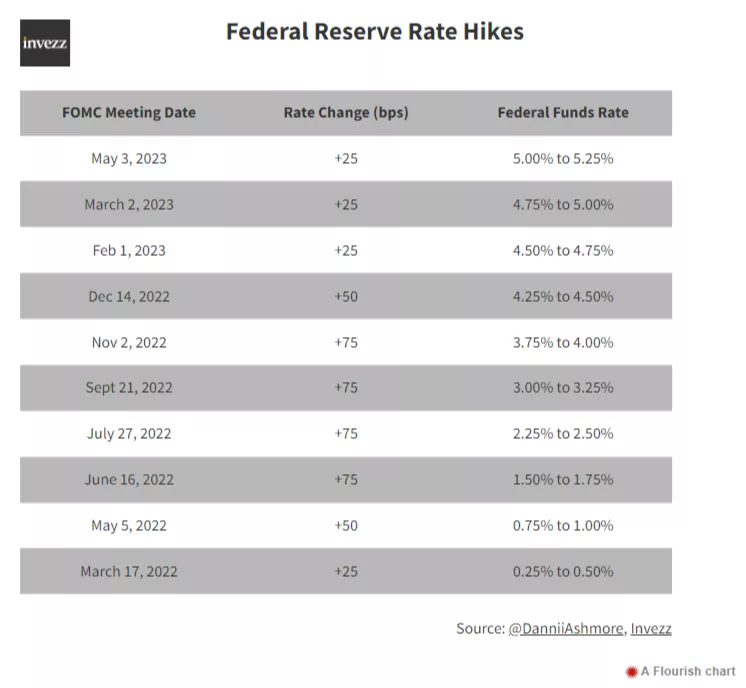

I published a piece this week looking into the Federal Reserve’s interest rate decision Wednesday, assessing whether it was reckless to hike again in the current climate.

The decision came and went as expected, the Federal Reserve hiking rates another 25 bps. As I wrote yesterday, however, this was largely priced in, and it was the language of Fed chair Jerome Powell that was likely to be the more influential on markets.

That language was more hawkish than some investors were hoping for, as Powell did not seem enthused by the prospect of rate cuts.

“We on the committee have a view that inflation is going to come down not so quickly”, he said. “If that forecast is broadly right, it would not be appropriate to cut rates”.

Despite the hawkish tone, stocks were relatively stagnant. The tech-heavy Nasdaq, perhaps the most sensitive to interest rate policy, closed Wednesday down 0.5%.

Yet despite cuts seemingly ruled out, the language was certainly softer than previous meetings. Language that further hikes “may be appropriate” was removed, with Powell noting in his press conference after that the change was “meaningful”.

Inflation remains the priority for the Federal Reserve

The interesting thing here is that inflation is somewhat of a human-created phenomenon, too. Obviously, there are tangible factors that crate inflation in the first place – supply chain issues, the war in Russia, incessant money printing and so on. But there is also the economic fact that the expectations of future inflation can cause inflation today, like a self-fulfilling prophecy.

That is because future inflation will cause people to spend more today as they anticipate future price rises, thus precipitating those exact expectations. Secondly, on the labour side, workers seek wage rises, which again contributes towards further inflation.

This is likely part of the reason that the Fed is taking this hawkish line. In truth, the prospect of rate cuts must be coming closer. We have seen weaker economic data of late showing true softness, while the banking sector is obviously creaking under the pressure of these elevated rates.

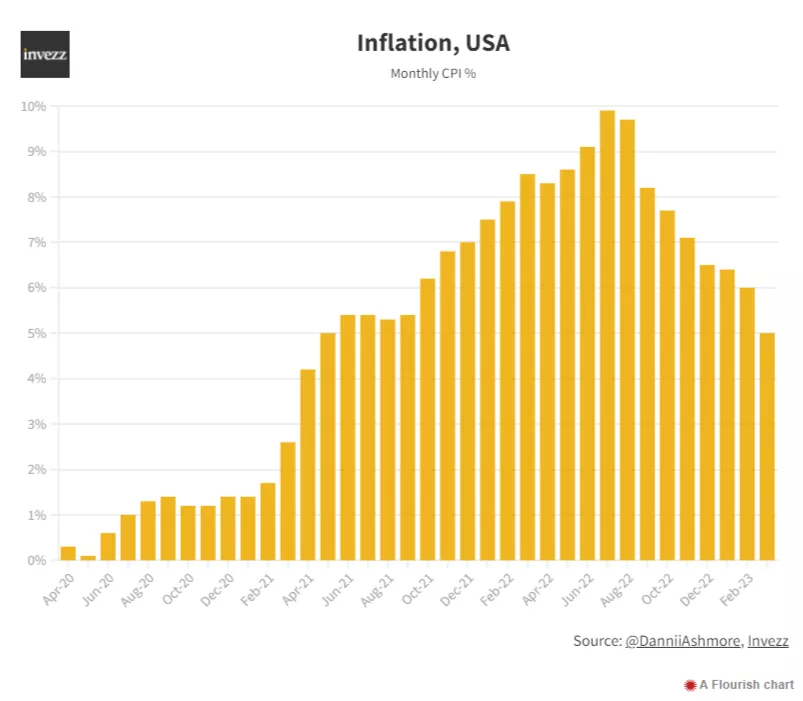

And while inflation remains well north of the 2% target, it has come down a long way from its peak (9.9% last July).

That said, as I wrote yesterday, this latest hike hammers home what we knew already: the Fed’s number one priority really is inflation. Hiking this deep into a tightening cycle, with what is happening in the banking sector, is a very aggressive line.

But should we be surprised? Not really. I’m not sure I agree with one last hike in this climate, when a wait-and-see approach until next month may have been more prudent, but the Fed is determined not to release the market quite yet, and risk inflation spiking back up. And while the above chart shows inflation coming down, it also shows a 5% number – far beyond what the Fed deems as acceptable, with that 2% target unlikely to be hit anytime soon.

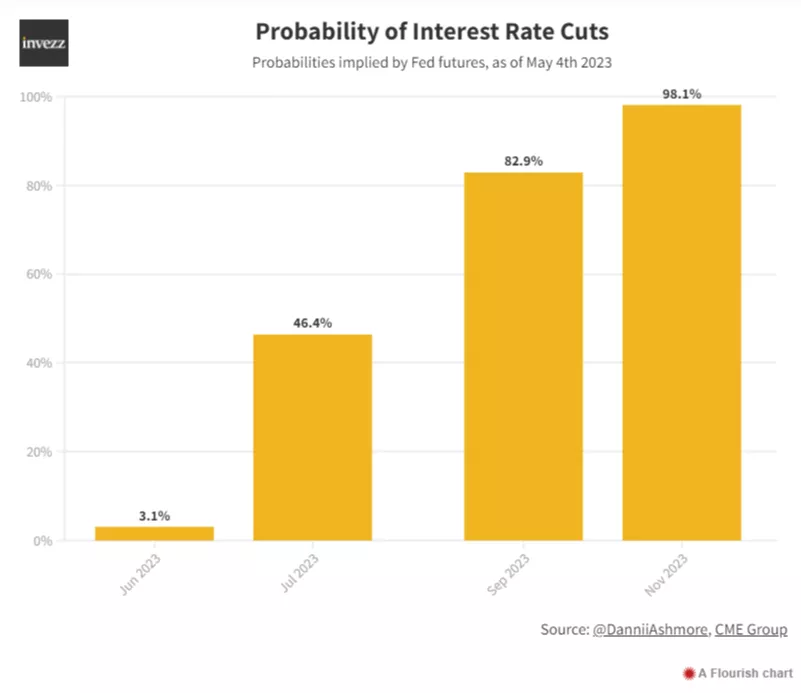

Market is not believing the Fed

As worrisome as the banking issues are, it still feels unlikely that there is a true systemic issue here – while regional banks are in a very bad state, it is certainly not on the level of 2008 when balance sheets were bogged down by terrible assets (subprime mortgages). This time around, it is poor risk management again, but it is more of a liquidity crisis as banks are holding more reputable bonds, they have just fallen in value significantly as a result of the interest rate hikes.

Looking at the probabilities backed out by Fed futures, the market knows that the Fed may be forced into cuts sooner than anticipated. Obviously, a lot will depend on the CPI data going forward, as well as the banking concerns, but the forecast right now shows a market calling the Fed’s bluff.

Futures may only imply a 3% chance of rate cuts at the next meeting (June), but there is a 46% chance of cuts happening by the next meeting (July), while one more (September) sees the probability rise to 83%.

And so, it appears very likely that the fastest tightening cycle in recent memory has come to a close. Eyes will now be squarely focused on economic data going forward, as the fear of a recession looms large.

It is economics 101 that aggressive tightening of monetary policy sucks liquidity out of the economy and risks a slowdown. Indeed, that is the very point, and how to combat inflation. Of course, the risk all along has been that the Fed will hike too aggressively, things will break and the economy will spiral into a nasty recession.

We are getting to the point where we are about to find out if that is true, or whether the coveted soft landing remains a possibility. But either way, the market is not believing language out of the Fed right now – investors are declaring, at the very least, that hikes appear done for now.

More By This Author:

USD/CAD Forecast: Signal Ahead Of US, Canada Jobs Data

Meta Stock Price Forecast: Mark Mahaney Sees Another 45% Upside

First Republic Bank Collapse Is Underway As FDIC Seeks Rescue

Comments

Log in or sign up to join the conversation.