Market Briefing For Monday, May 18

|

Tension on the tape - persisted through the entire trading week, despite a series of fairly wild shuffles, while 'home in the range' prevailed, thanks to a critical (to deflect 'algo' traders disrupting the pattern) 'Hail Mary' rebound off-of the lower limits of the S&P 'standard deviation' bands we'd outlined.

Executive summary:

Sabre-rattling between the U.S. and China has echoes of 'protectionism'; a sentiment that old-timers (or students of history) will associate with moves, of an anti-growth nature, that existed during the 'Great Depression'. As I'd noted Friday morning, this is not as likely an outcome as the superficial and largely political rhetoric (from both the U.S. and China) might imply. Yes it's hard to make a 'call' on how that goes in the final analysis; because it's pretty obvious that China has culpability; and it's not 'just' Trump trying to gain domestic 'cover' by jumping on China. They actually deserve some of it, but again I suspect this is playing to bases (his and the Communists). What's really going on 'probably' is more cooperation with China; which is exactly why Trump didn't even 'qualify' or hesitate, when asked during the introduction of the 'Warp Speed' vaccine leadership (I mentioned a couple days ago that he would appoint a major pharma vaccine executive, as he indeed did, formerly head of that division for GSK). The President clearly responded to a question of "would you accept and work with a vaccine if it were developed first by China and not us" and he answer was: 'Yes. Sure.'

And that matters, because it suggests the global nature of the challenge; a general assumption all humans with any time of humanity should urge; and yes at the same time there eventually probably will be changes to dealings with China; and that was happening already. China's cover-ups and delays as regards what was 'then' WuFlu (before the Covid-19 moniker) are better dealt-with later, as I mentioned. In fact, good cooperation with President Xi, if or when the time comes, might help ameliorate differences. I not only agree with Trump on 'repatriating manufacturing' (essential items especially) to the United States, but argued for this for several decades not just years, as many of you know. So when Trump ran for Office, part of my enthusiasm for the market (if he won) was not only 'capital repatriation' and 'lower tax' rates; but seeking achievement (not easy after so many years of neglect), the dawn of an 'American Manufacturing Renaissance'. Where I depart, and repeatedly try to emphasize, is policies that would 'cut off our nose to spite our face' fairly radical policies, which are too extreme. That's why I simplify it by saying: the world is intertwined and must retain a modicum of globalism; but not excessive globalism, which is where we got.

Had we disengaged 20 years go from China, it could have been different of course; so in this era the moderate approach of realigning supply chains (a process already a couple years into the process well before Covid-19) very much is preferable to radically severing ties with China, which Trump had hinted at earlier this week, sort of 'as if' he was in a position of strength on it. He is in some aspects; but in others China could put huge pressures (of course the first that come to mind is the continued or more forceful military presence in the South China Sea; or at worst moves against Taiwan; which Xi's Generals often advocated; and which would threaten a hot war.

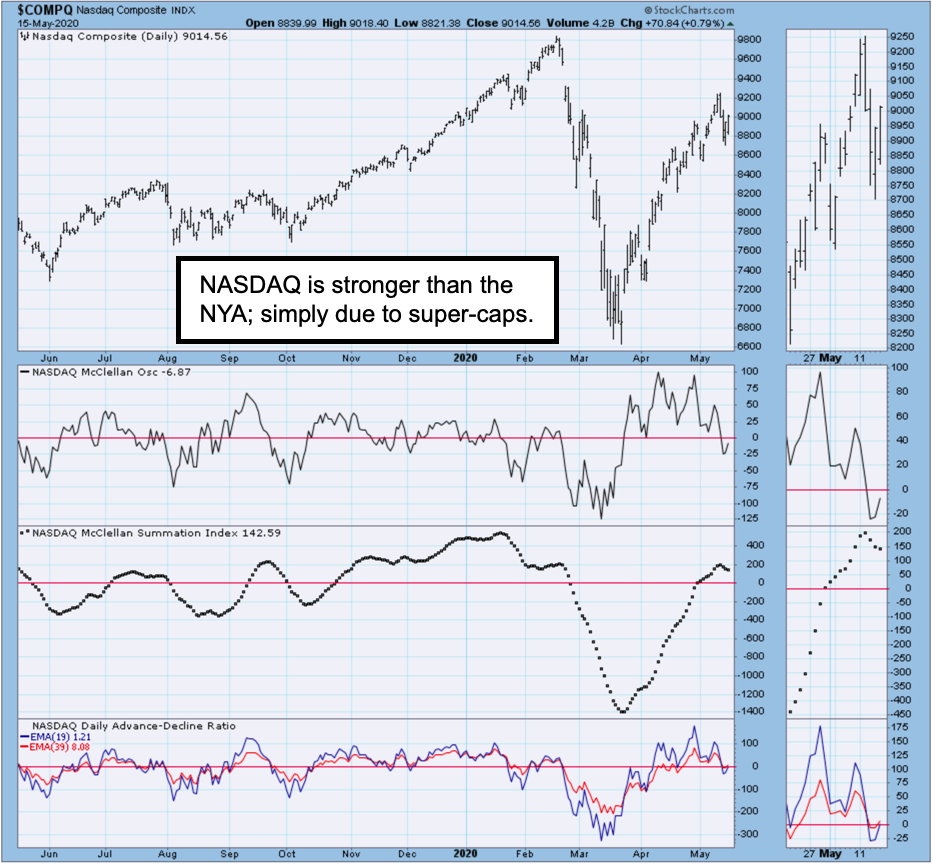

In sum: after all this the S&P remains bound in the range between the 50 DMA and 200-DAY Moving Averages, which was our target for the upmove from the (nailed) March capitulation low, that I affectionately labeled then as the 'Inger Bottom'. That was a V-turn; while the 'Inger Top' back in January and early February was more of an exhaustion distribution pattern as 'huge big-cap' stocks held up the S&P while mundane stocks did very little. As to Trump and China; I advocate taking one Xanax, not ten. (As I'm fond of saying: trimming tensions by finding a middle-ground with China reduces angst between both; and keep essential aspects intact.) That's less anxiety as one Xanax provides. Ten Xanax would be like severing limbs that bind; and the relationship might not wake-up at all.

Bottom-line: a little globalism will be maintained despite the rhetoric that's in the public realm. But it will be modified (that trend already is ongoing). It should be noted that Qualcomm gets royalties on every chipset going to China and someone will inform the President that the tit-for-tat has limits. Trump absolutely has merit with the Huawei restrictions; but perhaps calm in other areas is constructive if not essential; foremost being racing to find therapeutic drugs for Covid-19, even more so than the admirable pace of delivering a vaccine. As to the vaccine 'time-line', that's not so surprising. Moderna is advanced already, even though it's a different form of manufacture. The Israeli and a cooperative Texas vaccine are among those that already stated they are in a speedy effort hoping to have 'validity' around June (yes next month) and ideally rush into manufacture for inoculations to begin even late this year, not necessarily early next year, which is what the skeptics even question. I understand why (history of development); but the new approaches that do not have to be 'grown' in eggs for instance', also negate some opposition, that has possibly (whether they know it or not) been just allergic reactions. However, that does not say anything about future virus mutations; degrees of response, and so on (that aspect similar to seasonal flu vaccines, that in many cases only provide partial coverage given the various flu strains). Of course this is not flu; but most scientists are of the opinion that there is sufficient commonality (points on the virus that are shared by all mutations; addressed by vaccines regardless of the variations). That's why I was surprised to hear people say you'd need a number of different vaccines. I thought nope; many companies may join in to ramp-up production; and a number of vaccines may work; but they all have to provide similar protection.

Conclusion: increasing semiconductor production in the U.S. is a plus as well as enhancing our relationship with Taiwan (that's the part upsetting the Chinese I suppose; since they buy most chips from us; not domestic). Chip designs are the 'crown jewels' of the semiconductor industry; and for many decades I've argued not to share that with any countries other than those that simply have factories controlled by the American parent. Intel with the facilities in Israel and Germany is a good example. Apple with factories in China is different; as those are primarily 'assembly' of products; the chips in iPhones for instance, are not made in China (ARMS licensed to Apple and typically made by Taiwan Semiconductor). Basically the market behavior is tenuous; open to correction; but note there is a concerted effort to defer or at least delay anything busting wide open. |