Federal Housing Administration In The Reverse-Mortgage Market

from the Congressional Budget Office

Reverse mortgages let households that have at least one member age 62 or older borrow money by using the equity in their home as collateral. The borrowed funds can be used to repay an existing mortgage or to fund other expenses. The federal government plays a large role in supporting the market for reverse mortgages, and policymakers have shown interest in modifying that support - for example, through changes that would reduce costs to the federal government or make reverse mortgages less risky for borrowers.

How Does the Federal Government Support the Reverse-Mortgage Market?

The Federal Housing Administration (FHA) guarantees repayment on qualifying reverse mortgages made by private lenders. Through its Home Equity Conversion Mortgage (HECM) program, FHA has guaranteed more than 1 million reverse mortgages since 1992. (Loans that receive an FHA guarantee through that program are called HECMs, pronounced “heckums.")

Homeowners who take out a HECM are eligible to borrow an amount equal to a given fraction of their home’s current value. They may draw on the available funds - known as the available principal limit - either immediately or over time. FHA, the lender, and the entity administering (servicing) the loan charge the borrower various fees, including a fee intended to compensate FHA for its guarantee. The loan balance (what the borrower owes) increases as interest and fees accrue on the amount outstanding.

A HECM becomes due and payable under a number of circumstances, such as if the borrower (and spouse, if any) dies or moves to a different primary residence. The borrower or the borrower’s estate must then satisfy the loan obligation, either by repaying the outstanding balance or by forfeiting the home. In general, if the funds received from the borrower do not equal the outstanding balance of the HECM, the lender may claim the difference from FHA. By offering lenders a guarantee against losses, the federal government encourages them to issue reverse mortgages more readily than they would otherwise.

What Are the Budgetary Effects of FHA’s Guarantees?

The HECM program affects the federal budget primarily through FHA’s payments to lenders and the fees that FHA charges borrowers. The Congressional Budget Office projects that if current laws generally remained the same, the roughly 39,000 new HECMs that FHA is expected to guarantee in 2020 would produce very small budgetary savings over their lifetime. (That projected lifetime amount is recorded in the budget in the year in which the guarantees are made.) That estimate is based on the accounting procedures specified by the Federal Credit Reform Act of 1990 (FCRA) for federal programs that make or guarantee loans.

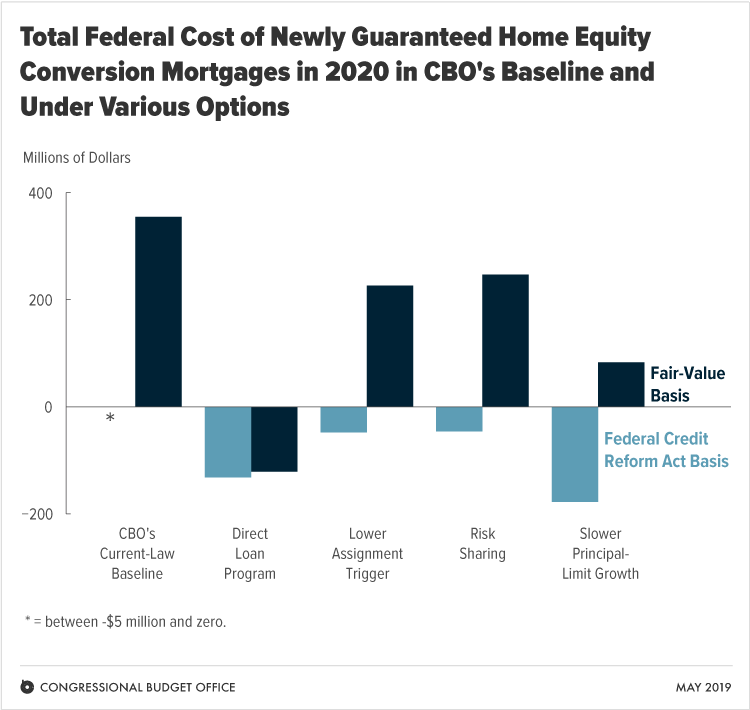

Using fair-value accounting - an alternative method that more fully accounts for the cost of the risk that the government is exposed to when it guarantees loans - CBO projects that the 2020 cohort of new HECMs would instead cost the government about $350 million over their lifetime (see figure).

How Might the Federal Role in the Reverse-Mortgage Market Be Changed?

Policymakers modified the HECM program after the 2008 financial crisis to reduce defaults by borrowers and costs to the federal government, but the program continues to face scrutiny. In particular, policymakers have expressed concern about the risks that the program generates for FHA and borrowers and the potential costs of those risks for the government. CBO analyzed four approaches for altering FHA’s reverse-mortgage guarantees (based on other federal credit programs):

- Converting the HECM program to a direct loan program, in which the government would fund reverse mortgages itself rather than guarantee loans funded by private lenders;

- Reducing the amount of a loan’s outstanding balance that FHA guarantees to repay lenders by requiring lenders to sell (or “assign") an active HECM to FHA earlier than they generally do under current policies (specifically, reducing the loan balance that triggers the option for lenders to assign HECMs);

- Sharing the risk of losses with lenders by requiring them to hold on to an active HECM much longer than they typically do now before assigning it to FHA; and

- Slowing the growth of the funds available to a borrower who does not draw the full amount of a HECM initially.

The number of HECMs guaranteed and the amount of budgetary savings or costs under each option would depend on several factors, including the ways in which FHA, lenders, and borrowers responded to the changes. Under the first three options, lenders would increase fees to borrowers or reduce the availability of HECMs, CBO estimates. (In the direct loan program, private lenders would continue to originate HECMs and charge borrowers closing costs.) Under the fourth option, lenders would be largely unaffected, CBO forecasts, but borrowers would either draw more of their available funds immediately or forgo a HECM in favor of other ways to tap into the equity in their home (such as through a refinancing loan or a home equity line of credit).

Measured on a FCRA basis, the fourth option would have the largest budgetary effect under the parameters that CBO analyzed. Under that approach to slowing the growth of the borrower’s available principal limit, the new HECMs projected to be guaranteed in 2020 would save the federal government $180 million over their lifetime, CBO estimates, compared with the negligible savings projected in CBO’s current-law baseline. The savings from the 2020 cohort of HECMs would be smaller under the other options on a FCRA basis: $130 million under a program of direct loans, or about $50 million if the risk of losses was shared with lenders or if the trigger for assigning reverse mortgages to FHA was reduced.

Measured on a fair-value basis, by contrast, the option to create a direct loan program would have the biggest budgetary impact of the four approaches that CBO examined. Under the direct loan program, the new HECMs projected to be guaranteed in 2020 would save the government about $120 million over their lifetime on a fair-value basis, CBO estimates, rather than cost $350 million as under current policy. Under the other three options, the 2020 cohort of HECMs would still generate costs on a fair-value basis, but the costs would be smaller than under current policy: $250 million if FHA shared the risk of losses with lenders, $230 million if the assignment trigger was reduced, and $80 million if the borrower’s available principal limit grew more slowly than it does now.

Data and Supplemental Information

Related Publications

-

Convert the Home Equity Conversion Mortgage Program Into a Direct Loan Program

December 13, 2018

-

How CBO Produces Fair-Value Estimates of the Cost of Federal Credit Programs: A Primer

July 12, 2018

-

Fair-Value Estimates of the Cost of Federal Credit Programs in 2019

June 29, 2018

-

Options to Manage FHA’s Exposure to Risk From Guaranteeing Single-Family Mortgages

September 28, 2017

Disclaimer: No content is to be construed as investment advise and all content is provided for informational purposes only.The reader is solely responsible for determining whether any investment, ...

more