Futures Jump On First Day Of May In Quiet Session

S&P and Nasdaq futures, and European bourses were volatile but ultimately rose on Monday to kick off a new month in a quiet session which saw several major markets closed, following a week of record earnings beat which however resulted in big stock drops with investors also keeping an eye on India COVID cases and economic data to gauge the pace of recovery (SPY, QQQ).

Trading was subdued with several including Japan, China and the U.K. closed for public holidays. S&P 500 futures added 0.6%, Dow e-minis were up 216 points, or 0.64%, and Nasdaq 100 e-minis were up 40.25 points, or 0.30%. Europe’s Stoxx 600 Index gained 0.4%. The yen weakened, while gold advanced.

With more than 60% of companies already having reported mostly stellar results so far, profits are now expected to have risen 46% in the first quarter, compared with forecasts of 24% growth at the start of April, which however has failed to propel stocks to new highs.

Monday's mood reversed from last Friday's surprise selloff as the biggest nasdaq companies reported blowout earnings only to be punished by the market. Some notable premarket movers:

- Megacap FAAMG stocks rose in premarket trading, with Apple, Amazon.com, Alphabet and Microsoft adding between 0.2% and 0.4% after posting largely upbeat results in the prior week (AAPL, AMZN, GOOGL, MSFT).

- Tesla Inc fell 0.9%. Industry sources told Reuters the electric vehicle maker, under scrutiny in China over safety and customer service complaints, is boosting its engagement with mainland regulators and beefing up its government relations team (TSLA).

- Moderna Inc gained 2.4% after the drugmaker said it would supply 34 million doses of its COVID-19 vaccine this year to the global COVAX program (MRNA)

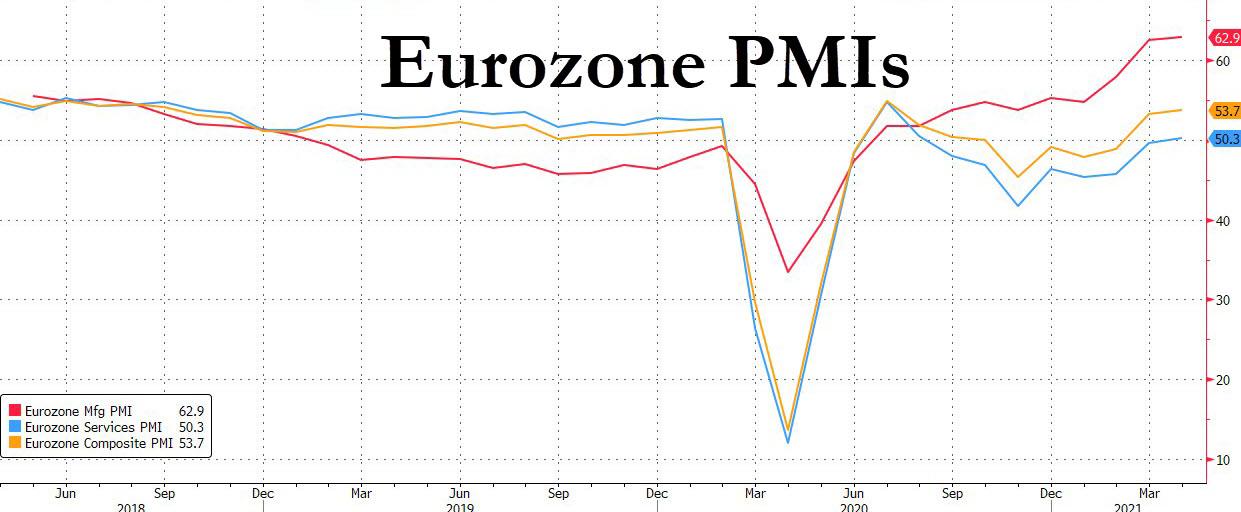

Europe's Stoxx 600 dipped then reversed after euro zone factory activity growth surged to a record high in April, boosted by burgeoning demand and driving a rise in hiring, although supply constraints led to an unprecedented rise in unfulfilled orders, the latest PMI survey showed. IHS Markit’s final Manufacturing Purchasing Managers’ Index (PMI) rose to 62.9 in April from March’s 62.5, albeit below the initial 63.3 “flash” estimate but the highest reading since the survey began in June 1997.

“The euro zone was late out of the gates in terms of its economic rebound but it does seem to be starting. Looking at where we are now the numbers are encouraging,” said Bert Colijn at ING. “It is a foregone conclusion that Q2 will be much stronger than Q1 was.”

Here are some of the biggest European movers today:

- Mediaset rises as much as 3.2% before paring some of the gains. The Italian broadcaster could be near a deal to resolve a legal dispute with Vivendi, Italian media reported over the weekend. Bestinver says that a solution with Vivendi could be a positive catalyst for the stock.

- Straumann shares climb as much as 2.6% to a record after Vontobel (buy) raises PT to CHF1,570 from CHF1,280 following the Swiss dental-implant maker’s “convincing” 1Q sales and given its longer-term prospects.

- KPN shares drop as much as 4.4% after the Dutch telecom carrier, long considered a potential takeover target, said it rejected two separate, unsolicited approaches. A report saying KPN got a EU3/share offer disappointed some investors, while analysts stressed the difficulties for would-be buyers.

- Siemens Gamesa shares fall as much as 6% after full-year sales forecast missed estimates. While the company topped Ebit expectations in 2Q, its 2021 guidance cut was unexpected given good onshore order volumes in first half, Citi says in note.

Earlier in the session, Asian stocks declined for a second day with the MSCI Asia Pacific Index slid 0.6%, heading to a one-month low as a resurgence in COVID-19 infections continued to weigh on sentiment. Stock markets in Japan, China, Thailand and Vietnam were shut for the holidays. The region’s surging coronavirus pandemic cases remains a concern, with the daily death toll in India hitting a record 3,689 on Sunday. Meanwhile, Singapore had its first fatality due to complications from COVID-19 in nearly two months over the weekend. Taiwan semiconductor stocks and Chinese internet companies were the biggest drags on the market. “A worsening pandemic situation in India cast a shadow over the Asia-Pacific markets, as investors assess the risk of reopening delays and stricter border controls,” Margaret Yang, a strategist at DailyFX, wrote in a note. South Korea’s benchmark erased gains and closed 0.7% lower as short selling resumed after a 13-month ban. Taiwan was the worst-hit market on Monday, with its benchmark falling almost 2%. Asian stocks have underperformed global peers for the past six weeks amid a surge in coronavirus cases

“Interest rates going forward will be led more by expectations on the tapering from the Fed rather than by inflation,” Raffaele Bertoni, head of debt capital markets at Gulf Investment Corp., said on Bloomberg Television.

As we reported overnight, billionaire Warren Buffett warned of rising price pressures and a “buying frenzy” spurred by low interest rates in his latest marathon Berkshire annual meeting. On Friday, stocks were spooked after Dallas Fed President Robert Kaplan (who’s not currently a voter on the rate-setting committee) said signs of excessive risk-taking suggest it’s time to consider fewer bond purchases. His remarks contrast with those of Fed Chairman Jerome Powell. These warnings come as all top U.S. financial officials and Powell are downplaying inflation risks.

A busy week for U.S. economic data is expected to show resounding strength, particularly for the ISM manufacturing survey and April payrolls. Forecasts are that 978,000 jobs were created in the month - with whisper numbers as high as 1.5 million - as consumers spent their stimulus money and the economy opened up more. Such gains could stir speculation of a tapering in asset purchases by the Federal Reserve, though Chair Jerome Powell has shown every sign of staying patient on policy.

"Payrolls should show another near 1 million jobs gain, but that would still leave them 7.5 million below pre-COVID levels," said Tapas Strickland, a director of economics at NAB.

"Chair Powell recently noted that it would take a string of months of job creation of about a million a month to achieve the substantial progress required to justify tapering QE."

In FX, the Bloomberg Dollar Spot Index inched lower as most Group-of-10 peers advanced after Friday’s rally in the greenback; the dollar index stood at 91.253 and off a two-month trough of 90.422, though it still ended April with a loss of 2%. The euro was steady at $1.2026 , having backtracked form a nine-week peak of $1.2149 on Friday. It now has solid support around $1.1990 as it shrugs off weaker- than-forecast PMI numbers and 10-year French, Belgian and Austrian yields all rose above last week’s highs as traders unwind haven buying amid thin liquidity; Eurozone April manufacturing PMI 62.9 vs flash reading 63.3. Australia’s dollar bounced from a one-week low a day before an interest rate decision from the central bank and ahead of its quarterly Statement on Monetary Policy later in the week. The front-end of Aussie swaps are fully discounting a rate hike of 15bps by mid-2022, which looks extreme relative to the bank’s latest cash rate guidance, according to Goldman Sachs strategists. The yen slipped to a three-week low against the dollar amid speculation that the Federal Reserve will tighten monetary policy over time while the Bank of Japan retains an easing bias.

In rates, Treasuries opened cheaper at 7am ET amid declines for futures on low volume as overseas cash bond markets were closed. Those losses were pared led by bund futures, leaving U.S. 10-year yields cheaper by ~2bp vs Friday’s close. Treasury yields cheaper by less than 2bp across the curve with front-end outperforming, steepening 2s10s by ~1.5bp; German 10- year yields are cheaper by around 1.5bp vs Friday as month-end demand bid fades. Focus this week is on Wednesday’s Treasury refunding announcement -- where most dealers expect auction sizes to be unchanged from February -- followed by Friday’s April employment report. On the supply side the dollar issuance slate empty; potential $150b of supply is expected for this month as financing remains cheap with spreads near the lowest in three years.

In commodity markets, gold held to a narrow range around $1,768 an ounce sidelined in part by investor interest in crypto currencies as an alternative hedge against inflation. Oil prices ran into profit-taking on Friday but still ended the month with gains of 6% to 8%. Brent was last up 16 cents at $66.92 a barrel, while U.S. crude firmed 18 cents to $63.76 per barrel.

Ethereum hit a record high on Monday trade above $3,000 for the first time, extending last week's rally in the wake of a report that the European Investment Bank (EIB) could launch a digital bond sale on the Ethereum blockchain network (ETH-X).

Powell is due to speak later on Monday and will be followed by a raft of Fed officials this week. Dallas Fed President Robert Kaplan caused a stir on Friday by calling for beginning the conversation about tapering

Market Snapshot

- S&P 500 futures up 0.5% to 4,193.50

- SXXP Index up 0.3% to 438.73

- MXAP down 0.6% to 205.19

- MXAPJ down 0.7% to 691.51

- Nikkei down 0.8% to 28,812.63

- Topix down 0.6% to 1,898.24

- Hang Seng Index down 1.3% to 28,357.54

- Shanghai Composite down 0.8% to 3,446.86

- Sensex down 0.6% to 48,490.19

- Australia S&P/ASX 200 little changed at 7,028.80

- Kospi down 0.7% to 3,127.20

- Brent futures little changed at $66.82/bbl

- Gold spot up 0.4% to $1,776.60

- U.S. Dollar Index little changed at 91.20

- German 10Y yield up 3 bps to -0.17%

- Euro up 0.2% to $1.2042

Disclosure: Copyright ©2009-2021 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies ...

more