How Tech Unicorns Are Just Like China’s "Ghost Cities"

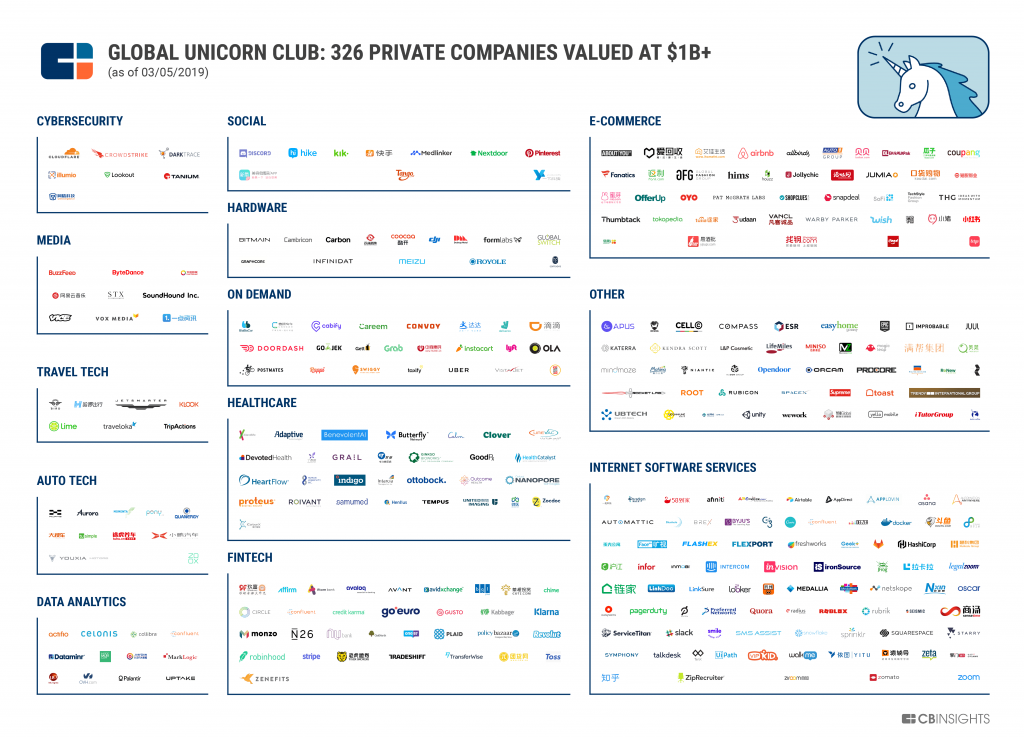

Since the Great Recession, there has been an explosion of interest and activity in the tech startup arena. Tens of thousands of tech startups have been founded in recent years and there are now over three hundred new “unicorn” startups that have valuations of $1 billion or more. The startup gold rush began as countless entrepreneurs attempted to follow in the footsteps of Facebook founder Mark Zuckerberg and the “Google Guys,” Larry Page and Sergey Brin. Unfortunately, the majority of today startups – including today’s hottest unicorns – are burning copious amounts of cash. In this piece, I will make the case that today’s startup phenomenon is very similar to China’s construction of countless empty “ghost cities” for the purpose of creating jobs and economic growth.

Though the U.S. was the epicenter of the Global Financial Crisis of 2008 and 2009, China’s economy was still strongly affected as well. After all, China’s largest export market – the U.S. – had just succumbed to a powerful recession. In an attempt to cushion the economy and create growth again, China’s government announced a RMB¥ 4 trillion (US$586 billion) stimulus package and helped to encourage an aggressive debt binge. A good portion of this stimulus package and debt binge was used to build massive infrastructure projects, extravagant government buildings, and entire cities throughout the country.

A very high proportion of China’s construction projects over the past decade were basically make-work projects that were undertaken for the purpose of creating jobs and GDP growth, despite the fact that they are typically wasteful and inefficient. Make-work projects are very common in centrally-planned economies like China. The economist John Maynard Keynes was a strong proponent of make-work projects and is even known for saying, “the government should pay people to dig holes in the ground and then fill them up.”

As an adherent of the pro-free market Austrian School of economics, however, I vehemently disagree with make-work projects and Keynesian-style stimulus programs because they create tremendous waste and misallocation of resources, which ultimately leaves society poorer in the long-run. China’s numerous empty “ghost cities” are an eerie reminder of the gross misallocation of resources that has occurred in the past decade. China’s government and real estate developers were hoping that “if you build it, they will come,” but that hasn’t proven true for many of the country’s brand new cities and malls that are almost completely devoid of people. There are an incredible 65 million empty apartments in China currently, which amounts to approximately a fifth of the country’s housing stock.

The pictures below show some examples of these empty cities:

Meixi Lake development near the city of Changsha. Source: Kai Caemmerer

Zhengdong in Zhengzhou in Henan Province. Source: Wade Shepard

Evergrande Splendor Kunming. Source: J Capital Research

Now, it’s time to discuss why the startup mania of the past decade is very similar to China’s construction of grandiose infrastructure projects and ghost cities. In addition to the housing and stock market plunge, the U.S. lost 8.7 million jobs during the Great Recession, so the Federal Reserve was desperate – just like China was in 2009 – to engineer another economic boom to create jobs and GDP growth again. China relied more heavily on fiscal stimulus, while the U.S. relied more heavily on monetary stimulus. The Fed cut and held interest rates at ultra-low levels for much of the past decade and pumped trillions of dollars worth of liquidity into the U.S. financial system via its quantitative easing programs. Unfortunately, dangerous economic bubbles and other distortions form when central banks and governments aggressively interfere with financial markets, especially interest rates. The chart of the Fed Funds rate below shows how bubbles form when interest rates are at low levels:

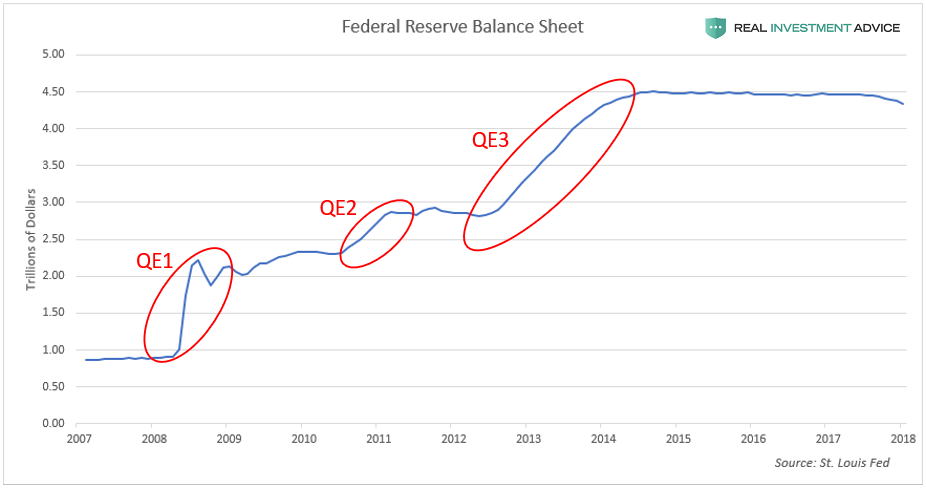

The Fed pumped trillions of dollars worth of liquidity into the U.S. financial system via its quantitative easing programs, which can be seen in the chart of the Fed’s balance sheet since QE started in 2008:

When central banks use monetary stimulus to create an economic boom, they usually succeed (until the boom turns into a bust, of course). What they don’t know, however, is what sectors of the economy are going to boom as a result of their stimulus. Each cycle is different – it was telecom and dot-coms in the late-1990s, housing and banking in the mid-2000s, and tech startups in the current cycle. The explosion of venture capital activity over the past several years can be seen in the chart of the monthly count of global VC deals that raised $100 million or more:

Trillions of dollars worth of central bank-created liquidity has been sloshing around the globe looking for a home, and a portion of it found its way into unicorn companies that are worth billions of dollars each. Most of these unicorns came of out virtually nowhere and amassed tremendous valuations despite hemorrhaging cash, which is a tell-tale sign of a bubble.

The majority of startups and unicorns are burning astounding amounts of cash – even those that have made it all the way to the IPO stage. For example, the 15 tech unicorns that went public over the past three quarters lost a combined $6 billion in 2018 despite having a lofty combined valuation of $178.3 billion.

Like China’s grandiose infrastructure projects and ghost cities, the majority of today’s tech startups only exist – at least at their current scale – because of stimulus, and are not economically viable, as evidenced by the billions of dollars they are hemorrhaging with no end in sight. China’s infrastructure projects and ghost cities and today’s tech startups serve essentially the same purpose – to create jobs and GDP growth, economic viability be damned.

The creation of tens of thousands of tech startups leads to the hiring of scores of technology professionals, renting tremendous amounts of commercial office space, buying computer and office equipment, and paying for professional services, which all serve to boost economic activity. Meanwhile, the boom that is driving all of that activity is basically bogus. The same phenomenon occurred during the mid-2000s housing bubble when soaring housing prices led to a surge of construction and lending activity, which created jobs for construction workers, real estate agents, and mortgage bankers. Of course, when the housing bubble burst, many of those workers lost their jobs; I expect today’s tech startup bubble to end in a similar fashion.

As stated throughout this piece, government and central bank interference in the economy creates dangerous distortions, bubbles, and waste. Austrian School economists call this kind of waste and bad investments “malinvestment” –

“Malinvestment is a mistaken investment in wrong lines of production, which inevitably lead to wasted capital and economic losses, subsequently requiring the reallocation of resources to more productive uses. “Wrong” in this sense means incorrect or mistaken from the point of view of the real long-term needs and demands of the economy, if those needs and demands were expressed with the correct price signals in the free market.Random, isolated entrepreneurial miscalculations and mistaken investments occur in any market (resulting in standard bankruptcies and business failures) but systematic, simultaneous and widespread investment mistakes can only occur through systematically distorted price signals, and these result in depressions or recessions. Austrians believe systemic malinvestments occur because of unnecessary and counterproductive intervention in the free market, distorting price signals and misleading investors and entrepreneurs. For Austrians, prices are an essential information channel through which market participants communicate their demands and cause resources to be allocated to satisfy those demands appropriately. If the government or banks distort, confuse or mislead investors and market participants by not permitting the price mechanism to work appropriately, unsustainable malinvestment will be the inevitable result.”

It’s almost impossible to find better examples of malinvestments than China’s empty cities and the tens of thousands of profitless tech startups that have taken the world by storm over the past several years. Future economics students are going to study those phenomena as case studies in how not to run an economy. Of course, it’s still party time in China and in the startup world for now, so the warnings of skeptics like myself fall on deaf ears. But, inevitably, all of the post-Great Recession stimulus-driven booms are going to violently end, and the GDP growth, jobs, and stock price gains created by them will be reversed.

For the author's full disclosure policy, click here.