Is Your Investing Like A "Bird Box" Challenge – Part 3

<< Read Part 1: Is Your Investing Like A “Bird Box” Challenge?

<<Read Part 2: Is Your Investing Like A "Bird Box" Challenge

In this 4-part RIA series, I urge investors to develop their “Gut Box,” and not remain blindfolded to the stories that are churned out by Wall Street and regurgitated by the front lines of big-box financial retailers. Their objective is to keep money invested in stocks regardless of how long it takes to recover from losses. Losses don’t matter to them. They matter to you.

Which brings me to the scion of Wall Street’s stories. The big daddy. The fable so entrenched it’s a religion.

It’s not if you heard this one – it’s how many times you’ve heard it.

“Stocks are for the long run.”

Heck, there are books about the topic everywhere. It’s a darn religion. To sell stocks or surgically exit markets is like striking a stake into the heart of your broker (or his wallet).

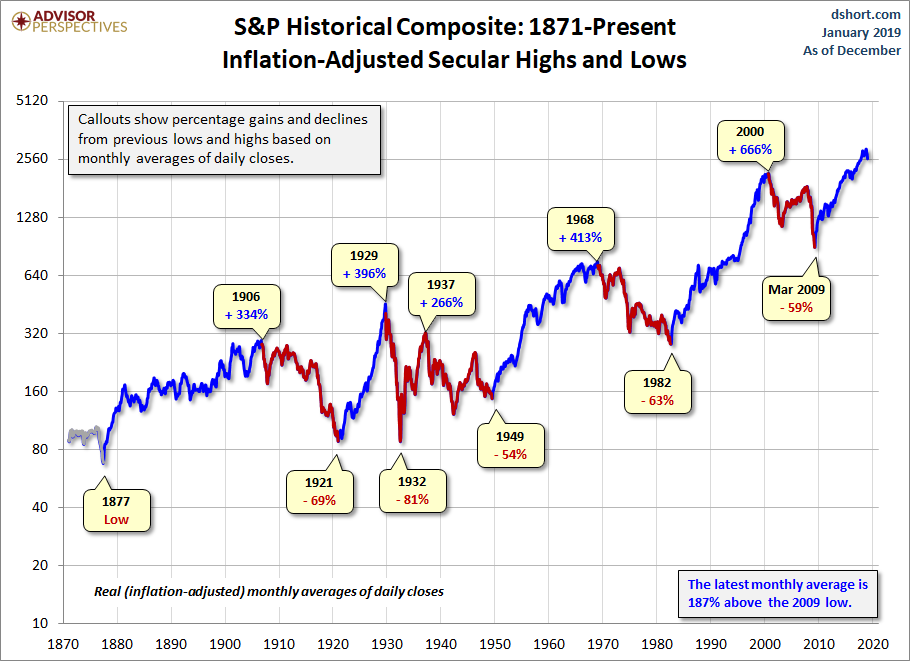

Speaking of stakes: Have you ever wondered how vampires have managed to become so wealthy and live in such lush mansions on big hills? Easy. They began investing in the stock market back in 1871 and never sold. They averaged that ethereal promise of 10% annual compounded returns for stocks!

Alas, as humans we do not possess such an opportunity. Not consistently, anyway. You see – institutions are infinite. As flesh & blood, we are finite. To markets, 10 years is a half beat from an eternal heart. To individual investors, a decade can be a heart attack.

I guarantee (in financial services, a guarantee is a four-letter word), that stocks will be higher in a century. I also guarantee that you won’t care either.

So, let’s adjust your gut box, shall we? Pay attention to the following tenets. Your wealth will thank you in the end (the human end).

Stocks are not safer in the long run.

Remember – it’s not stocks for the long term, it’s stocks for YOUR TERM.

Don’t be blinded by the panacea of stocks. Markets are irrational. Markets are driven by emotion. Even the father of Modern Portfolio Theory, Harry Markowitz wrote his seminal thesis originally for institutions, NOT people. The financial industry highjacked his work to sell product. Plain and simple.

Unlike the cancerous dogma communicated by money managers like Ken Fisher who boldly states that in the long-run, stocks are safer than cash, stocks are not less risky the longer you hold them. Unfortunately, academic research that contradicts the Wall Street machine rarely filters down to retail investors. One such analysis is entitled “On The Risk Of Stocks In The Long Run,” by prolific author Zvi Bodie, the Norman and Adele Barron Professor of Management at Boston University.

In the study, he busts the conventional wisdom that riskiness of stocks diminishes with the length of one’s time horizon. The basis of Wall Street’s counter-argument is the observation that the longer the time horizon, the smaller the probability of a shortfall. Therefore, stocks are less risky the longer they’re held. In Ken Fisher’s opinion, stocks are less risky than the risk-free rate of interest (or cash) in the long run. Well, then it should be plausible for the cost of insuring against earning less than the risk-free rate of interest to decline as the length of the investment horizon increases.

Dr. Bodie contends the probability of a shortfall is a flawed measure of risk because it completely ignores how large the potential shortfall might be. Sound familiar? It should. We write of this dilemma frequently here on the blog. Using the probability of a shortfall as the measure of risk, no distinction is made between a loss of 20% or a loss of 99%.

If it were true that stocks are less risky in the long run, it should portend to a lower cost to insure against that risk the longer the holding period. The opposite is true. Dr. Bodie uses modern option pricing methodology i.e., put options to validate the truth.

Using a simplified form of the Black-Scholes formula, he outlines how the cost of insurance rises with time. For a one-year horizon, the cost is 8% of the investment. For a 10-year horizon, it is 25%, for a 50-year time frame, the cost is 52%.

As the length of horizon increases without limit, the cost of insuring against loss approaches 100% of the investment. The longer you hold stocks the greater a chance of encountering tail risk. That’s the bottom line (or your bottom is eventually on the line).

There exists a formidable body of work that validates reducing equity exposure as markets break down. It’s not a ‘all in, all out’ story. It’s a surgical reduction saga. Sell until you can handle the motion. If you must sell all stocks in your portfolio to feel better, then frankly, you shouldn’t own stocks regardless of the conditions. It’s a harsh truth but best to face it.

Andrew Lo, professor of finance at the MIT School of Management, creator of the Adaptive Market Theory and co-author of A Non-Random Walk Down Wall Street outlines that stock price movements are all not random.

Today more than ever, stock prices balk at random walks. With the proliferation of algorithms with big mathematical hooks that grab on to the latest trend (up or down), stocks herd on steroids.

It’s crucial that an advisor maintains a sell or risk reduction strategy based on rules. No system is perfect. The key is to ask the question, understand the rules and then determine whether you agree with the sell philosophy. A surgical sell discipline isn’t active trading. It’s risk management. Time may or may not minimize your risk depending on how many months and years you’re willing to trade to get ahead or most likely, just breakeven which gets me to…

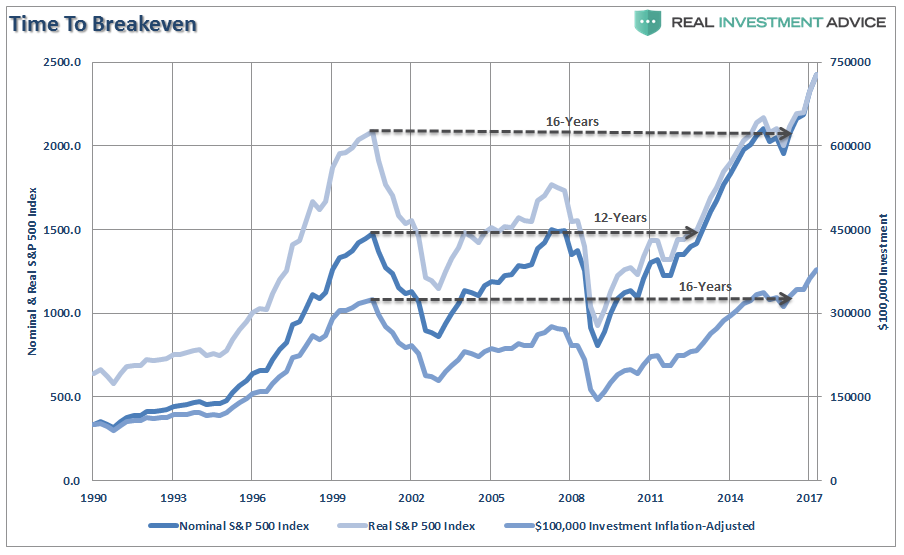

Investing to breakeven is NOT a strategy.

It occurs too often I meet with an investor who has wasted most of an investing life breaking even; where most of the portfolio “returns” are derived from human capital commitment or the ability to invest on a consistent basis. I cannot solely blame the stock market for such unfortunate outcomes. It’s a behavioral soup with a foundation in financial industry stretches of the truth that lethally mix with high fees, bad advice and a complacent attitude toward the lasting damage of bear markets (markets laugh at bears but bears damage humans).

Time grows increasingly precious. There’s a point where you painfully internalize its speed, comprehend its worth. Unlike markets that can disrespect time, laugh defiantly in its face – time as it moves ahead at hyper-speed, batters the human condition like storms against aging barriers. Investors recognize the luxury of waiting for recovery of wealth runs short. Scars remain where money once existed.

Realistically, you as a human probably experiences 20 uninterrupted years of saving before life gets in the way of a long-term plan – An illness, layoff, underemployment, caregiving for a loved one, college loans for children and grandchildren. The tribulations of life are not part of a broker’s story. Too depressing. So, how many years of breakeven are you willing to accept? Can your entire investing life be sadly dictated by breakeven? Yea, it can.

Harvesting stocks or selling, does not classify you as a trader (traitor).

Valid reasons exist (no, really), for the harvest of stock investments.

- Your portfolio allocation hasn’t been rebalanced in what feels like an eternity. Brokers are great at selling, not so great at ongoing portfolio maintenance or risk management which includes bringing stock allocations back into alignment with your emotionally-neutral allocation or willingness to take on risk. For example, if an agreed-upon allocation target is 30% stocks, 70% fixed income and stands at 45%, it’s acceptable to act to reduce stocks to 30% and increase cash or bond exposure. With Fed Chair Powell seeking to relent to stock markets perhaps due to slowing economic growth, the “Powell Put” has provided a brief tailwind to stocks which is an opportunity to sell.

- The risk-reward for stocks vs. cash isn’t as appealing during a market cycle. In the brokerage biz, cash is trash. The mandate from upper management (or lose your job) is cash must be monetized, cemented into managed product for fee revenue.

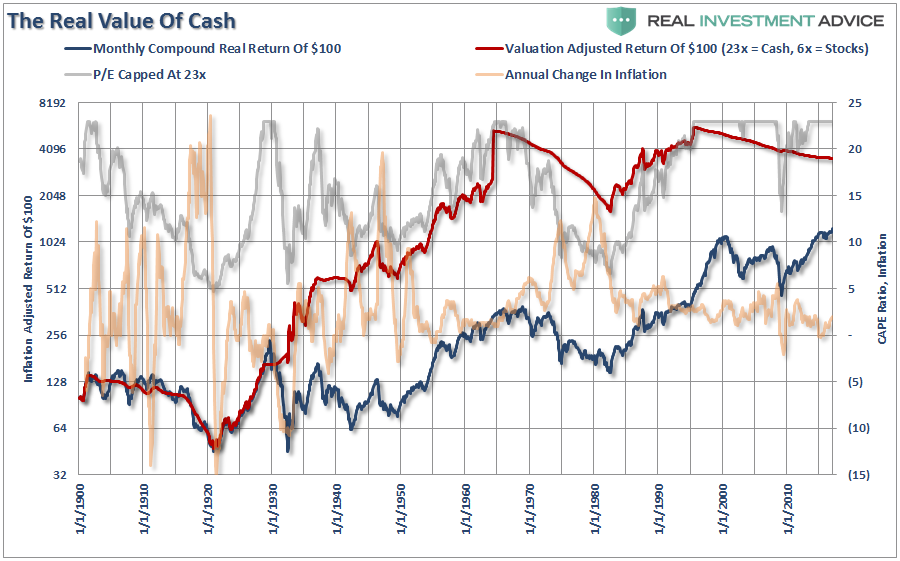

Below is a chart we feature at our Retirement “Right-Lane” Class. One of my favorites.

Here, RIA’s Chief Investment Strategist Lance Roberts outlines the inflation-adjusted return of $100 invested in the S&P 500 (capital appreciation only using data provided by Dr. Robert Shiller). The chart also shows Dr. Shiller’s CAPE ratio. Lance caps the CAPE ratio at 23x earnings which has historically been the peak of secular bull markets. He then conducts a simple cash/stock switching model which buys stocks at a CAPE ratio of 6x or less and moves back to cash at a ratio of 23x.

During the great inflation of the 1970s in the United States, the value of cash experienced downward pressure. In other words, although the CAPE ratio in 1970 was roughly 23x, the switch to cash didn’t work so well.

Today, with the Shiller PE at roughly 29x, the 2-year Treasury yield at 2.467% and cash in money markets earning close to 2%, a tactical overweight to cash and short-duration bonds is not a bad idea. Per the Federal Reserve Bank of Dallas’ Trimmed Mean PCE Inflation Rate which stands at an annualized rate of 1.9%, inflation doesn’t appear to be out of control. In other words, the maintenance of cash shouldn’t place your long-term personal rate of return targets in jeopardy.

Brokers lament – “Cash isn’t working for you! Cash will lose to inflation!” Well, there are times when cash will do just that. However, it’s the responsibility of your money manager to make portfolio adjustments. The ebb and flow of portfolios to adjust for risk is a responsibility most brokers will not undertake therefore they must trash cash regardless of valuations and the overall health of the market.

REMEMBER – It’s not cash forever; it’s cash for now.

As Lance so eloquently states –

“While no individual could effectively manage money this way, the importance of “cash” as an asset class is revealed. While cash did lose relative purchasing power, due to inflation, the benefits of having capital to invest at lower valuations produced substantial outperformance over waiting for previously destroyed investment capital to recover.

While we can debate over methodologies, allocations, etc., the point here is that “time frames” are crucial in the discussion of cash as an asset class. If an individual is “literally” burying cash in their backyard, then the discussion of the loss of purchasing power is appropriate.

However, if cash is a “tactical” holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.”

Much of the mainstream media will quickly disagree with the concept of holding cash and tout long-term returns as the reason to just remain invested in both good times and bad. The problem is it is YOUR money at risk. Furthermore, most individuals lack the “time” necessary to truly capture 30 to 60-year return averages.

Stocks are one alternative to growing and preserving wealth. They’re not the only investment in town. There is no time period (unless you’re Dracula), where stocks should be considered ‘safe.’ There are cycles where risk vs. reward are in an investor’s favor. There are occasions when taking on more risk does not generate a commensurate or greater degree of return. Sometimes, it’s merely taking on more risk.

It’s the responsibility of an advisor to establish and communicate realistic expectations for future returns for risk assets and assess whether stocks are a head or tailwind to achieving financial objectives.