It’s Not A Bad Time To Rebalance

Maybe you don’t like a lot of fuss as an investor, and you want to buy-and-hold a simple portfolio for the long term. That’s fine, but you do have to rebalance periodically. And people who favor simplicity may do that rebalancing on a pre-set schedule – quarterly, semi-annually, or annually.

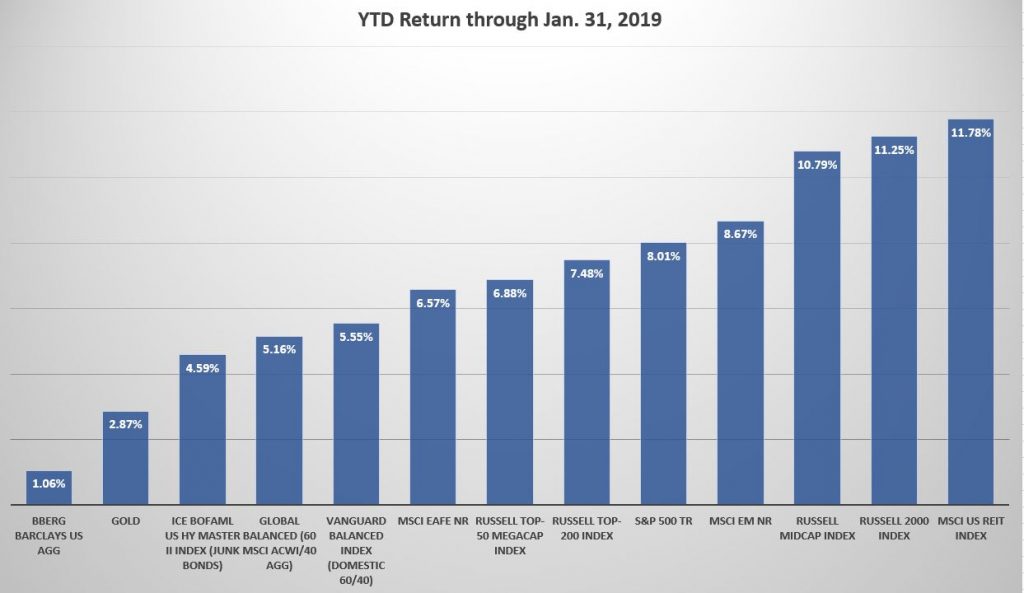

But if you want to be a little more active regarding your rebalancing, now’s not a bad time to consider doing it. Here are some asset class returns for the year through January 30, 2019:

You can see that stocks have done well, with the S&P 500 Index surging by around 8%. Small cap stocks have done even better, with the Russell 2000 Index rising more than 11%. Emerging markets stocks have bounced back too from a poor showing in 2018 with an 8.67% return for the first month of this year. And finally, with interest rates seemingly under control, REITs have topped the list with a gaudy 11.78% return.

If you started the year with a balanced portfolio of, say, $100,000, the $60,000 you had in stocks could now well be over $63,000. The $40,000 you had in bonds, by contrast, might not even be at $40,500 at this point. It’s not necessary to rebalance, but if you have a tax-advantaged account like a 401(k) or an IRA, and you can switch funds without paying fees or commissions, it’s not a bad idea. If your $100,000 is now close to $104,000 because of the $3000 you’ve made in stocks and a few hundred dollars in bonds, go ahead and move around $1,000 from stocks to bonds. That will get your stock exposure back to 60%.

That’s not a huge move, but the great investor, Benjamin Graham, who understood investor psychology before behavioral finance became an academic discipline, knew that investors get antsy to do something. And if fees, commissions, or taxes aren’t an issue, rebalancing is a good way to satisfy that itch to trade without doing yourself harm.

Besides satisfying the desire for activity, rebalancing can help you in other psychological ways. If you rebalance, and the market drops, you can feel happy that you took at least some money off the table – even if it was only a small amount. If, on the other hand, the market goes up, you can be satisfied that you didn’t alter your target (60/40) allocation; you just returned your portfolio to it after the January gains altered it, booking some profits in the process. You still have 60% of your money working in stocks.

There will always be woulda-coulda-shoulda thoughts when markets move. When stocks go up, you wonder why you didn’t have more money exposed to them. And when they go down, you wonder why you didn’t have less. But a balanced portfolio is one that most people can live with psychologically. It provides enough exposure when stock go up to minimize regret. And it provides enough bond exposure when stocks go down to minimize regret.

Investors should understand, however, that a balanced portfolio isn’t perfect. It may well return much less over the next decade than it has over the very long term. That’s because bond yields are so low that it will be virtually impossible for bonds to deliver more than 3.5%-4%, depending on your mix of Treasuries and corporates and your average maturity. Also, stocks are trading at high prices relative to past long-term earnings, which is usually a situation that produces lower-than-average future returns. That’s more incentive to rebalance in accounts that won’t hit you with transaction fees or a tax bill for doing so.

Last, if you think we may get some inflation, you can take that $1,000 away from stocks and put it in gold or leave it in cash. The economy isn’t robust on many indicators, but, according to DoubleLine fund manager Jeffrey Gundlach, inflation can come from all the quantitative easing the Fed has done and the large amount of U.S. debt outstanding. If a balanced portfolio is likely going to deliver subpar returns, and debt turns out to be a problem, holding some alternatives to stocks and bonds is reasonable.