Inflation And Broken Windows

Gripping Hand Update

As I have been repeating all month (see here, here, and here), anything I say about the economy or markets is subject to the coronavirus “Gripping Hand.” It greatly constrains the available options. Other possibilities open up if we manage to get and keep the virus under control.

Bluntly, conclusion first: You cannot predict inflation or deflation until you understand the extent of the virus this summer. You get to radically different outcomes, which I will discuss at the end.

The good news is that US vaccinations are accelerating. States and the federal government are working out bugs in the process. Supply constraints are easing a bit. It is still going much too slowly, but was always going to be an ordeal. The single-dose Johnson & Johnson (JNJ) vaccine should be approved soon and will help. With luck, everyone who wants to be vaccinated should have the chance by this summer.

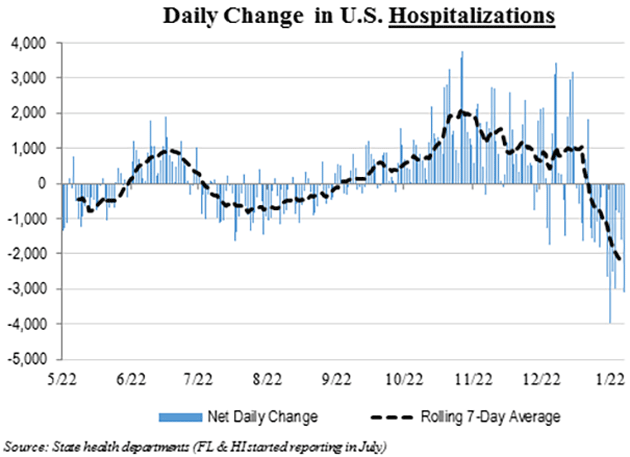

Let’s look at a few charts. First of all, hospitalizations are way down. That is very good news.

Source: Justin Stebbing

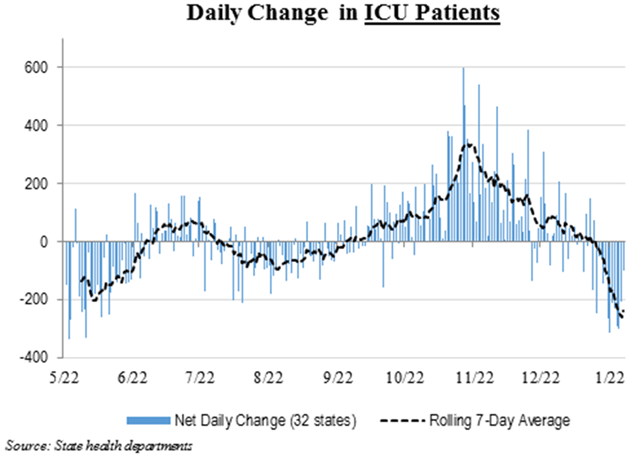

Ditto for ICU patients:

Source: Justin Stebbing

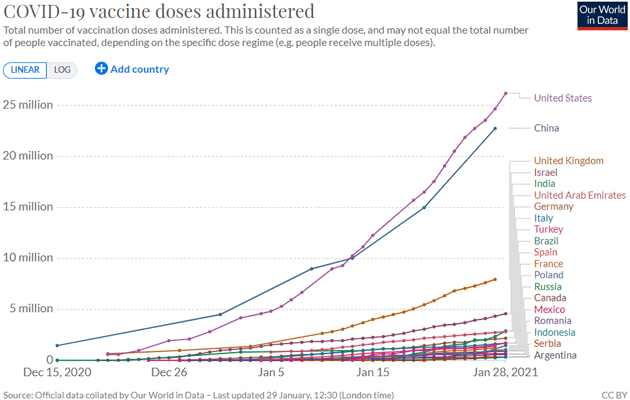

The testing positivity rate and number of new cases are dropping, too. Well over 27 million people in the US have had at least one vaccine dose, with about 1.3 million more doses administered each day.

Source: Our World in Data

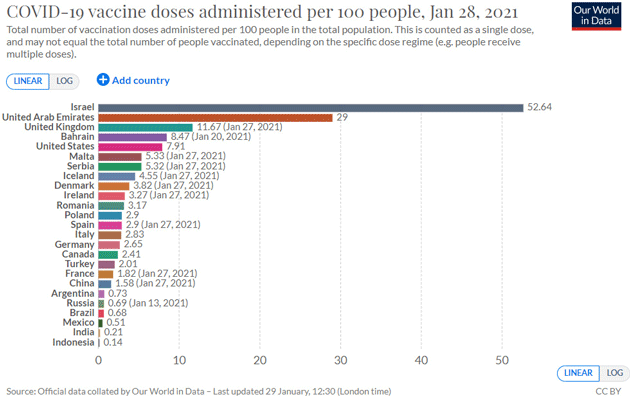

Here is another chart comparing the responses of various countries. We must remember that we have to vaccinate the world to keep a new strain/variant from popping out and starting this process all over again.

Source: Our World in Data

The next question is whether that will be enough. The winter surge is reversing, but the B117 and other more infectious variants could send case numbers and hospitalizations higher again, and possibly a lot higher. And even with recent improvement, the numbers are still worse than they were at last summer’s peak.

Back with a Vengeance

Thinking positively, imagine the US and other major economies vaccinate enough people in the next few months to let semi-normal life resume. We’ll still be cautious, but the generalized fear subsides enough to let us circulate again. Restaurants, hotels, airlines, and other hard-hit industries start to get back on their feet. Then what?

Scenarios like that usually point to inflation. Pent-up demand will make people spend some of the extra savings they accumulated (often via fiscal aid programs) in the last year. Possible? Yes, but I don’t expect it. I think this experience is scarring many people in the same way the Great Depression scarred our parents, giving their generation a permanently thrifty attitude. We’ll see.

But inflation can come from other directions, too. My friend Louis Gave recently described the larger forces at play.

I think inflation will come back with a vengeance. One of the key deflationary forces in the past three decades was China. I wrote a book about that in 2005; I was a deflationist then, as my belief was that every company in the world would focus on what they can do best and outsource everything else to China at lower costs. But now, we’re in a new world, a world that I outlined in my last book, Clash of Empires, where supply chains are broken up along the lines of separate empires. Let me give you a simple example: Over the past two years, the US has done everything it could to kill Huawei. It’s done so by cutting off the semiconductor supply chain to Huawei. The consequence is that every Chinese company today is worried about being the next Huawei, not just in the tech space, but in every industry. Until recently, price and quality were the most important considerations in any corporate supply chain.

Now we have moved to a world where safety of delivery matters most, even if the cost is higher. This is a dramatic paradigm shift… It adds up to a huge hit to productivity. Productivity is under attack from everywhere, from regulation, from ESG investors, and now it’s also under attack from security considerations. This would only not be inflationary if on the other side central banks were acting with restraint. But of course we know that central banks are printing money like never before.

The pandemic is clearly accelerating some pre-existing trends. Globalization was already starting to slow and possibly reverse for technological reasons. President Trump’s trade war gave more impetus to “Buy American” and “Buy Local” policies, and Biden seems intent on continuing them. And now COVID-19 gives national governments everywhere reason to be as self-sufficient as possible. Businesses feel the same pressure.

But what really matters is how the Federal Reserve responds if price inflation pushes interest rates higher. Louis believes the Fed will enact some kind of “yield curve control” to keep long-term Treasury yields near 2%. This will tank the dollar, raising inflation but sending “real” interest rates even more negative than they are now, thereby helping finance fast-growing government debt (TLT).

This scenario would be good for gold and terrible for bonds. But it’s not the only scenario, so let’s turn next to my favorite bond bull.

Broken Window Fallacy

Lacy Hunt of Hoisington Investment Management has been steadfastly bullish on Treasury bonds for 39 years. He saw what Paul Volcker was doing and became a monster bond bull. He has been exactly right. His argument is really just simple math. To summarize:

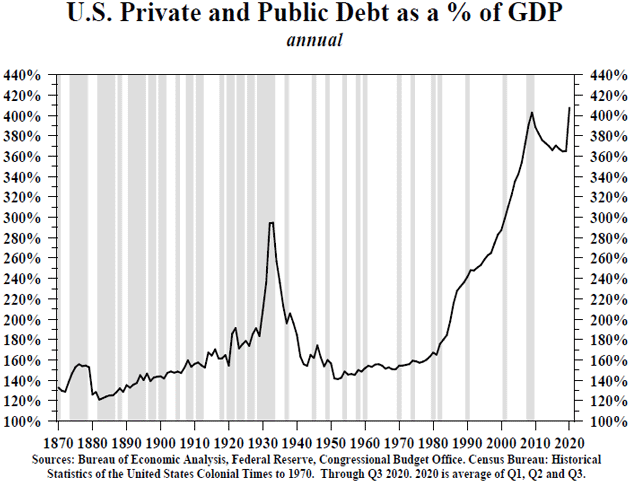

- Growing public and private debt suppresses economic growth as the additional debt has a smaller and smaller effect.

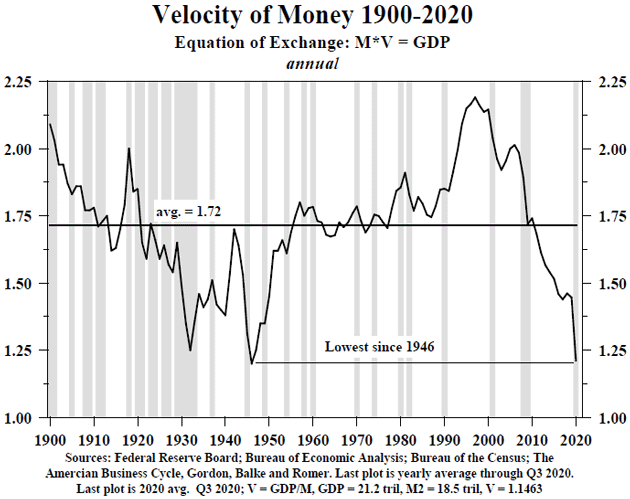

- The low growth reduces velocity of money, without which sustained general inflation is impossible (though there can be inflation in some segments).

- Inflation being the major determinant of Treasury yields, those yields will move lower.

In his latest report, Lacy takes on the idea that fiscal stimulus plus recovery from the pandemic will spark inflation. He notes that any GDP growth from here won’t reflect the pandemic’s vast wealth destruction. He compares it to the famous Frederic Bastiat/Henry Hazlitt story of the broken bakery window. Fixing the damage boosts GDP, but you don’t see the other costs incurred or opportunities missed. Just as we can’t grow the economy by breaking each other’s windows, we can’t expect pandemics or other disasters to be beneficial.

He also points out (and Louis Gave does, too) that most fiscal stimulus has a small and maybe negative multiplier effect. Governments aren’t “investing” in new productive capacity or building anything new. They are simply transferring money between taxpayers, bondholders, and benefit recipients. This may be necessary in the short term, but it also misallocates resources and reduces future growth.

Lacy saves his real fire for our overuse of debt. This isn’t new but the pandemic has accelerated it.

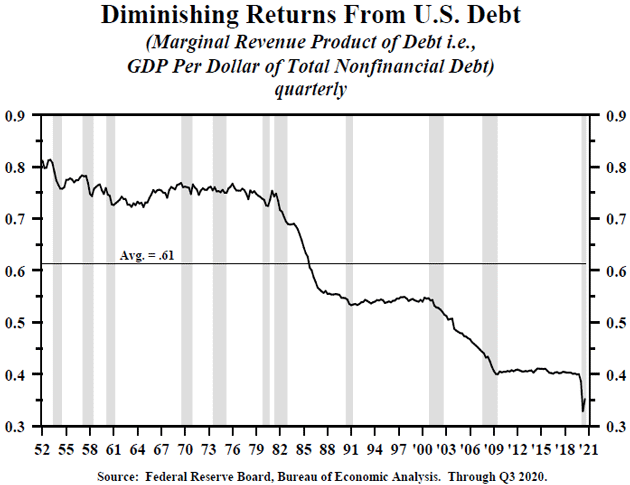

When debt capital, like any other factor of production, is overused its marginal revenue product declines. This serves as a persistent drag on economic activity that restrains growth despite the best efforts of monetary and fiscal policy. The decline in the marginal revenue productivity of debt, due to the pandemic, must now operate with even weaker demographics around the world. The pandemic resulted in considerably lower marriage and birth rates which will have negative long-term consequences for domestic and global growth. Based upon the universally applicable production function, the capability of achieving historical rates of economic growth will be even more difficult in the years ahead.

Source: Hoisington Investment Management

The Federal Reserve is trying to stimulate an economy that already had too much debt with yet more debt. No surprise, it’s not working, though it is boosting stock/asset/housing prices. Most of their stimulus simply stays on the sidelines. This is very clear in the velocity of money, which was already trending lower but fell sharply in 2020.

Source: Hoisington Investment Management

At the most basic level, this is just plumbing. Water flows downhill. Inflation is hard to imagine unless that velocity line turns higher. But water can still splash for short periods. Velocity rose sharply in the post-WW2 years when, not coincidentally, the Fed was engaged in the kind of yield curve control Louis Gave expects.

My friend David Rosenberg agrees. He did a very interesting podcast with Grant Williams and Stephanie Pomboy. Quoting from the transcript:

David Rosenberg: So look, I would just say that you can almost dust off your slide package from 12 years ago. The same people calling for inflation now were calling for inflation back then. They’re the ones that have to answer as to why it is that inflation in the final analysis even with a stock market that quintupled, and even with a bull market and commodities, and even with 3-1/2% unemployment, we never did get the big inflation. So they’d have to come and explain why all of a sudden we’re going to get inflation in the coming cycle that we couldn’t get in the previous, not just one, not just two, but the previous three cycles.

Stephanie Pomboy: What worries me about it is that I totally agree with you on those forces of deflation or disinflationary forces that are clearly evidenced over that whole period …. But that doesn’t preclude people from getting all hot and bothered and getting chinned up on an inflation scare. They see the dollar going down, they see import prices going up and they assume, okay, well, that’s going to lead to CPI inflation, never mind that as you point out it didn’t for the last decade or even longer, but what is the possibility?

David Rosenberg: [At] the end of the day though, we have the most unpatriotic development you could ever think of, which is that Americans have paid down their credit card balances at a 14% annual rate over the past six months. It’s never happened before. And so it’s very difficult to get inflation when there’s no credit creation, which is what the money velocity numbers are telling you, or where there’s no significant wage growth. Where’s the wage growth going to come from? It’s very interesting that the same people that tell you about inflation are so bulled up on the economic outlook, they believe that full employment is still somewhere at or below 4%.

And of course the Fed’s forecast is that the next few years we’re going to get back to that magical level below 4%. But let’s just say that we have a situation where one in eight Americans is either unemployed or underemployed. There’s still tremendous idle capacity in the labor market. We have a capacity realization rate in industry that’s around 74%. We’re nowhere near the conditions, in terms of the capacity pressures in the economy, that’s going to lead to a sustained increase in inflation. It doesn’t mean that you don’t get some temporary periods of pass through in the goods-producing side from commodities in the weaker dollar, but that’s not lasting inflation.

So which will we get? I suspect both. First off, this summer we will have very low comparisons for inflation if you only look back for 12 months. If we get even a modest recovery in the COVID numbers, we clearly could see some short-term “inflation” in annual data from those weak comparisons. It won’t last. If you look back 24 months (which we never do) you would see inflation still under 2%. And for the record, annualized PCE inflation, the Fed’s favorite measure, is only 1.3% annually today. We have a long way to go to get to 3%.

The debt burden will cap growth enough to keep the inflation mild. It won’t be another 1970s period of sustained inflation. But it might be enough to send gold to record highs. A lot depends on how much inflation the Fed chooses to tolerate. Their recent signals indicate it may be a lot more than we’ve seen in this century. I don’t think they get worked up until inflation is well north of 3% for six months to a year. They have made it clear they want inflation to “average” 2% for a period of time. That means they have to overshoot that target to get that average.

Implications

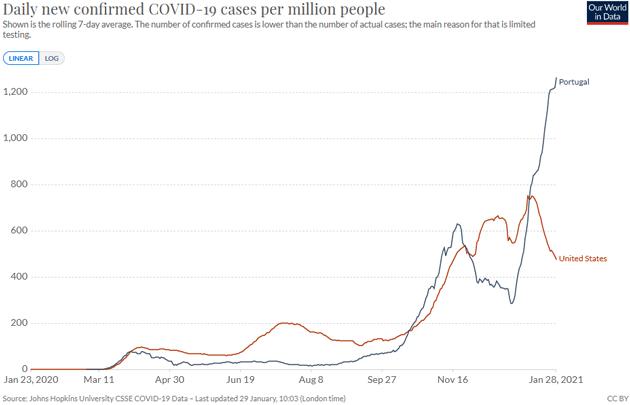

To get inflation, we have to assume that we have controlled the gripping hand of the coronavirus. Look at what’s happening in Portugal, where B117 recently began taking off.

Source: Our World in Data

This looks almost exactly like the Irish problem I mentioned two weeks ago. Notice that barely a month ago, Portugal was seeing a steep drop in cases per million, much like the US is today. Then boom!

We really need to avoid such a spike here, first of all to save lives, but also economically. People would stay home and businesses close voluntarily even if governors don’t order it, further devastating our already-weakened economy.

Former FDA commissioner Scott Gottlieb, looking at CDC data, thinks 50% of US coronavirus cases will be the B117 variant by the end of February. If this is the case (and we will know in a few weeks), then it means another very serious spike in cases.

This would leave governors no good choices. Lockdowns which are increasingly shown to be ineffective? No lockdowns and let it run? Nothing but bad options. Fortunately, we are getting better medicines to deal with the disease. The Cleveland Clinic has begun sending nurses to administer IV drugs in patients’ homes, avoiding hospitalization. We will see more such innovation and it will help.

Nevertheless, in a variant-driven spike event, the modestly recovering economy will probably fall back into recession. Recessions are by definition deflationary events.

Obviously we all hope to avoid that, and I think it is quite possible. A few more weeks of solid vaccine progress, warmer weather, continued distancing and other precautions, plus a little luck, might do the trick. But there is no time to waste. I urge everyone: Get vaccinated as soon as it is available to you, and keep avoiding crowds and all the other standard measures. That is the best way you can help the economy, and particularly the small businesses that have been hit so hard. We can get through this but it will require everyone’s cooperation.

Other risks remain, too. Scientists think the current vaccines will still work against the known variants, but that is not yet certain. The South African and Brazilian variants are already in the US (I have actually been to Manaus where the Brazilian variant came from). Other variants could appear, too.

It’s also still unclear how long immunity lasts, whether from vaccines or from prior infection. And more than a few people simply don’t want the vaccine, for whatever reason. Reaching “herd immunity” is not a sure thing even when vaccinations crank up.

Then there is the rest of the world. Truly solving this problem requires global herd immunity, which means billions of vaccinations. That part of the battle has barely begun and could take several years.

So the gripping hand, aside from superior strength, has independently moving fingers. We need them all to relax before we can relax. And oddly, that happy outcome might trigger the kind of inflation we’d rather not see. But I don’t expect it this year. And the bigger we build our debt in the US and Europe, the less likely inflation becomes.

If we overcome the virus, the dollar likely continues lower, although the eurozone is already trying to figure out how to manipulate the euro lower. If we get that spike here? And it shows up in the rest of Europe like it did in Portugal? The dollar bears could get their face ripped off. I think gold does well in any event. Sadly, every prediction and outcome is still in the Gripping Hand. Stay tuned…

Disclaimer:The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One ...

more