FX Positioning: Dollar Longs Rose Into The Fed Meeting

CFTC data shows that dollar longs continued to rise heading into the August FOMC, which supports our view that the dollar’s negative reaction to the meeting may have at least partly been a position-squaring event. The Canadian and New Zealand dollars saw the largest short squeezes in the week ending July 27.

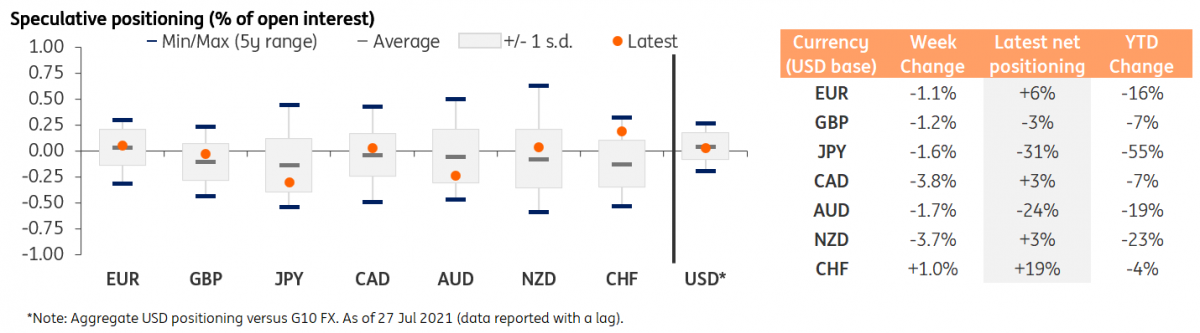

USD: Bullish sentiment on the dollar continued to rise

CFTC data on G10 FX positioning shows that the aggregate dollar positioning continued to rise into net-long territory in the week ending 27 July. The gauge of net-long USD (UUP) positions vs reported G10 currencies (i.e. G9 excluding Norway's krone and Sweden's krona), moved from being worth 1.5% of open interest to 3.0% of open interest in that week, as the dollar’s positioning gained ground against all G10 currencies except for the Swiss franc where speculative positions reported by the CFTC are often detached from spot market dynamics.

Sources: CFTC, Macrobond, ING

This move in the dollar’s positioning is an indication of how markets continued to increase their bullish sentiment on the greenback, thanks to a less supportive risk environment with growing doubts about the global recovery (which prompted an unwinding of reflationary trades) and to the Fed moving closer to normalizing monetary policy. We think that the rise in USD net longs also endorses our view that the drop in the currency after the FOMC rate announcement and Jerome Powell’s press conference on 28 July (so not covered by the data) can at least be partly considered as a position-squaring/profit-taking event, as speculators who had bet on dollar strength backed by Fed tapering expectations may have taken the chance to cash in on their long-dollar positions.

This week – as per our G10 FX Week Ahead preview - we do not expect to see more dollar weakness, as the data-flow in the US should allow markets to cement their hawkish Fed views and the risk environment may struggle to fully recover due to China’s regulatory crackdown and the US retaliation.

CAD and NZD worst hit by rise in USD longs

Two of the currencies that still had a respectable net-long positioning – CAD and NZD - were those that saw the largest short-squeeze in the week ending 27 July. Indeed, their high beta to global risk sentiment also contributed to the drop in positioning. Both CAD and NZD have had a very similar net-positioning (in open interest terms) lately and they have now moved to a neutral positioning, with net-longs only worth 3% of open interest (FXC).

Both currencies are indeed backed by hawkish central banks, although policy adjustments by the Reserve Bank of New Zealand have been more meaningful, as the asset purchase program was terminated in July and we expect a first hike either this month or in October (much will depend on this week’s jobs data in New Zealand). For this reason, we think NZD’s upside potential is higher than CAD’s, although the downside risks for NZD have also risen lately, given the high exposure of the Kiwi economy to China.

Elsewhere in the G10, EUR/USD positioning was at 6% of open interest and only the Swiss franc (FXF) presented a more pronounced overbought condition. As mentioned above, and often reiterated in our FX positioning commentaries, the CHF positioning as reported by the CFTC is often detached from actual market sentiment on the currency and should be taken with a pinch of salt (FXE).

The Japanese yen and Australian dollar remain the biggest shorts in the G10. For the yen, this is a bit surprising considering how US interest rates have continued to edge lower (which normally triggers stronger interest in JPY). For AUD, it is surely less of a surprise, as the currency has recently been caught in the crossfire of unsupportive external risk factors and a domestic central bank that is lagging most of its peers (especially in New Zealand, Canada and Norway) in the policy normalization process (FXY, FXA).

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more