Is This 6.4% Yield About To Get Slashed?

Shipping companies, particularly oil and natural gas transporters, have been notorious dividend cutters over the past few years. The trend is due in large part to plummeting oil and gas prices.

For example, Teekay Corp. (NYSE: TK) slashed its quarterly dividend by 90% to $0.05 per share. This took place just six months after it raised the dividend to $0.55 from $0.32.

Nordic American Offshore Ltd. (NYSE: NAO) has consistently lowered its quarterly dividend since it started paying one in June 2014. Factoring in this month’s cut, it has gone from paying $0.45 to $0.05.

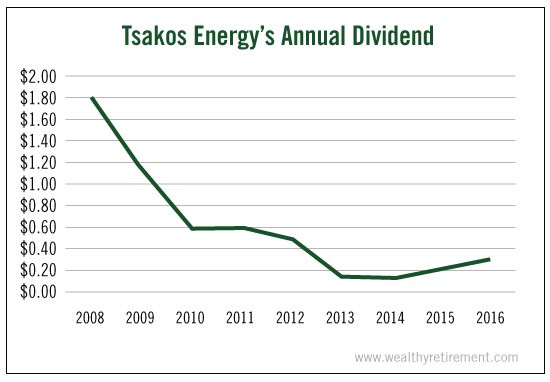

And Tsakos Energy Navigation (NYSE: TNP), the subject of this week’s Safety Net column, cut its dividend from a high of $0.90 per share in 2008 to a low of $0.05 in 2013.

However, unlike Teekay and Nordic American, Tsakos has raised its dividend in 2015 and 2016. It now stands at $0.08 per share, or $0.32 annually. That gives the stock a 6.4% yield.

Can it sustain such a respectable yield considering energy prices are still fairly low?

If you look at the company’s free cash flow, the answer is a definitive no.

Short on Cash

Last year, Tsakos generated $17 million in free cash flow. It did this while paying shareholders $33 million in dividends.

In other words, for every dollar it brought in the door, Tsakos paid shareholders $1.98. That’s not sustainable.

Especially when you consider that this year, free cash flow is projected to be negative.

The Best Long-Term Investment Strategy

Don’t invest in just any dividend-paying stock... Pick up shares of the 10 best “Dividend Aristocrats” - stocks that have increased their dividends every year for the past 25 years. But not all of these stocks deserve a standing ovation, so we’ve picked the 10 best based on yield and payout ratio.

Besides paying more than it can afford in dividends, the company is also buying back shares with money it doesn’t have.

It recently completed a $20 million share buyback at an average price of $5.59 per share. That’s about 10% higher than today’s stock price. And management recently announced a new $20 million repurchase program.

Sure, Tsakos has $290 million in cash. But it also has $320 million in short-term debt to pay off or roll over to new debt. And it has $1.1 billion in long-term debt.

Between 2008 and 2012, Tsakos cut its dividend four times. SafetyNet Pro does not like that and neither do I.

Given its history of dividend cuts and the fact that Tsakos doesn’t generate enough cash to pay its dividend, there’s no doubt that Tsakos’ dividend is in jeopardy.

Dividend Safety Rating: F

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker symbol in the comments section below.

Good investing,

Marc

Disclaimer: Nothing published by Wealthy Retirement should be considered ...

more