Market Briefing For Monday, February 10

Pensive concerns limit enthusiasm - even as the political backdrop at least seems to have calmed a bit (with regard to Trump and a backlash against extreme leftist opposition prospects), while the virus remains very much a concern for the near-term. Hence that's why several institutions at this point are calling for 'recession'. I understand the logic but demur.

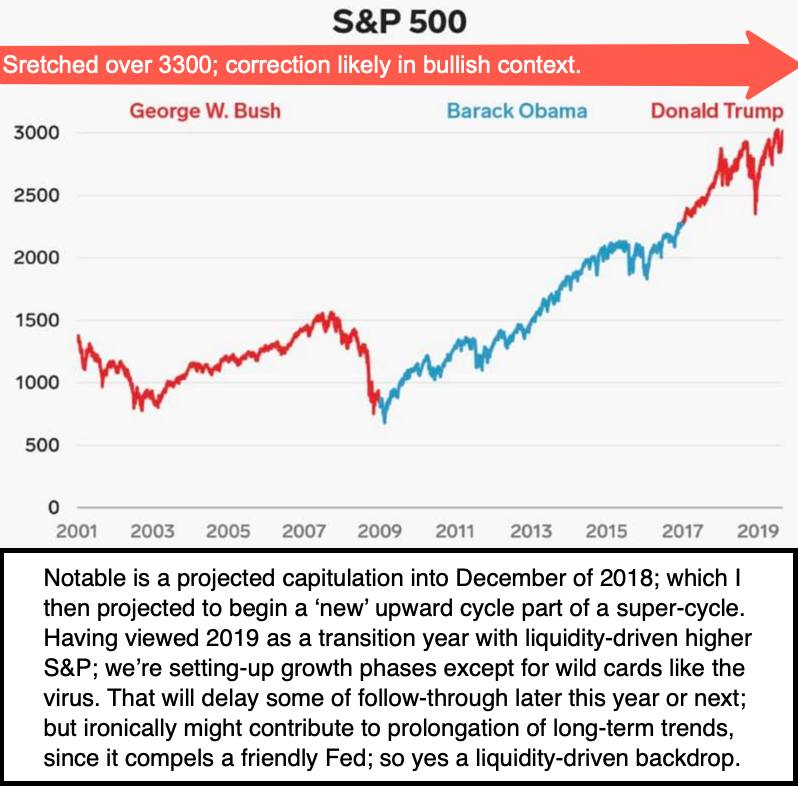

As readers here know, we've had an internal rotating recession in many industries for almost 2 years, following my proclaiming the end of a basic 'to the Moon if Trump won' 2016 call, ending in January of 2018. Then as we looked at the 'Maytag Market' (rinse & repeat oscillations with a mass of stocks in rotating corrections while the Street focused on a handful of leaders, commonly called FANG but really big-cap momentum stocks), it looked like (and was) a high-wealth exodus that we thought made sense in the Spring of 2018, but ended with a projected washout late that year.

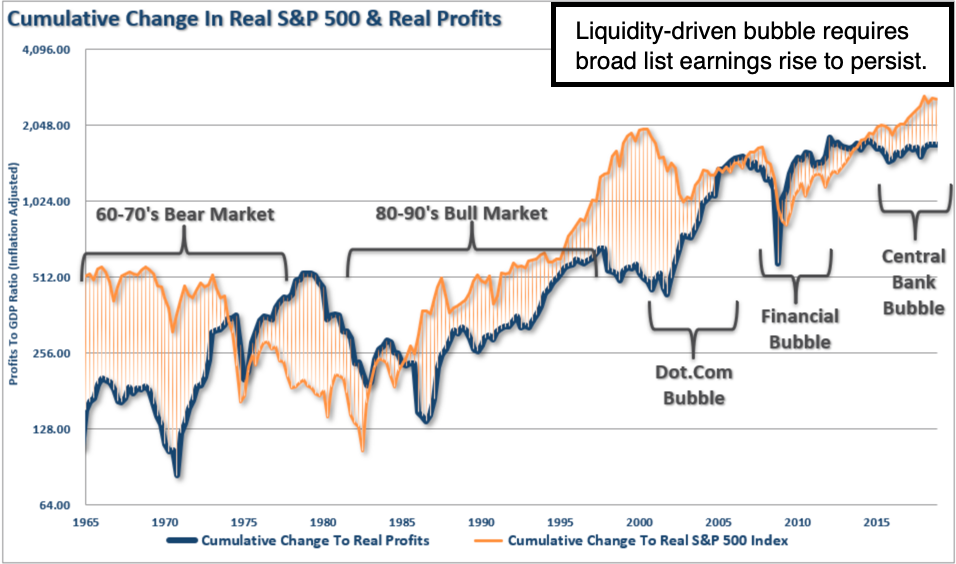

Notably, we believed a friendly Fed (not just buybacks or other sources), with the TINA approach (there is no alternative) would hold the S&P thru the 2019 transition year and lead us to continued or resumed upside. Of course, it's at a fairly ridiculous level for the S&P, but the expected start of recoveries from the broader list would help fill-in for heavy lifting that the handful of FANG-types can't be reasonably expected to dominate ahead, although some will depending on how their actual businesses do.

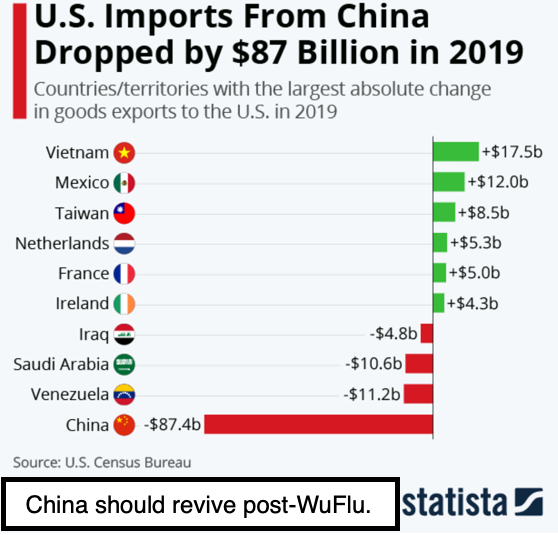

Hence the idea, with the USMCA and China trade deals done, set stages for a broader period of growth. However, it's delayed with the real variable of the Wuhan virus and whether or not that messes up growth beyond Q1 and Q2 (which seem a given). Near-term the question is: will China (and the world) see more virus or less when workers return to their jobs over the next couple weeks? That's probably a big question and challenge. At this point, I do NOT trust (but wish true) Chinese reports of peak virus. As they are telling citizens to stay home, reported data is likely incorrect.

Have we come too far or too fast? Well, the Bears said that for two years, and I consistently and rightly, called for corrections within the context of a long ongoing super-cycle, but with a view that we're in a separate phase that began with our 'get back in' admonition of 2018's Christmas Eve. So many opposed that and shorted the market that it helped our impetus to a higher level, and here we are.

Before the outbreak we started to see improvements to the global outlook and more; and essentially you can accelerate greater demand once we're through the epidemic concern, provided it doesn't become full pandemic proportions. I was so sad to hear of the passing of Dr. Li, the esteemed whistle-blower ophthalmologist we had just mentioned days ago, as very much a hero had the local authorities in Wuhan not suppressed him.

And I hope you appreciate the efforts of all those who quietly posted truth about the coronavirus (that I've dubbed WuFlu) in recent weeks. I rallied against the censorship that denied the genomic structure discussions that recognized doctors or universities posted to medical sites or social media because of the importance of allowing all kinds of ideas to treat it.

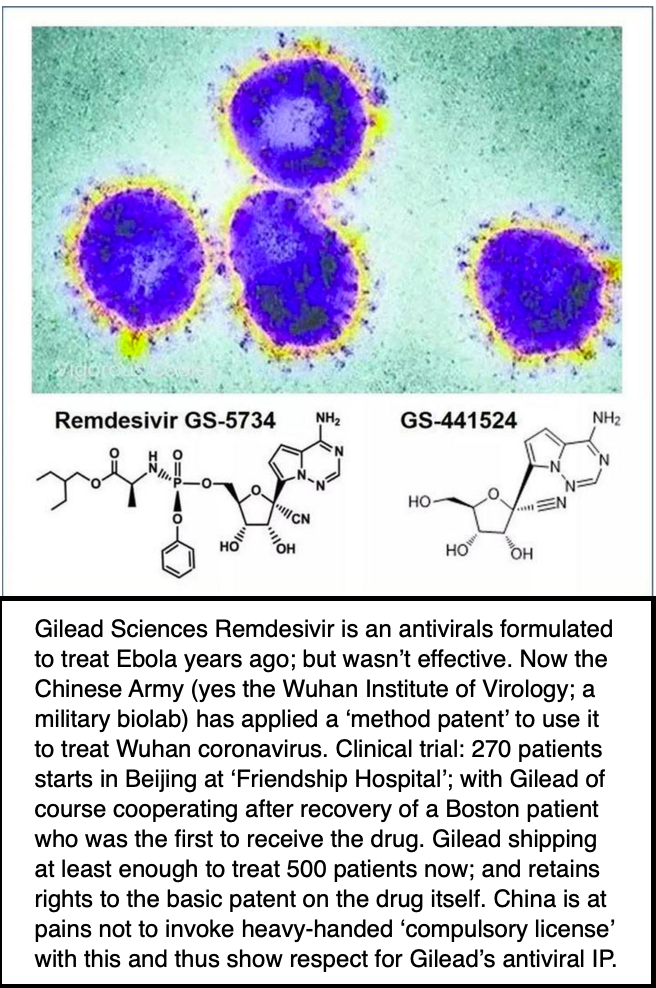

That's now past, and 'existing' antiviral drugs used to treat HIV (reported as a 2-strand component of this coronavirus, which was likely feared by the censors) are being tested on more patients in Asia. Even Dr. Fauci of our NIH danced-around this issue and it took a question to a doctor at John Hopkins on CSPAN to finally learned that research was pulled. Now a question is whether these drugs really work, and the old SARS vaccine too. Both factors matter as relate to how quickly one can envision growth returning to expected rates, especially on a global basis.

Minor notes: little LightPath Technologies (LPTH), long on the back-burner as far as stocks we watch, might see a bit more illumination. Their 2nd fiscal Quarter is out, and they beat numbers pretty solidly. That reflects not just expenses of consolidation behind but also emphasized solid orders and backlog. Ironically they are appealing the shutdown in China as some of the products they make there are essential to hospital equipment needed to treat patients. Presently a sub-1 speculation, LPTH has yet to select a new CEO and has plans (possibly the dreaded reverse split) if needed to comply with NASDAQ requirements that CEO Gaynor says they'll retain.

Our picks of the year for 2019 (made in late 2018) were AMD (AMD) (around 16-17 now 48) and AT&T (T) (around 28-30 and now 38); for speculators and investors respectively. Our 2020 pick remains Amarin (AMRN)(mid-teens). It's the maker of the novel Vascepa treatment for reduced cardiovascular risk, and now with a wider FDA approval achieved, and more aggressive marketing and/or partnerships pending, we consider it remains a decent value because it's been defensive in a choppy range for some time. We are actually surprised the shares are not at a higher level already, but as or if the litigation gets behind (Amarin was the plaintiff against generics in Reno, and the 'trial' is over with the Court's ruling expected in March), or if the Company is more forthcoming about its business plans or partners, we might see it move higher. It's a bit amazing that it's so narrow given as well the Canadian approval and pending EU approval as well.

In-sum: the S&P has absorbed everything thrown at it so far, so saying it ignores questionable and bad news is an understatement. However it's a truism that markets that do so are basically 'climbing worry walls', which it seems continues how I've assessed this market for months. With one key difference, and that's the variable from the epidemic more than politics.

So: we've had an internal rotating recession in many industries for almost 2 years, and now we should see a broader period of growth. However, it's delayed with the real variable of the Wuhan virus and whether or not that messes up growth beyond Q1 and Q2 (which seem a given at this point). Will we see more virus or less when workers return to their jobs in China over the next couple of weeks? That's probably a big question.

Bottom-line: I believed the 'stealth' recession or closeted-bear-market in everything but the S&P and NASDAQ 100, was 2018 and 2019, masked by buybacks and 'friendly Fed' liquidity injections holding S&P up.

At this point tailwinds are in-place for growth, aside unknown side effects of the WuFlu outbreak, which (if contained or effectively treated) retain a (fingers crossed) potential to be a huge relief for trade and GDP .. again 'if' contained. Definitely, it will result in a GDP contraction for China in Q1 and Q2 as well, so more or less delays some actual growth rather than denies it ultimately.

Footnote: chills go through my fingers as I tell you this with prayers: the very same State media that reported the Chinese Doctor who sounded a slew of early warnings about the Wuhan virus is now 'revising' that report, saying he's not dead, but in critical condition. Wuhan Central Hospital on its Weibo account says that Dr. Li is seriously ill and being resuscitated. I think this Doctor should be recognized internationally if he survives and of course, even should he relapse again.