Keep Manhattan, Just Give Me The Countryside

In another meeting this week at REIT Week in New York City I listened to Farmland Partners (NYSEMKT:FPI) CEO and Founder, Paul Pittman.

FPI, although only a public REIT for just over a year, has become a popular REIT - at least based upon the standing only crowd at the conference this week. I have also become tempted to plant a seed in the ground with FPI but have hesitated, primarily due to the company's unproven track record and small cap platform (the current market cap is just around $144 million).

Crops grow fast though: FPI IPO'd in April 2014 with around 7,300 acres and the company has since grown in size to around 70,000 acres (owned or under contract). The portfolio is broken down into 4 primary farming regions: Plains (21,946 acres), Delta (15,561 acres), Corn Belt (10,064 acres), and Southeast (22,362 acres).

The company (based in Colorado) has also begun to diversify with 35 tenants (farmers) and assets of over $300 million. The acquisitions were done at a weighted average cap rate of 4.95% and the weighted average cap rate of the portfolio is 4.67%.

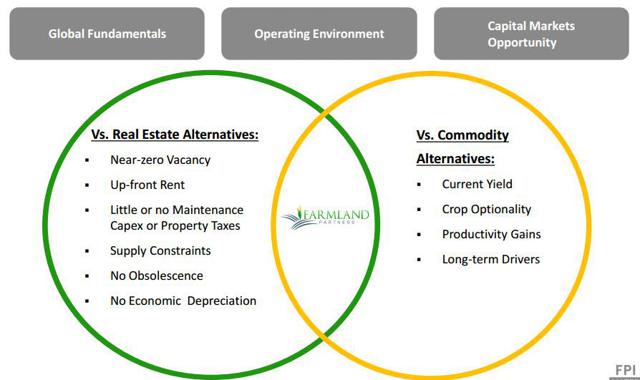

Most of Pittman's presentation at REIT Week was focused on the company's primary drivers, chief among them is Global Food Demand. Pittman stated that "farmland supply is in permanent land decline and will be". Accordingly he argued that farmland is an attractive asset class because it is a ZERO vacancy business model and because of the supply constraints and "paid up front" cash requirements, the fundamentals favor the Landlord.

FPI said that the company is buying farms at cap rates of around 5% and to fund the growth FPI has taken advantage of two 10-year bonds under its Farmer Mac facility, a $14.9 million, 10-year, interest-only bond at a fixed rate of 3.69% and a $11.2 million, 10-year, interest-only bond at a fixed rate of 3.68%.

The two 10-year bonds have a weighted average interest rate of 3.69% and extend the average maturity of FPI's debt. Additionally, FPI issued a $41.7 million five-year bond at 3.2%. The company currently has $149.0 million outstanding under its Farmer Mac facility. It also obtained an $8.1 million, 11-month, amortizing loan at one-month LIBOR plus 180 bps.

Continue reading this article here.

Brad Thomas is the Editor of the Forbes Real Estate Investor.

more