Garden Variety Pullback Before More Highs? Looking At All The Data

Welcome to our weekly State of the Markets video where Seth Golden and Wayne Nelson discuss all aspects of the market, from the macro to the micro. Please click the link to review the video. (1hr duration). For expedient reviews, feel free to skip segments of the SOTM by following the Outline below:

- Introduction of this week's focus points for market headwinds and tailwinds, macros and micros.

- FOMC press conference was met with market disapproval as the Powell introduces the characterization of inflation as being "transitory".

- Overbought conditions have persisted over the last 60 days. Deepest SPX pullback YTD has been 2.5% back in mid-March.

- Oil has pulled back with SPX following. The two have been intertwined for a long time and feed off each other. (0-8 minutes in)

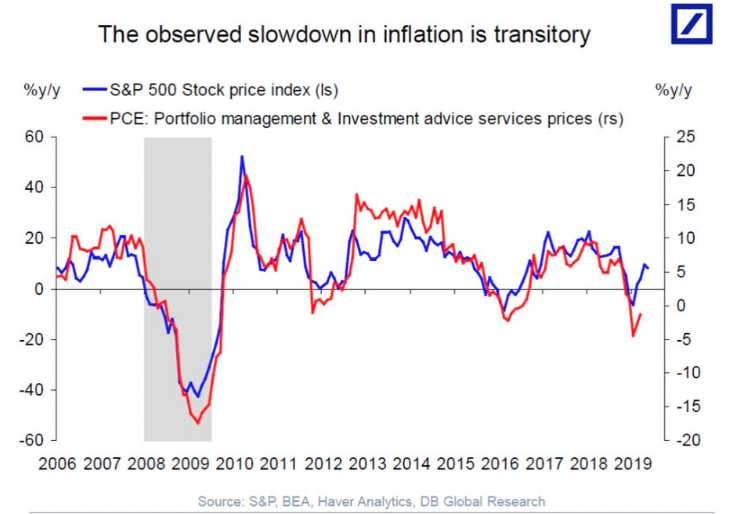

- Inflation paradigm suggests future reflation will have increasingly limited upside potential due to technological advances as well as frequent recessions and market shocks since the turn of the century.

- "Transitory inflation" explained with error and serves to keep the market at bay. Reality is the trend of reflation is ever lower and with diminishing returns. Most people don't fully understand what transitory inflation ISN'T. (8-14 minutes in)

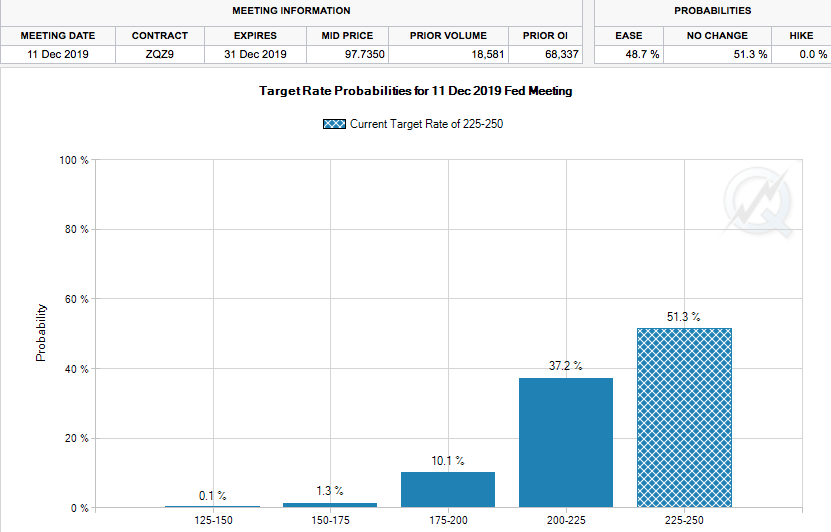

- Fed messaging should guide the markets, but it has proven ineffective under Jerome Powell in effectively guiding markets. Rate cut has been expected by December 2019.

- Rate cut probability has been diminished since FOMC press conference from 65% to 50%.

- China/U.S. trade deal suggested to be in jeopardy by India news source.

- Market downside potential may be limited due to low leverage positioning and FOMO on the heals of positive Q1 EPS and better than expected global GDP data.

- Nonfarm Payroll data due out and expectations have risen. Wage inflation component still in focus. (14-28 minutes in)

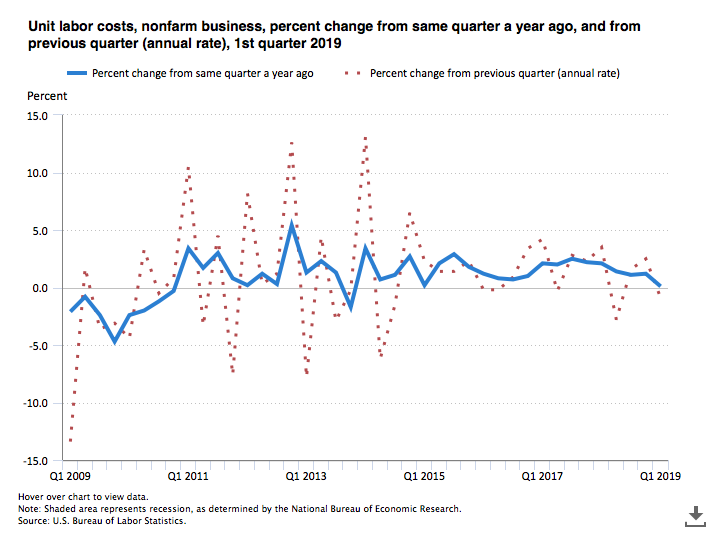

- Wage inflation has been highlighted within Q1 earnings season. But wage pressures are starting to subside.

- Productivity growth has also improved in Q1 as unit labor costs have also come down.

- Income inequality is always present and growing under a capitalistic economy.

- Don't let the market volatility scare you out of the market. Locate professional investors and advisors to help you build your portfolio during a bull market and economic expansion. (28-39 minutes in)

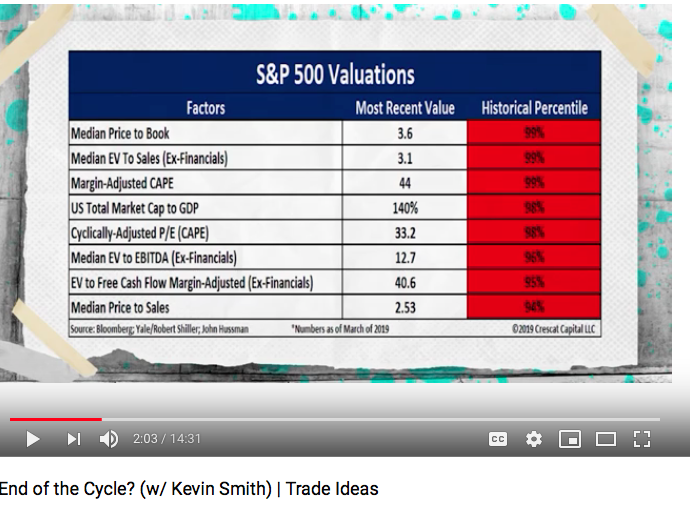

- Kevin Smith calls for the end of bull market cycle. Probabilities are low for a significant market decline, although not completely void.

- Always review both sides of the sentiment and thesis on the market.

- CAPE/Shiller PE ratio accounts for inflation but not retention of earnings per share. Useless and nobody uses CAPE PE ratio for its flaws.

- Bear market narratives seem intelligent, but lack substance when analyzed with market expertise.

- "French bread inflation indicator". (39-51 minutes in)

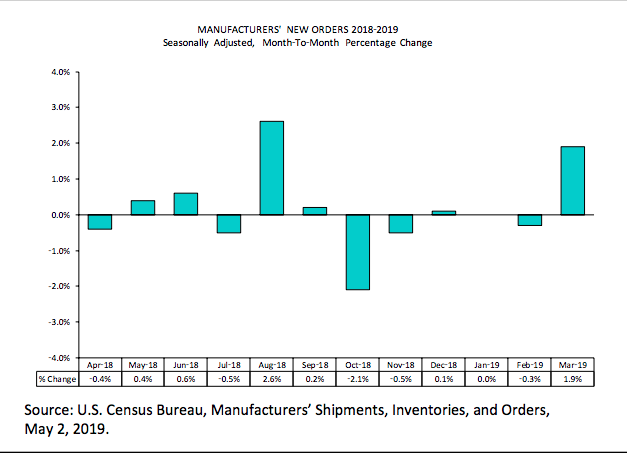

- Discussing some of the latest economic data including latest rise in Factory Orders

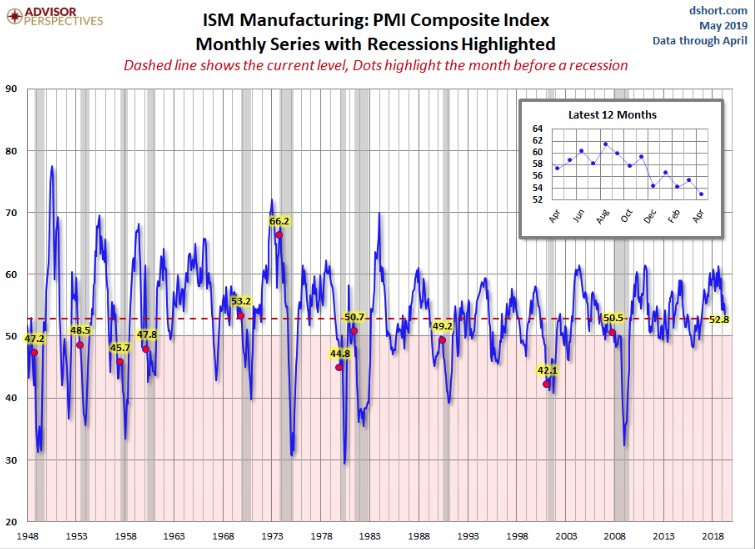

- ISM manufacturing index. Lack of trade deal continues to weigh on business spending inclusive of ordering. Customer inventories are still too low.

- Most Q2 GDP estimates still show growth above 1% to start the cycle.

- ISM prices paid fell from 54 to 50, highlighting the disinflationary environment.

- Doug Short suggests the ISM manufacturing index is somewhat useless and long-term chart validates. (51-56 minutes in)

- Myths and omissions from market bears with respect to the latest quarterly global trade data.

- Factory Orders, Durable Good Orders, global GDP data and Baltic Dry Index defy the global trade data.

How did you like this article? Let us know so we can better customize your reading experience.

Comments

Leave a comment to automatically be entered into

our contest to win a free Echo Show.