Market Briefing For Thursday, April 7

Inflicting damage on stocks, is presumed to be the Fed's objective with the tighter monetary policies. Actually the target is inflation, and perhaps housing more particularly than equity markets. However, the Fed is keenly aware that Americans have more of their 'net worth' in equities (directly or indirectly) than ever before, creating a situation that is untenable from several perspectives.

Now we're going to hear about not being all in equities, which makes sense of course, but isn't something heard except when markets hit potholes. As for real estate, this has been obvious for many months, and it's almost a "cliff" in some cities with regard to listings that go without bids, and mortgage declines. The media is touching this lightly, but the reality is we go from shortage to the fabled excess, especially in pricey new houses and luxury condos, quickly.

Parts of the stock market have come down to levels of relative attractiveness with valuation levels being increasingly compressed, or remaining speculative for the sprinkling of innovative and/or disruptive contenders already smashed. However that doesn't mean (like you saw Wednesday) that already downtrodden are somehow immune to erosion especially if they're included in ETF's or Indexes (even if they subsequently get some air and take a breath on the upside).

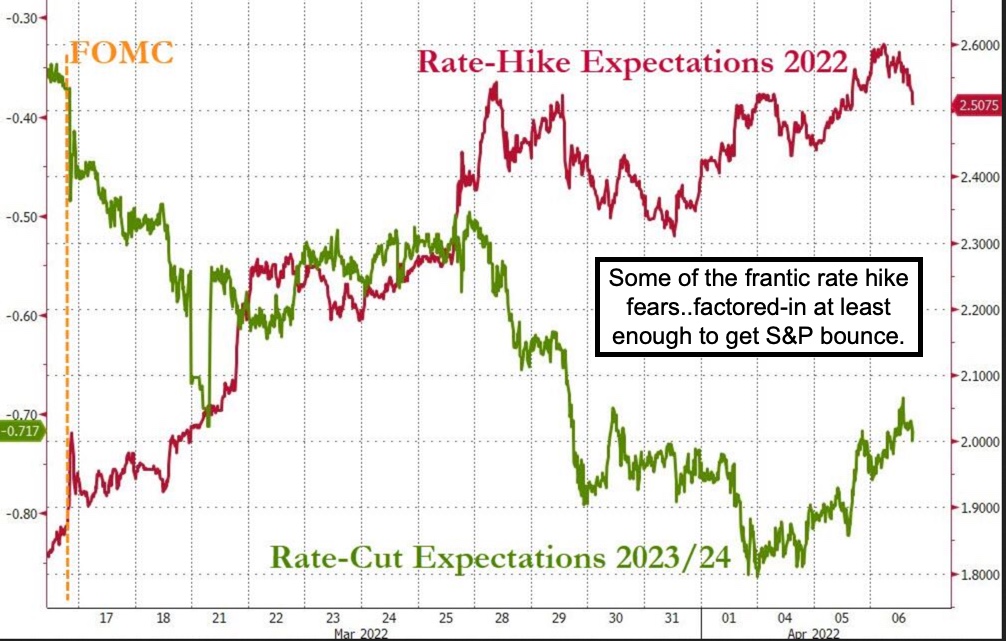

The Fed Minutes last time showed a fairly robust Balance Sheet discussion, a topic that was avoided in Chairman Powell's Q&E later. The Fed isn't going to hit the 'cap' of their runoff plans immediately. But, if they adhere to aggressive unwinding, this will also impact markets in a shorter period of time. Part of that is already discounted by many stocks, however not so much by S&P or NDX.

In-sum:

The market's not exactly prepared for a bigger and faster Fed move. We've already seen some deleveraging, with negative momentum prevailing.

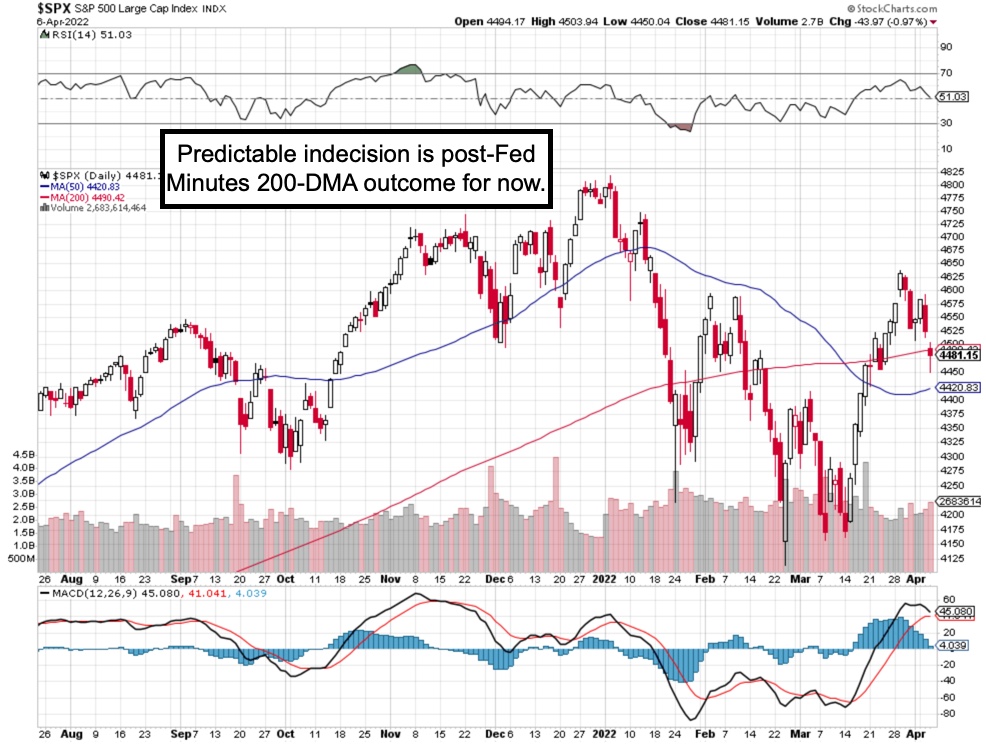

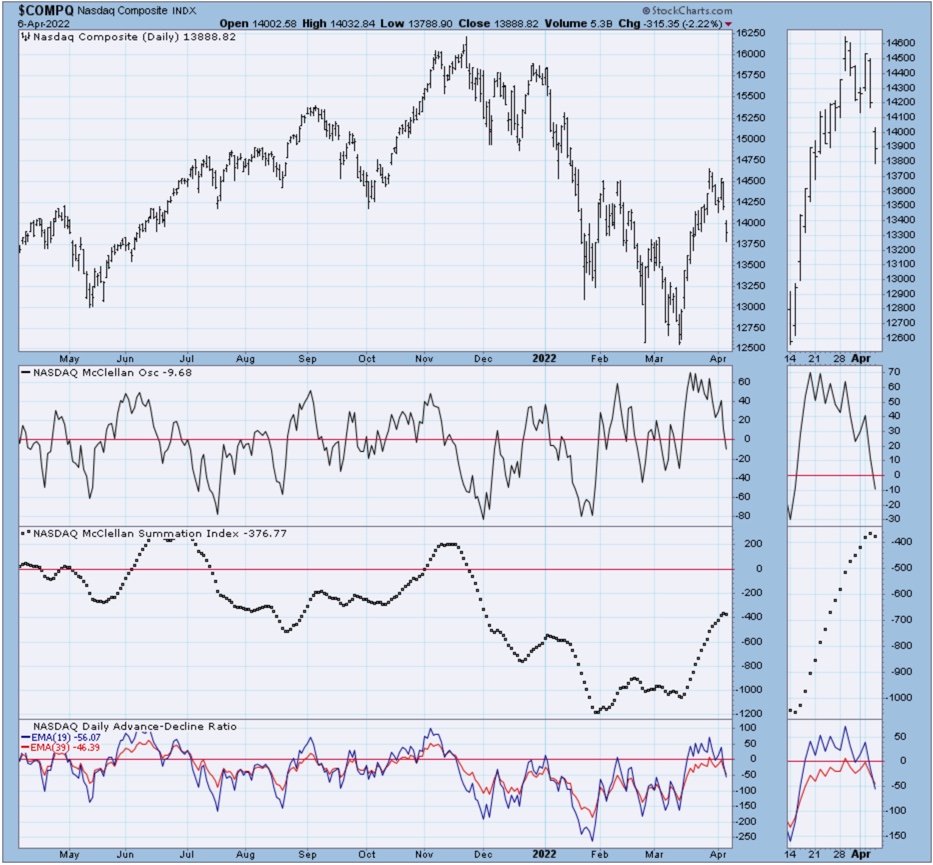

If one wants to simplify the S&P chaos and current technical posture after this wild day, it's this: many speculative stocks were barely red after deep declines earlier. And the S&P, which broke the 200-Day Moving Average, rebounded to finish just shy of the 200 DMA, which means 4490 or so. Hence: indecision.

Classic 'late cycle' behavior is what the market has been expressing in core big-cap stocks, and as the FOMC Minutes recognized that, it means the Fed's not really as aggressive as was feared based on Brainard's 'hawkish pep talk'.

The Fed's bark was thus a bit greater than its bite, and oscillations are just the fallout of trying to interpret the Fed's goals, that actually were on-expectation, at least at the last meeting. So you got a rally followed by selling and 'chop'. I think we can horse around and get a bit of a rebound here, but then variable.

It's hard to say whether 50 bp hikes are on the table, and if so how many. So I would opine that the Fed's decisions have yet to be taken (in May). They are, however, inline with what the Fed governors have been discussing, and stocks to a degree have mostly priced-in what's coming.

The Fed-heads delivered as part of the approach to nursing all this, through of course a narrow corridor, and it is not conducive to a 'soft landing' either. Why that is so is reflected merely by looking at Housing for now, while a Transport decline reflected more factors, some of which (lower shipping costs) are really a plus for softening the pace of inflation. (I noted DJT warning last week.)

Concurrently the war restrained the Fed from moving higher even sooner or in greater magnitude, while the COVID situation in China wasn't addressed, but in my opinion really does contribute to supply-chain and pricing issues for now and will diminish as China gets a handle on things, and/or eases lock-downs.

The Fed is reducing investing in longer-term securities, slows the economy as well, and brings down inflation, to the extent they have myopic domestic effect which they do, but they aren't giving ample consideration to existential factors.

Bottom-line:

The Fed is 'mapping' what it wants to do, but isn't actually doing it yet, and that matters. The traders today initially faded the Fed, then a fast lift and then soberly reassessed, realizing that regardless rates are going higher.

Peaks in big-cap profit margins remain a factor, Quarterly estimate revisions I suspect will be seen as we get corporate guidance in weeks just ahead. Even Oil is down, partially on the idea of lower demand, but that's also disinflation.

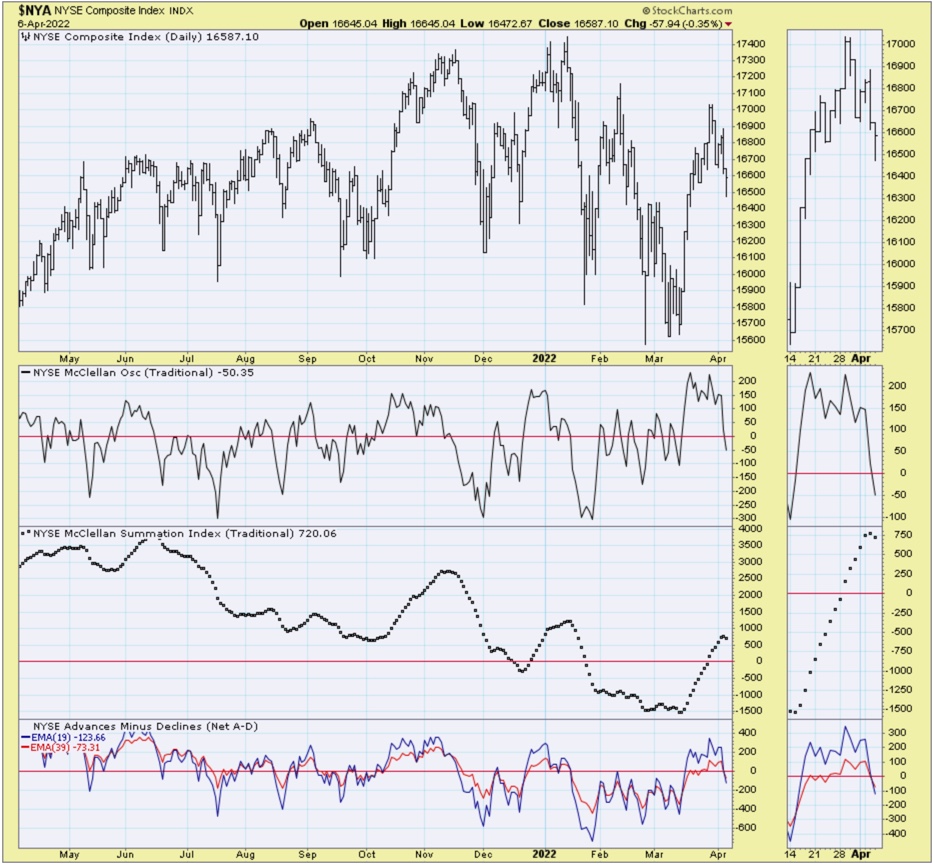

Lots of what went on today, is algorithmic, while hedger risks are being taken with a bearish bias. They may have overextended their downside presumption at least for the moment, which was reflected in an irregular snapback after the Fed Minutes were released, as was essentially something speculated likely. It was better in the S&P than in Nasdaq or SOX in the very late going.

Bill Dudley (former NY Fed President) said essentially 'if stocks don't fall on their own, the Fed will make that happen'. Perhaps is my response to that. Of course we don't ignore what the Fed is saying, or what Dudley implies. Really this comes down to too-much money thrust into the system, same for stimulus in-excess, failure of Government to calibrate the impact beyond immediacy of so-called 'help' to society during a pandemic, and now higher wages and Oil for sure influencing prices, plus a war, which domestic Fed moves won't resolve.

A lot of damage (outside of a handful of mega-caps) has already taken place, the Fed does need to snug-up, but the market may weather this storm better in the fullness of time than people think, unless the Fed really wishes to harm the economy and replicate the 1970's, which I doubt is their intention. Besides we do have a majority of non-Index stocks scraping at all-time lows not highs.

This Fed is over-impressed by their ability to tame inflation, given the added factors of war and China's COVID which also impacts supply-chains with no particular way for Fed interventions to interdict. Debating the preceding or forthcoming S&P lows isn't the point of course, nor is the idea that being optimistic is 'fighting the Fed'.

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more