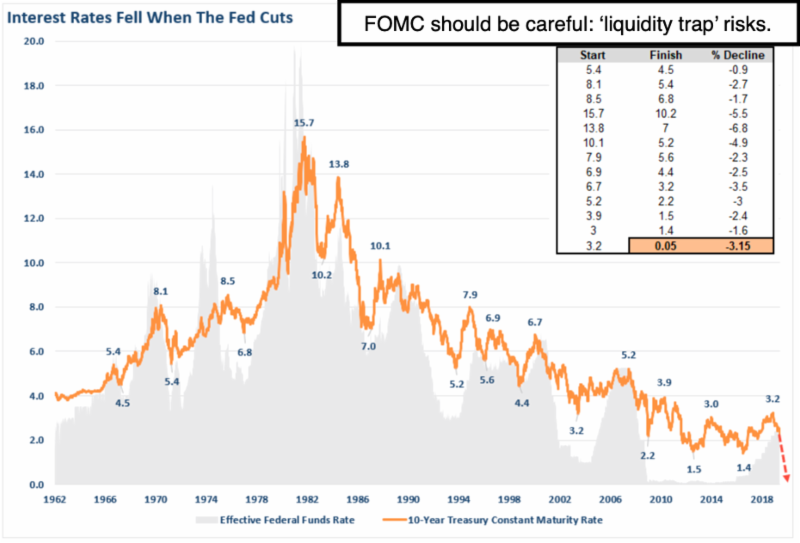

A rate cut might briefly (and not sustainably) help the market, but mostly the move would buy time for the bond market and keep debt service low (that's the main reason Government wants low rates). Actually they'd rather have a period of inflation, so they can repay dept with 'devalued greenbacks', as I'd term their desire on-occasion. It's always amusing to see reporters ponder 'why' the Fed wants a little inflation; but that's what it comes down too in an era with embedded high-debt psychology, which itself is a macro issue.

In sum: we've already shared alternative knee-jerk reactions possible to the Fed's decision and/or what happens with G20 in Japan. On the latter we are not among those who say 'we must get a trade deal at Osaka'; because that is not what G20 is about. I suspect the most you'll get (if even) would be an agreement to resume talks towards agreement; with very little specificity.

Meanwhile, the market (so far) is ignoring Iran's serious 'nuclear blackmail' threat. Tehran needs to be careful because 'now' they're playing their cards against the EU, just as they are against the United States. By threatening to exceed the 'ceiling on enriched uranium' ten days from now; the U.S. moans about their behavior; but they still have the 'active' deal with Europe. That's at-risk; so their macho behavior on the issue with the EU is a non-starter.