Market Briefing For Thanksgiving 2021

"Cancel culture" fortunately spared yours truly this year, hence much to be thankful for. Trying not to be too melodramatic, but wow.. what a Thanksgiving with unfortunately no family locally, but lots of good wishes being shared. And as you're reading this, I presume you guys and gals also made it through what has been an incredible pandemic. I thought 2020 was bad enough, but that of course was merely an inconvenience compared to what this year brought.

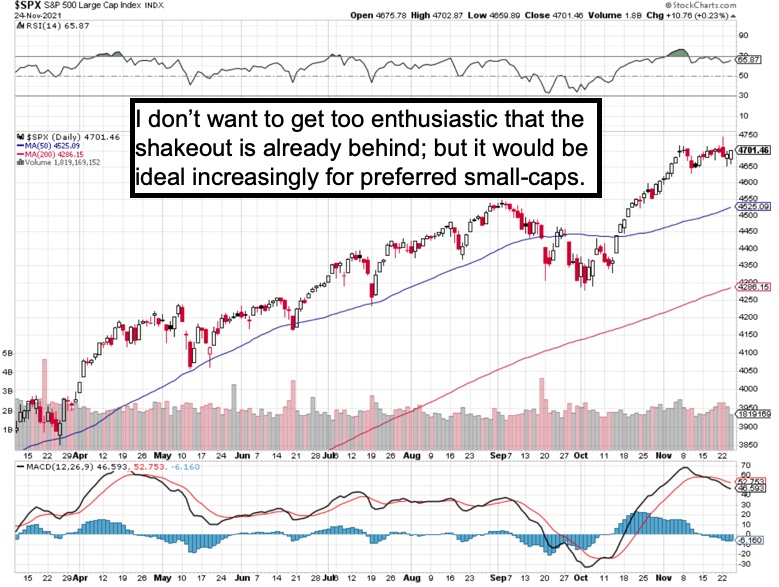

For investments, even though this isn't New Years (just feels like I want 2021 to end quickly) I look back and see how little the Indexes changed amid so much shifting and struggles, including almost no movement while I was hospitalized and then it got a little interesting, but just a 'grind' higher to posture the S&P.

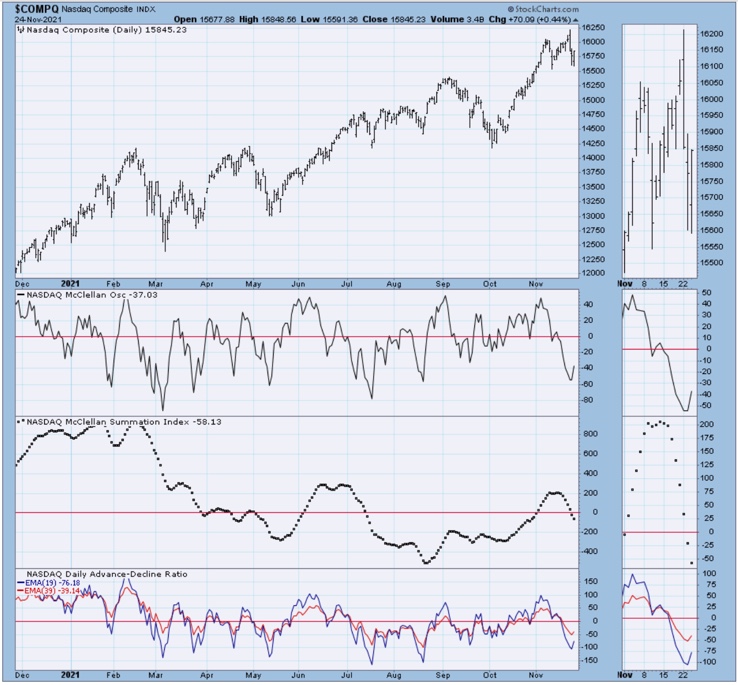

The high valuation names have been alternatively crunched and recovered, a bit including this day before Thanksgiving, which just happens to be seasonal as well. This year is different because of probably tax changes next year, that I won't review as we all know the impact on losses and gains 2022 may bring.

There are some with an extreme point of view, which has SPY Puts with enormous premiums that would require a thousand handle hit to simply breakeven. That's nuts. Not even a couple Fed rate hikes would do that much damage. World War 3 might, so unless the Put buyer resides in China, I'd like to know about it. Such a person must know more than all of us.

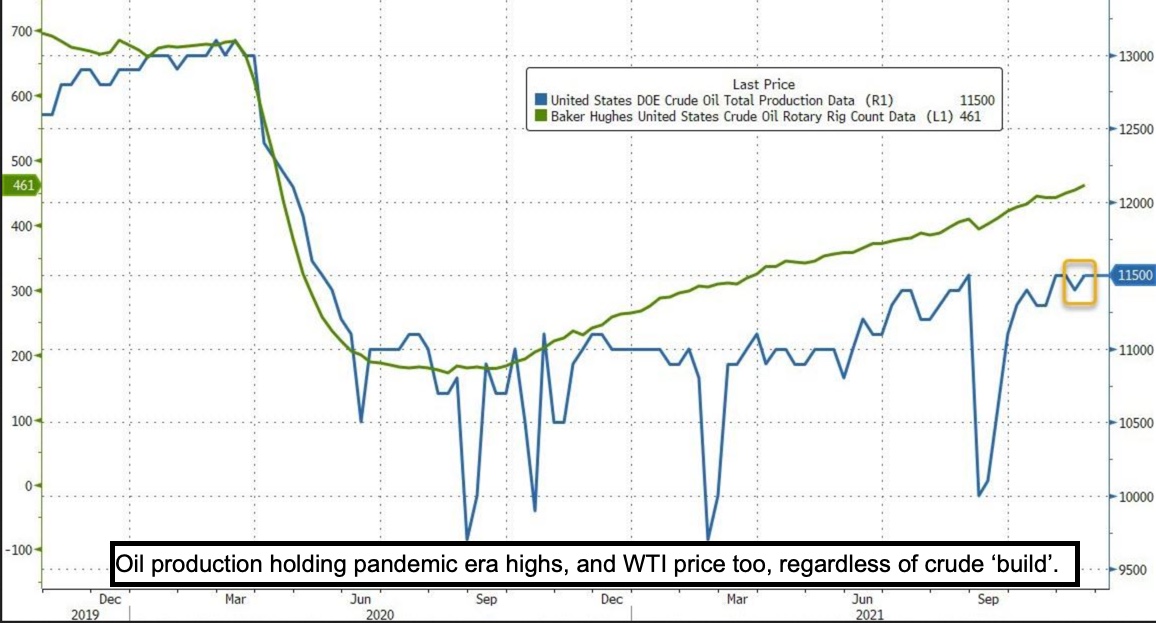

The shifts in focus have included one of our key calls of last year, which was a requirement that Oils and Banks (especially Oil) rally in 2021 for the market to hold together and let the mega-cap leaders grind-out those higher levels. Oils are expected to generally stay firm in 2022 also, essentially regardless of Washington's twisted Oil policy, where they hammered against fossil fuel then beg OPEC for a production increase and blame the oil companies after they beat up on them (OIL).

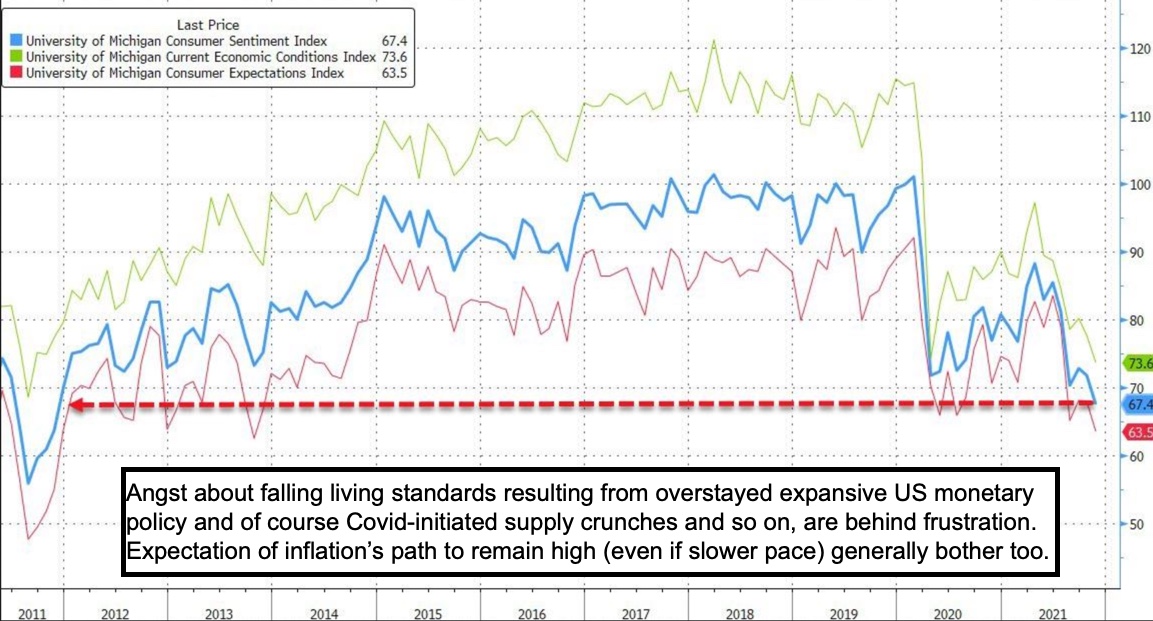

The majority of 'free money' (which isn't free) is done, and savings eventually get burned-off by consumers, so they are indeed grumpy but also spending. It is a funny crosswind (of worry but spending), and that figures like a consistent bifurcated nature of the crosscurrents in the stock market, for months really.

The interesting risk next year would be for some price 'reversion' that results in a sizeable 'deflation', but even that would 'at best' be hard-pressed to get an inflation pace down to the target 2% rate. Many price increased are baked into the future, and enduring as I've often discussed.. especially wages and if I may say, relatively high, but not astronomical, oil prices.

Let's hope most of the tax selling is out of the way but time will tell, especially if one differentiates taking 'gains' this tax year, versus losses and the 31 days to wait to replace, which may be a factor contributing to most already done (if an investor wants to be in that same issue in 2022). I'd still expect some chop and 2-way action in the market for the coming week, as it remains fairly dicey.

Meanwhile we have 'real' disposable personal income below the inflation rate, and things definitely don't feel as great as the politicians want us to believe. It is big transfers of taxpayer money (is that redistribution?) inviting higher taxes that probably contributed more to this, along with mandatory wage increases, that accounts for the projected inflation, more so than just Oil prices.

Politically DC certainly would like to blame anything 'other than' politicians or the uber-easy Fed', which has a reappointment of the Republican Chairman Powell, possibly only because he went-along (or saw the need) to bailout the country in early COVID (but as I've suggested that was needed then, and was a huge factor in my March 23, proclamation of an S&P low last week), and it seems he continued to 'play ball' longer than that strategy was constructive.

We now feel the inflationary impact of overstaying the policies and if things do fall apart (which in this environment they will clearly try to avert) this Fed has a relatively little (if any) room to come to the rescue. I suppose that's the 'bear' view of next year and the reason for outrageous premiums on Puts. So far all the Index Put buyers with any duration beyond nailing a shakeout to the week have lost everything, just as was generally the case for those who fought big mega-caps over the past year. For those still-solvent bears, it might work one day, but not this day.

Enjoy the holiday!

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more