Don't Ignore The Yield Curve

Over the past few days, there’s been lots of chatter about the recent flattening of the yield curve. The rising of short term yields with the opposite move at the longer-end has caused the 2 and 5-year portion of the curve to invert. With any inversion, suddenly everyone is a bond trader and has an opinion about what it means for risk assets and the world in general. Of course, the MacroTourist is no exception, but before I throw my opinion into the sea of sound bites, let’s examine how we got here.

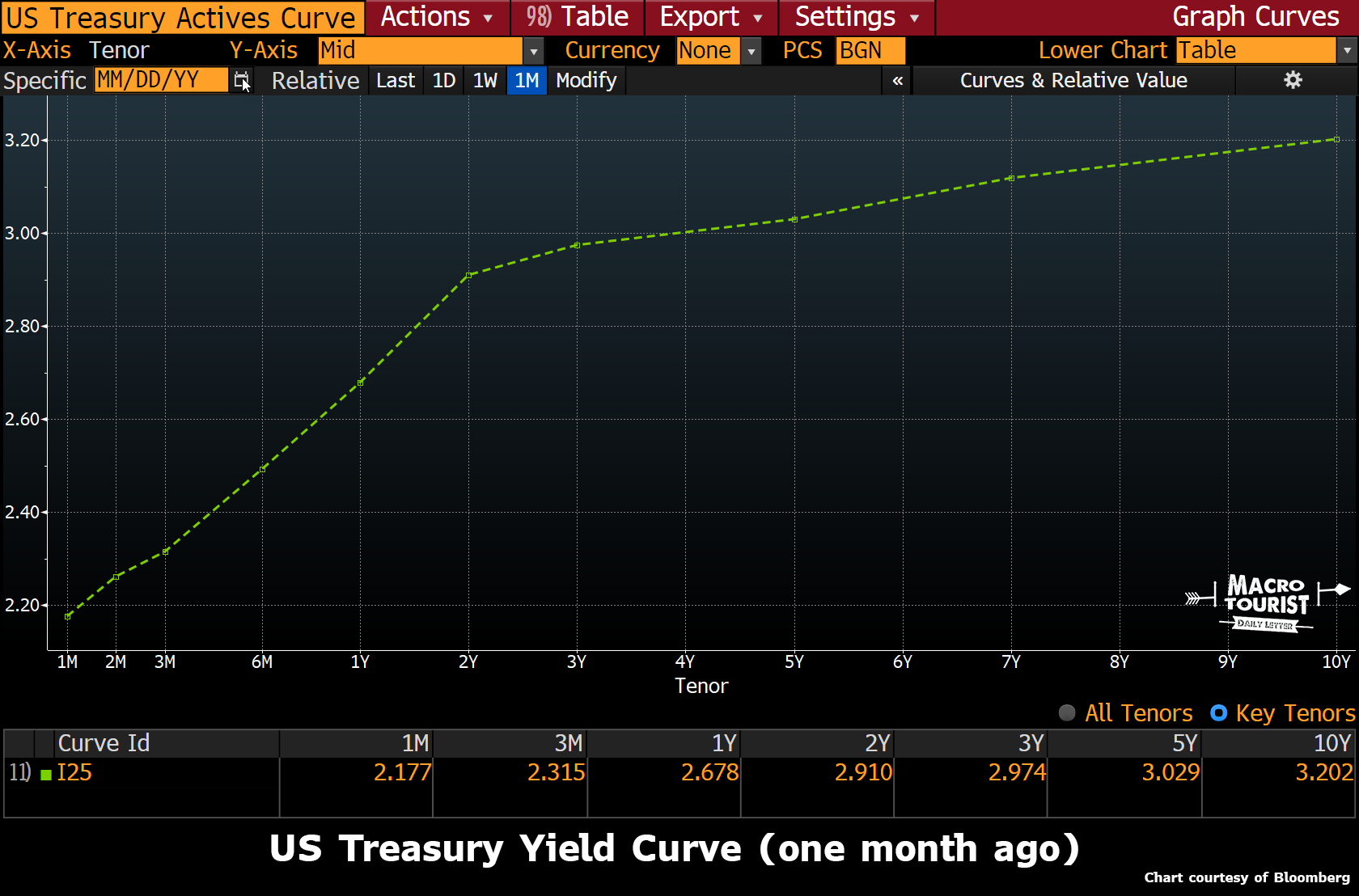

Let’s start with the yield curve one month ago.

I am using the active U.S. Treasury yield curve, but they all look roughly the same. As you will notice, back then it was a nice upward sloping yield curve. Every tenor had a higher yield than the previous shorter dated maturity.

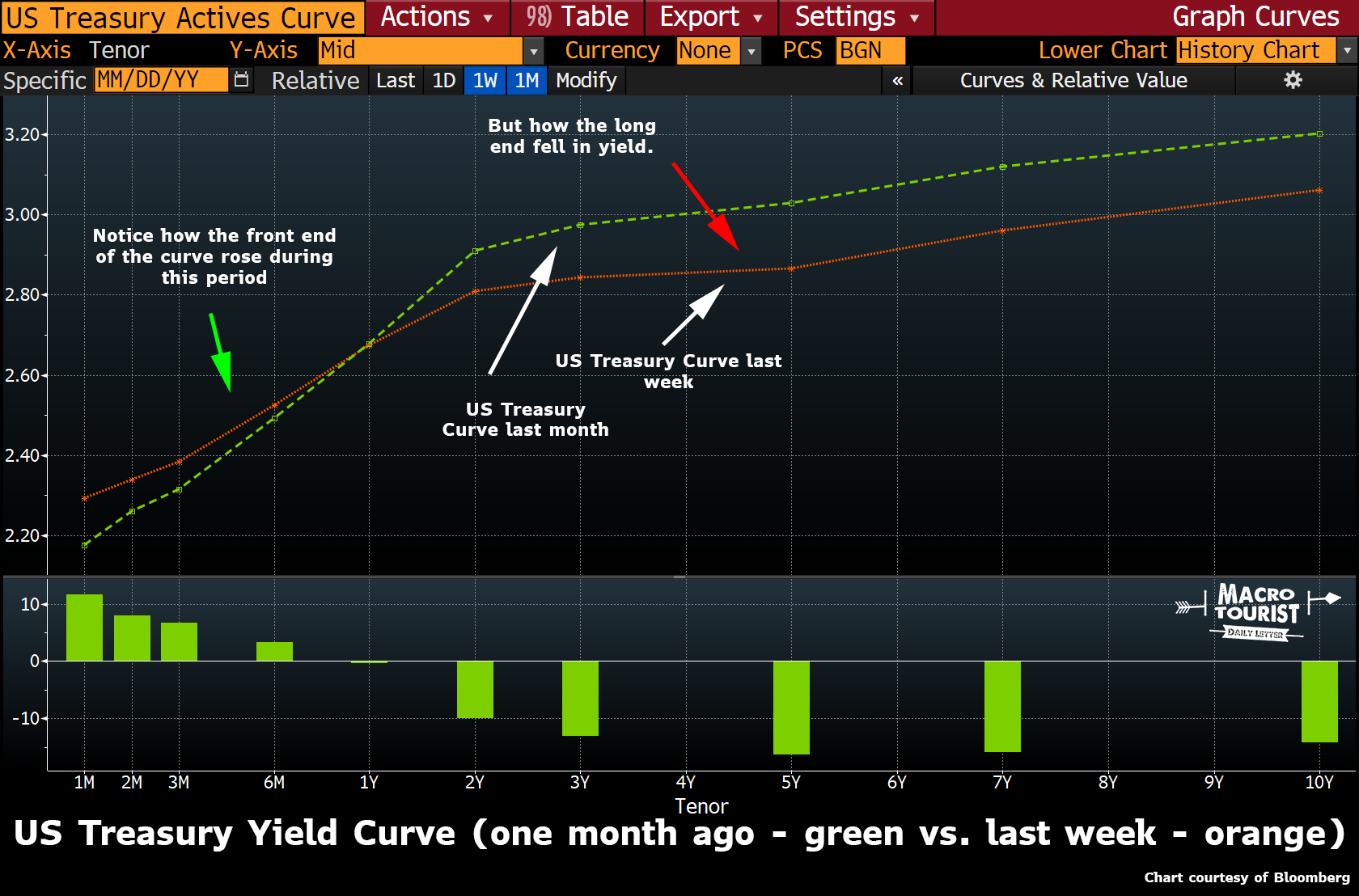

But then last week, Federal Reserve Chairman Powell gave his speech where he “blinked” and took a more dovish stance.

What happened to the yield curve? Well, versus a month ago, the front end of the curve ended higher, while the long end fell in yield.

This was a flattening of the yield curve. Yet notice how still every longer maturity had a higher yield. At this point last week, the curve was still upwardly sloped.

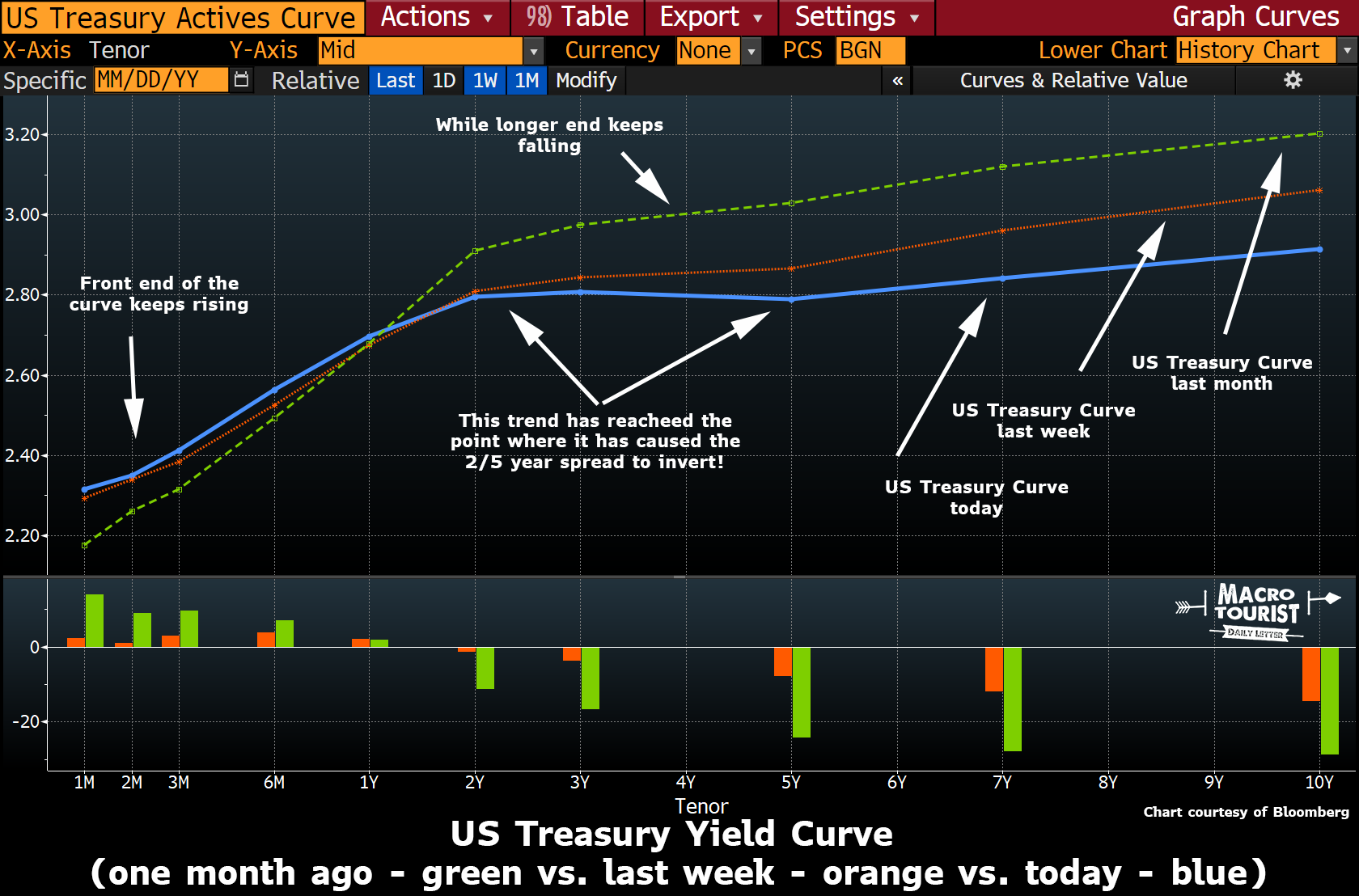

Yet we can’t say the same today (actually, I am late publishing this piece, so the data is from yesterday - December 5th, 2018)

Look at the yield curve. The front end has risen while the long end has kept falling. This has caused the 2⁄5-year spread to invert (meaning the 2-year yield is higher than the 5-year yield).

Here is a chart of the difference between the 2 and 5-year yield:

It’s that ticking below the red line that has gotten all the financial news pundits lathered up into a frenzy.

But what does that really mean?

Well, an inversion of the yield curve has traditionally been one of the best indicators presaging a recession. There has been tons of studies and even more conclusions drawn from the data, so you probably don’t need me to rehash them all.

Yet I think it’s amusing to hear all the yield-curve-apologists (a term coined by my colorful pal, Janney’s Guy LeBas in this article) once again claiming that yield curve inversions don’t matter.

Whether it’s the fact that we need to wait for the 3-month / 5-year to invert, or whether it is the long lead time between the 2-10-year spread inverting and the actual recession, there are plenty of excuses being offered up about why the yield curve inversion doesn’t matter.

Yeah, let me get this straight. The largest, most liquid market in the world is sending a signal that has consistently been one of the most reliable indicators that a recession is near and somehow it makes sense to fade it?

As a trader who cut his eye-teeth in the equity market, I can tell you unequivocally, bond traders are smarter. They just are. Denying it is like trying to argue that people in Malibu are no better looking than any other big U.S. suburb.

So when the yield curve starts inverting, you better believe I am paying attention.

However, as usual, there is a catch. Market cycles are similar, but never exactly the same.

In the post-GFC era we will not see the same degree of yield curve inversion that we have in past cycles. There is simply too much debt out there. The global economy cannot handle the same amount of tightening as in past cycles.

I know the crowd who believes that “Powell is different than all the other Fed Chairs” will cry out in anguish at this proclamation, but last week’s dovish shift shows his stomach to handle any sort of market disruption is way lower than previously believed. Powell will be no different than all the other Fed Chairs. At the end of the day, he will be loose.

Yet I acknowledge one aspect that is different. Powell hung in there with the tightening bias way longer than I would have guessed. And in doing so, he did what Central Banks always do - he tightened until he broke something.

Don’t believe me?

I would like to highlight a comment he made on October 3rd of this year with PBS’ Judy Woodruff:

“The really extremely accommodative low interest rates that we needed when the economy was quite weak, we don’t need those anymore. They’re not appropriate anymore,” Powell said.

“Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral,” he added. “We may go past neutral, but we’re a long way from neutral at this point.”

A long way from neutral. October 3rd. When the market heard that comment, traders throughout the globe interpreted it to mean that Powell would continue with his hawkish policies regardless of what it meant for the markets.

But the really interesting part? Powell’s comments ushered in the correction he was looking for.

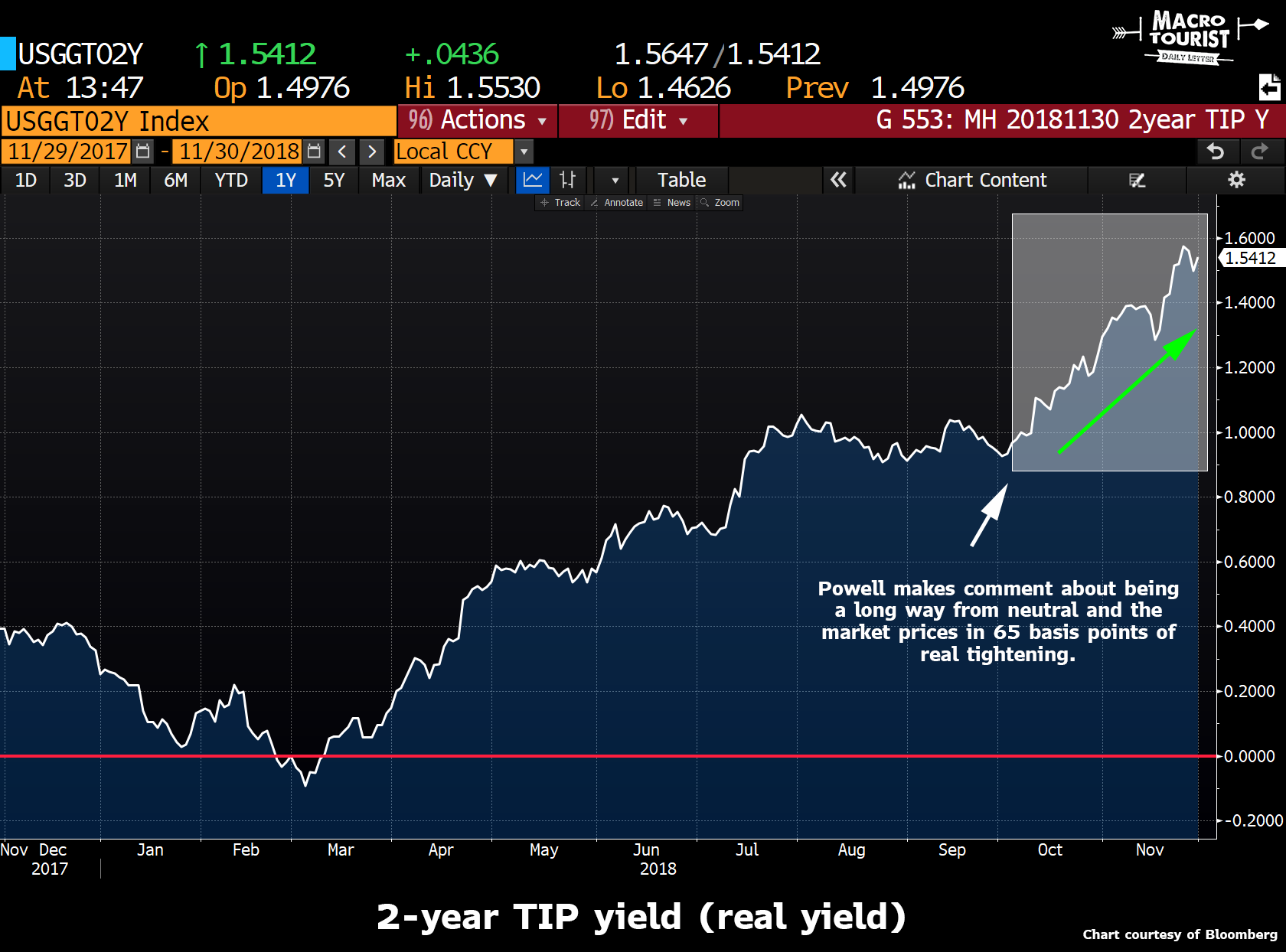

Let’s go through some charts. (I am sorry the charts are from last week, but I made them up for my appearance on MacroVoice’s Patrick Ceresna’s new podcast - The Market Huddle):

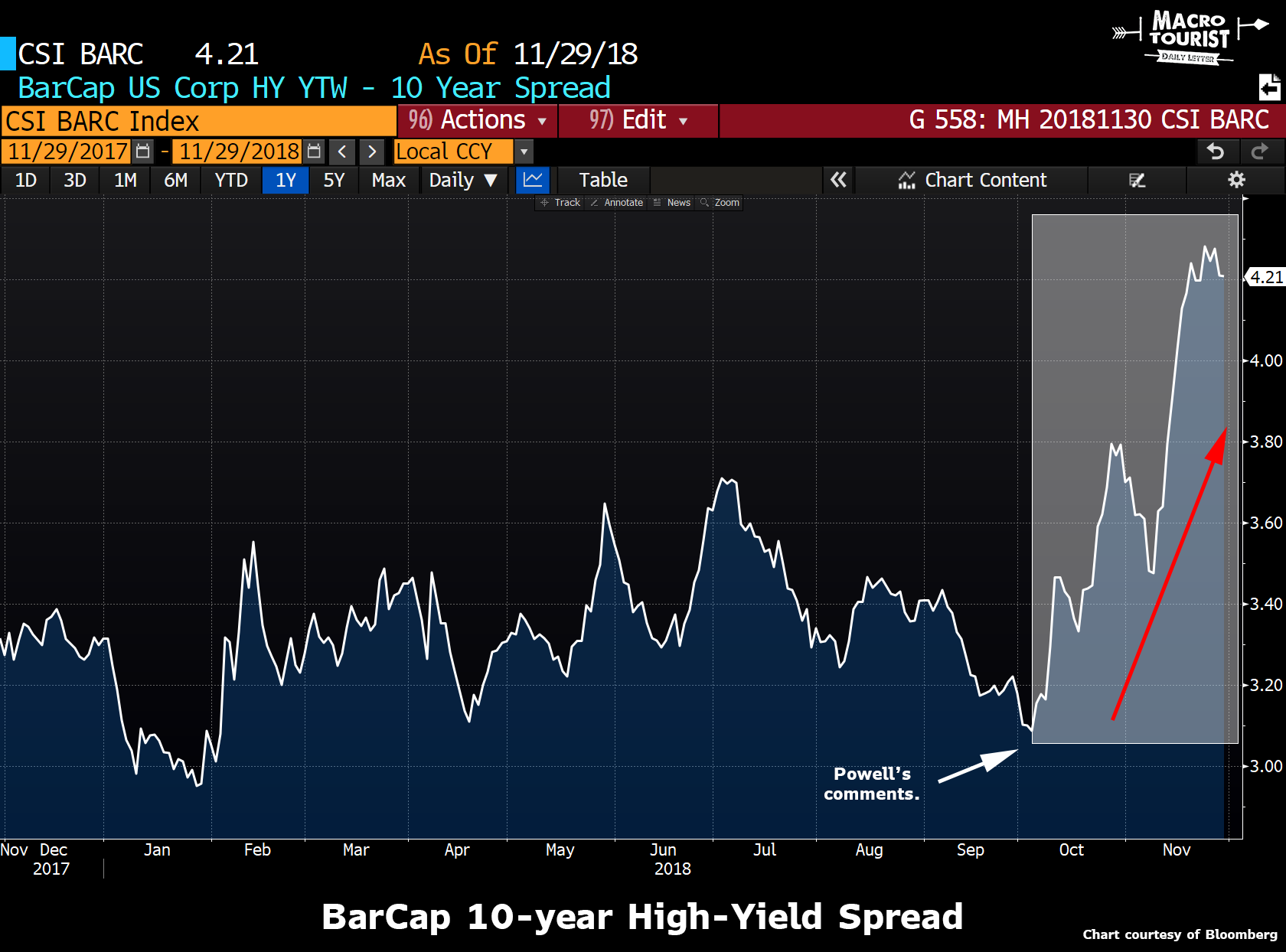

Notice how real yields took off after Powell’s comments.

This caused credit spreads to widen and tighten financial conditions.

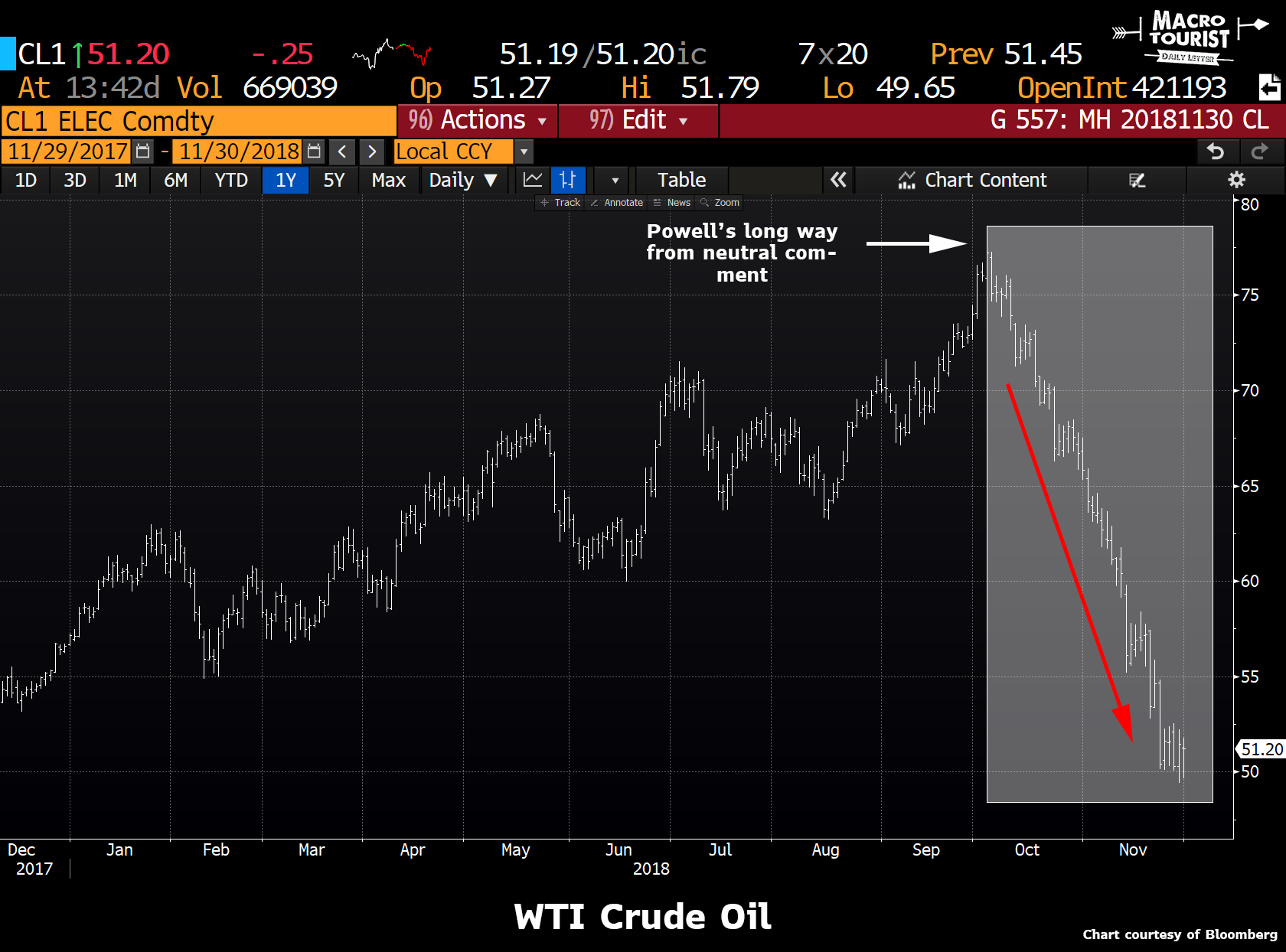

And it wasn’t limited to financial markets. Guess what day crude oil topped?

Yup. October 3rd. Powell’s hawkish comments pushed a lot of markets over the edge.

And the most obvious one? How did the S&P 500 fare?

Again, Powell’s comments ushered in the correction.

The Fed finally broke something

I always said this Fed Chairman would keep tightening until he broke something. Powell’s overly aggressive comments did exactly that, and it’s no surprise that two months later, he said the following:

“Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy - that is, neither speeding up nor slowing down growth.”

What changed in the space of two months for Powell to go from “we’re a long way from neutral” to “rates are just below…neutral”?

It’s quite obvious. I have just sketched it out in those four charts.

But back to the yield curve. The inversion is not that surprising given the late-cycle-nature of the expansion combined with the Fed’s aggressive comments.

Yet isn’t one of the MacroTourist’s main beliefs that the yield curve will steepen? Yes, but here is when stick-handling through the crowd might get a little more difficult, but we have the help of the famous macro strategist, David Rosenberg to help us. I heard David interviewed on Meb Faber’s terrific podcast - The Meb Faber Show where he said the following:

“The risks to the economy is not that the Fed is going to raise rates too quickly, it’s that when it comes time for easing, they will be way too slow.”

Now I might have previously disagreed with him about that first statement, but it’s clear that last week Powell shifted and will no longer keep tightening regardless of economic conditions. The real question is whether the Fed has already gone too far. As Rosie continues:

”…that’s what happened in 2000-2001. That’s what happened in 2007-2008. The Fed was slow to react [by cutting rates]”

David’s comments got me to realize that he is spot-on correct. At the beginning of economic expansions, the Fed is too slow to raise rates but equally too slow to lower them at the end of the economic cycle.

If the economy has rolled over (it has), then the front-end of the yield curve will stay too high because of the Fed’s unwillingness to react with cuts.

Therefore the front couple of years is probably pinned at current levels. After this December rate hike, the Fed will pause and most likely stay there for a while. So when it comes to yield-curve-spread-trading, it makes little sense to be long anything shorter than 2 years.

Which is why the 2-5-year spread has inverted.

End result? Don’t play the 2-10-year-spread steepener. Buy the 5-30-year steepener instead.

But regardless, don’t underestimate the power of the bond market to predict the next economic slowdown. Those bond traders are way smarter than the rest of us. It’s sad, but it’s true.

Disclosure: None.