Economic Theories & Debt Driven Realities

One of the most highly debated topics over the past few months has been the rise of Modern Monetary Theory (MMT). The economic theory has been around for quite some time but was shoved into prominence recently by Congressional Representative Alexandria Ocasio-Cortez’s “New Green Deal” which is heavily dependent on massive levels of Government funding.

There is much debate on both sides of the argument but, as is the case with all economic theories, supporters tend to latch onto the ideas they like, ignore the parts they don’t, and aggressively attack those who disagree with them. However, what we should all want is a robust set of fiscal and monetary policies which drive long-term economic prosperity for all.

Here is the problem with all economic theories – they sound great in theory, but in practice, it has been a vastly different outcome. For example, when it comes to deficits, John Maynard Keynes contended that:

“A general glut would occur when aggregate demand for goods was insufficient, leading to an economic downturn resulting in losses of potential output due to unnecessarily high unemployment, which results from the defensive (or reactive) decisions of the producers.”

In other words, when there is a lack of demand from consumers due to high unemployment, then the contraction in demand would force producers to take defensive actions to reduce output. Such a confluence of actions would lead to a recession.

In such a situation, Keynesian economics states that government policies could be used to increase aggregate demand, thus increasing economic activity and reducing unemployment and deflation. Investment by government injects income, which results in more spending in the general economy, which in turn stimulates more production and investment involving still more income and spending and so forth. The initial stimulation starts a cascade of events, whose total increase in economic activity is a multiple of the original investment.

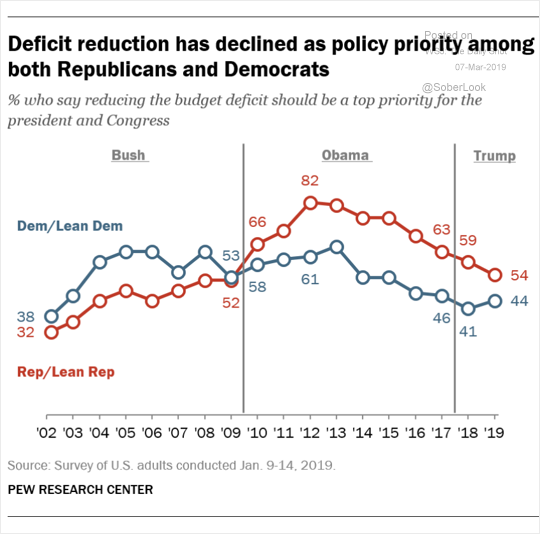

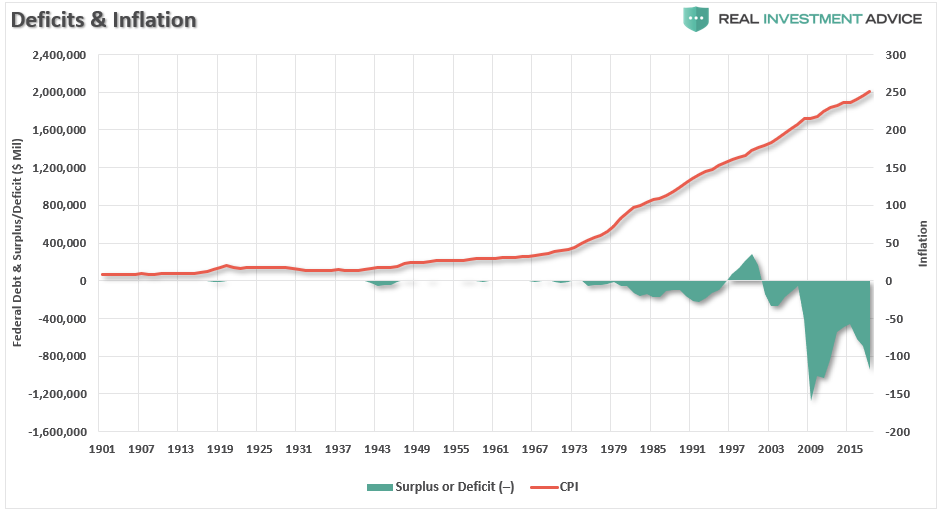

Unfortunately, as shown below, economists, politicians, and the Federal Reserve have simply ignored the other part of the theory which states that when economic activity returns to normal, the Government should return to a surplus. Instead, the general thesis has been:

“If a little deficit is good, a bigger one should be better.”

As shown, politicians have given up be concerned with deficit reduction in exchange for the ability to spend without constraint.

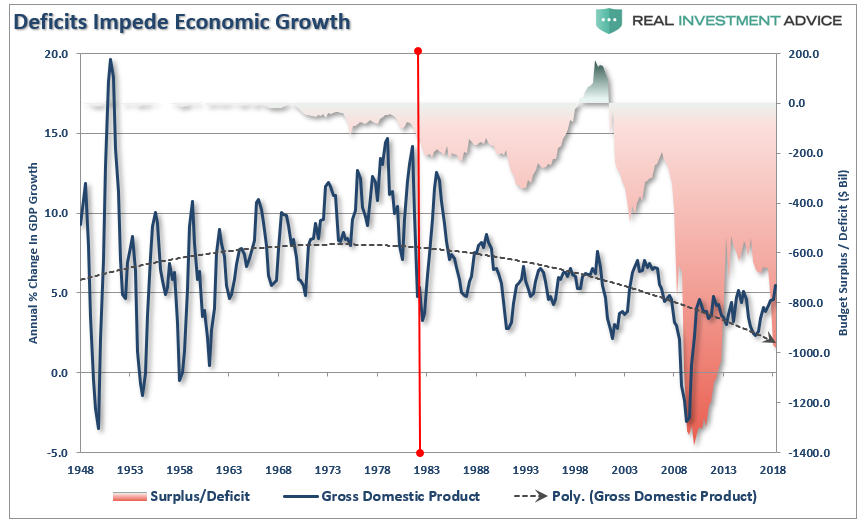

However, as shown below, the theory of continued deficit spending has failed to produce a rising trend of economic growth.

When it comes to MMT, once again we see supporters grasping onto the aspects of the theory they like and ignoring the rest. The part they “like” sounds a whole lot like a “Turbotax” commercial:

The part they don’t like is:

“The only constraint on MMT is inflation.”

That constraint would come as, the theory purports, full employment causes inflationary pressures to rise. Obviously, at that point, the government could/would reduce its support as the economy would theoretically be self-sustaining.

However, as we questioned previously, the biggest issue is HOW EXACTLY do we measure inflation?

This is important because IF inflation is the ONLY constraint on debt issuance and deficits, then an accurate measure of inflation, by extension, is THE MOST critical requirement of the theory.

In other words:

“Where is the point where the policy must be reversed BEFORE you cause serious, and potentially irreversible, negative economic consequences?”

This is the part supporters dislike as it imposes a “limit” on spending whereas the idea of unconstrained debt issuance is far more attractive.

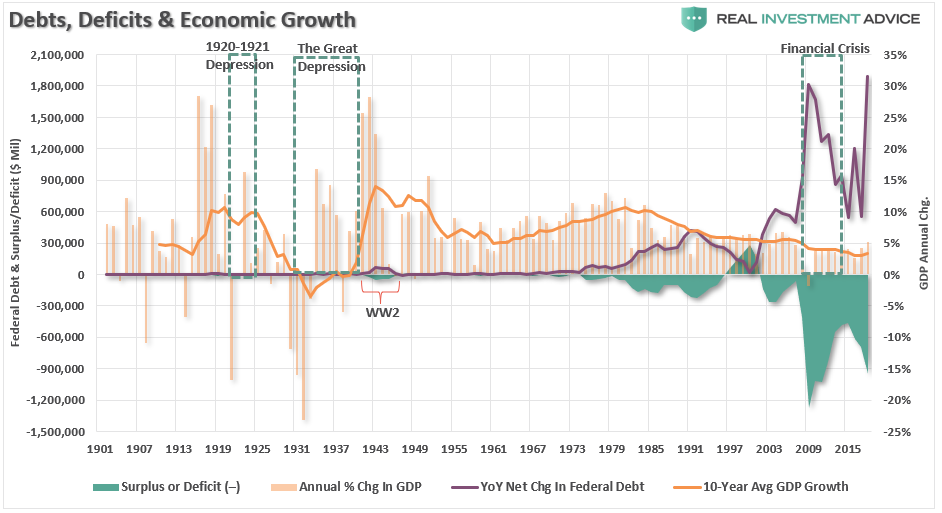

Again, there is no evidence that increasing debts or deficits, inflation or not, leads to stronger economic growth.

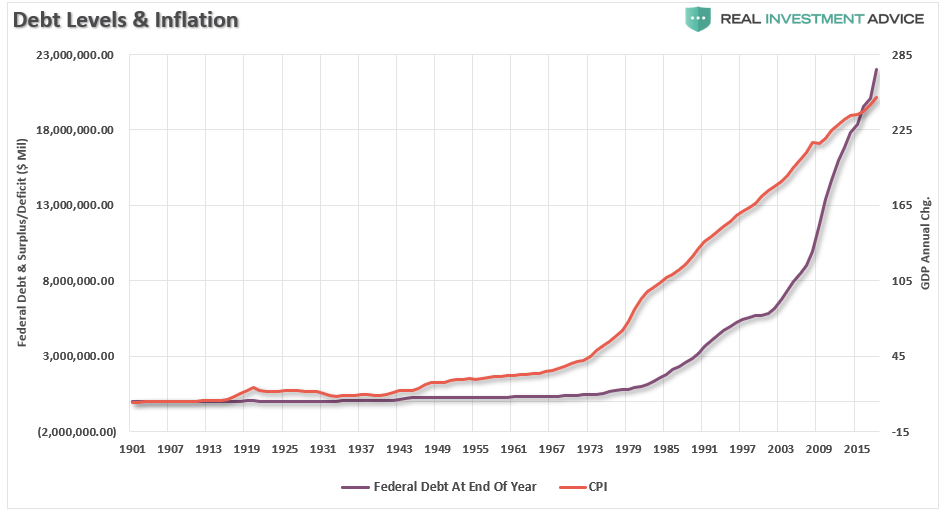

However, there is plenty of evidence which shows that rising debts and deficits lead to price inflation. (The chart below uses the consumer price index (CPI) which has been repeatedly manipulated and adjusted since the late 90’s to suppress the real rate of inflationary pressures in the economy. The actual rate of inflation adjusted for a basket of goods on an annual basis is significantly higher.)

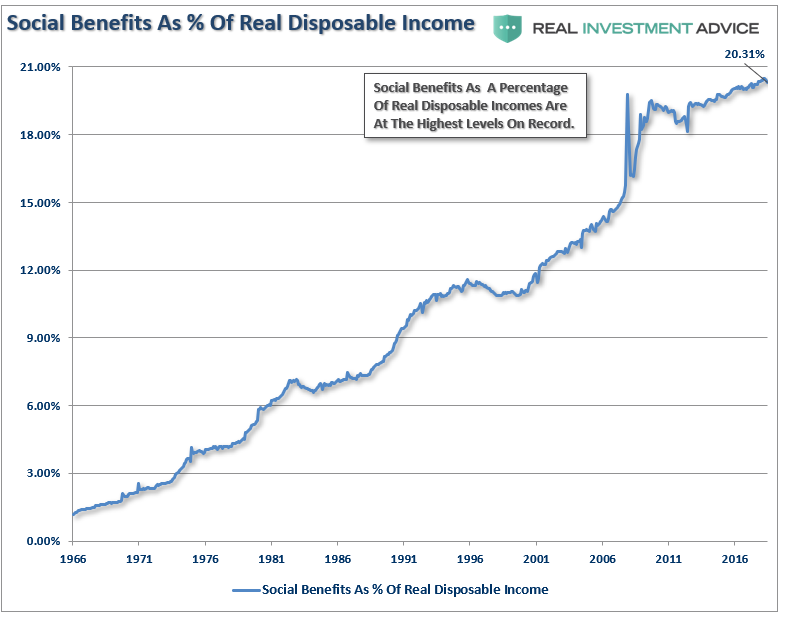

Of course, given the Government has already been running a “quasi-MMT” program for the last 30-years, the real impact has been a continued shift of dependency on the Government anyway. Currently, one-in-four households in the U.S. have some dependency on government subsidies with social benefits as a percentage of real disposable income at record highs.

If $22 trillion in debt, and a deficit approaching $1 trillion, can cause a 20% dependency on government support, just imagine the dependency that could be created at $40 trillion?

If the goal of economic policy is to create stronger rates of economic growth, then any policy which uses debt to solve a debt problem is most likely NOT the right answer.

This is why proponents of Austrian economics suggest trying something different – less debt. Austrian economics suggests that a sustained period of low-interest rates and excessive credit creation results in a volatile and unstable imbalance between saving and investment. In other words, low-interest rates tend to stimulate borrowing from the banking system which in turn leads, as one would expect, to the expansion of credit. This expansion of credit then creates an expansion of the supply of money.

Therefore, as one would ultimately expect, the credit-sourced boom becomes unsustainable as artificially stimulated borrowing seeks out diminishing investment opportunities. Finally, the credit-sourced boom results in widespread malinvestments. When the exponential credit creation can no longer be sustained a “credit contraction” occurs which ultimately shrinks the money supply and the markets finally “clear” which causes resources to be reallocated back towards more efficient uses.

Time To Wake Up

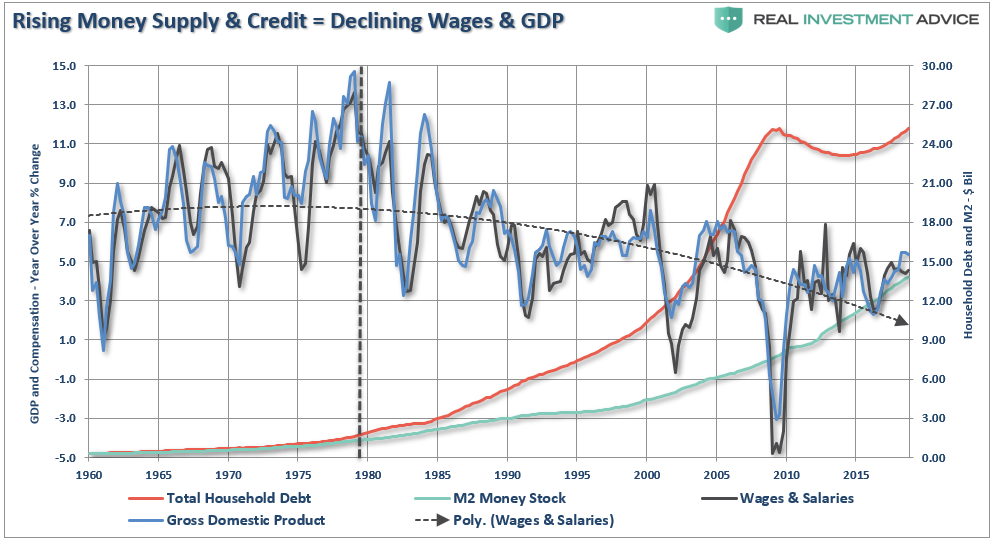

For the last 30 years, each Administration, along with the Federal Reserve, have continued to operate under Keynesian monetary and fiscal policies believing the model worked. The reality, however, has been most of the aggregate growth in the economy has been financed by deficit spending, credit expansion and a reduction in savings. In turn, the reduction of productive investment into the economy has led to slowing output. As the economy slowed and wages fell the consumer was forced to take on more leverage which also decreased savings. As a result of the increased leverage, more of their income was needed to service the debt.

Secondly, most of the government spending programs redistribute income from workers to the unemployed. This, Keynesians argue, increases the welfare of many hurt by the recession. What their models ignore, however, is the reduced productivity that follows a shift of resources toward redistribution and away from productive investment.

In its essential framework, MMT suggests correctly that debts and deficits don’t matter as long as the money being borrowed and spent is used for productive purposes. Such means that the investments being made create a return greater than the carrying cost of the debt used to finance the projects.

Again, this is where MMT supporters go astray. Free healthcare, education, childcare, living wages, etc., are NOT productive investments which have a return greater than the carrying cost of the debt. In actuality, history suggests these welfare supports have a negative multiplier effect in the economy.

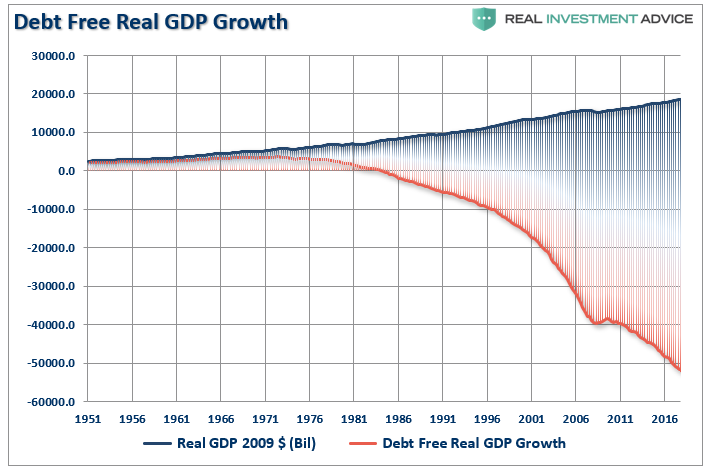

What is most telling is the inability for the current economists, who maintain our monetary and fiscal policies, to realize the problem of trying to “cure a debt problem with more debt.”

This is why the policies that have been enacted previously have all failed, be it “cash for clunkers” to “Quantitative Easing”, because each intervention either dragged future consumption forward or stimulated asset markets. Dragging future consumption forward leaves a “void” in the future which must be continually filled, This is why creating an artificial wealth effect decreases savings which could, and should have been, used for productive investment.

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the end result, has been clearly wrong. It hasn’t happened in 30 years.

MMT supporters have the same view that if the government hands out money it will create stronger economic growth. There is not evidence which supports such is actually the case.

It’s time for those driving both monetary and fiscal policy to wake up. The current path we are is unsustainable. The remedies being applied today is akin to using aspirin to treat cancer. Sure, it may make you feel better for the moment, but it isn’t curing the problem.

Unfortunately, the actions being taken today have been repeated throughout history as those elected into office are more concerned about “satiating the mob with bread and games” rather than suffering the short-term pain for the long-term survivability of the empire. In the end, every empire throughout history fell to its knees under the weight of debt and the debasement of their currency.

It’s time we wake up and realize that we too are on the same path.