Dimon’s Detached View Of Economic Realities

In December of 2019, I wrote about Dimon’s delusional view of economic realities. To wit:

“The consumer, which is 70% of the U.S. economy, is quite strong. Confidence is very high. Their balance sheets are in great shape. And you see that the strength of the American consumer is driving the American economy and the global economy. And while business slowed down, my current view is that, no, it just was a slowdown, not a petering out.” – Jamie Dimon

That’s what the head of JP Morgan Chase told viewers in his “60-Minutes” interview.

Then the 2020 recession set in, consumption collapsed, and the Government passed massive stimulus bills to support the 50-million unemployed.

Such isn’t the first time that I have discussed Dimon’s distorted views. Just as we discussed then, even just marginally scratching the surface on the economy and the “household balance sheet” reveals an uglier truth.

In his latest annual shareholder letter, he recently made his usual bombastic and still delusional statements.

Economic Boom Into 2023

“I have little doubt that with excess savings, new stimulus, huge deficit spending, more QE, a new potential infrastructure bill, a successful vaccine, and euphoria around the end of the pandemic, the U.S. economy will likely boom. This boom could easily run into 2023 because all the spending could extend well into 2023.” – Jamie Dimon

There are many problems with his view looking forward.

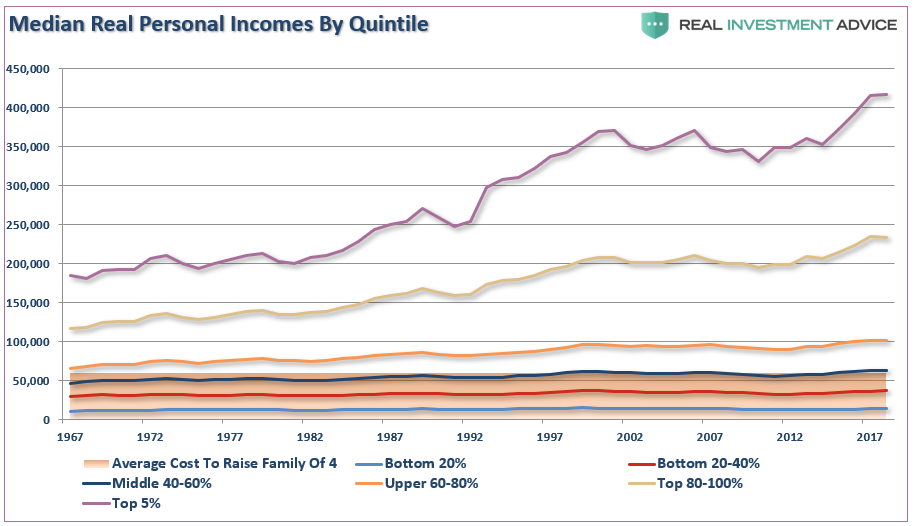

To begin with, the vast majority of American’s do not have excess savings. If they did, then repeated stimulus payments wouldn’t be needed to support economic growth. The reality is “savings” get skewed by the top 20% of income earners, notably the 0.01% like Jamie Dimon.

The top 5%, of income earners skew the measure. Those in the top 20% have seen substantially larger median wage growth versus the bottom 80%. (Note: all data used below is from the Census Bureau and the IRS.)”

Since the top income earners have more than enough income to maintain their living standards, the balance falls into savings. This disparity in incomes generates the “skew” to the savings rate and obfuscates the ability to “maintain a certain standard of living.”

More Stimulus Not The Answer

Such remains problematic for many Americans and consistently forces them further into debt.

“The debt surge is partly by design. A byproduct of low borrowing costs the Federal Reserve engineered after the financial crisis to get the economy moving. It has reshaped both borrowers and lenders. Consumers increasingly need it. Companies increasingly can’t sell their goods without it. And the economy, which counts on consumer spending for more than two-thirds of GDP, would struggle without a plentiful supply of credit.” – WSJ

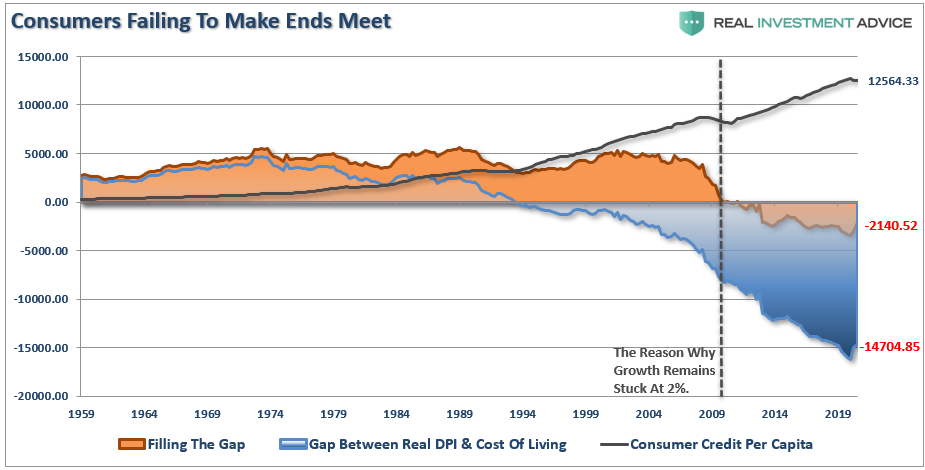

I often show the “gap” between the “standard of living” and real disposable incomes. In 1990, incomes alone were no longer able to meet the standard of living. Therefore, consumers turned to debt to fill the “gap.”

Currently, there is almost a $2150 annual deficit facing the average American. (Note: this deficit accrues every year, which is why consumer credit keeps hitting new records.)

Notably, more “stimulus” has two very negative consequences economically:

- It pulls forward future consumption leaving a future void to fill (presumably with more stimulus); and,

- Stimulus reduces productive economic activity, which retards future growth.

With still high levels of mortgages in forbearance, the need for continuing “eviction moratoriums,” and the ongoing demand for “government largesse” suggest the consumer is not nearly as strong as deemed.

Wasted Deficit Spending

“We need to properly invest, on an ongoing basis, in modernizing infrastructure. Spent wisely, it is an opportunity for everyone.”

Mr. Dimon is correct. Proper spending on infrastructure could indeed be economically beneficial. However, even a cursory glance at previous expenditures, shows such is not the case. Out of the entirety of Biden’s proposed infrastructure plan, only roughly 6% goes to building roads and bridges. Another 2% goes to waterways and dams. The other 92% is a Democratic grab bag of liberal projects, most of which have a negative long-term investment return.

As such, the infrastructure bill is a negative long-term impact on economic growth. Such was a point we discussed previously in “One Way Trip:”

“The chart below shows the deficit, 10-year average GDP growth, and the annual change in Federal Debt. The problem should be obvious. Since the Federal government began ramping up debt, and running deficits, growth continues to deteriorate. Such is not a coincidence.”

With the government already running a massive deficit and adding another $4.25 trillion to date, the negative impact of debt on economic growth will increase.

Recent Wharton School analysis confirmed the same:

- The spending provisions of the AJP, in the absence of any tax increases, would increase government debt by 4.72% and decrease GDP by 0.33% in 2050, as the crowding out of investment due to more significant government deficits outweighs productivity boosts from the new public investments.

- The tax provisions proposed in the AJP, in the absence of any new spending, would decrease government debt by 11.16 percent in 2050. Despite reducing public debt, the AJP’s tax provisions discourage business investment and thus reduce GDP by 0.49 percent in 2050.

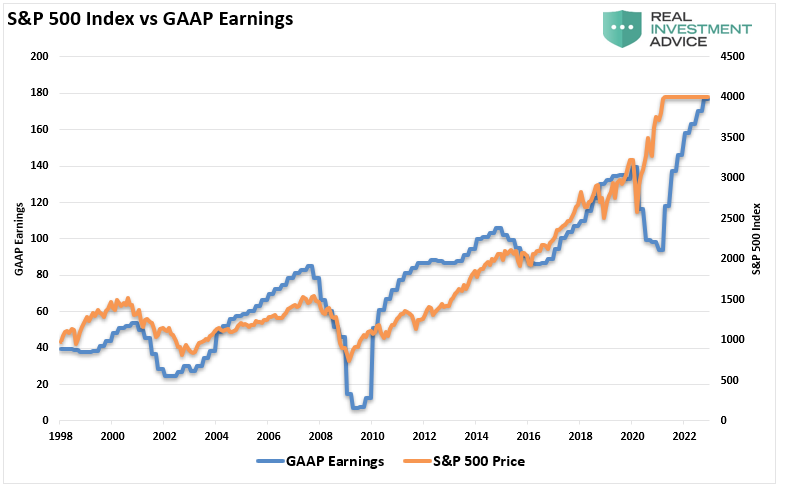

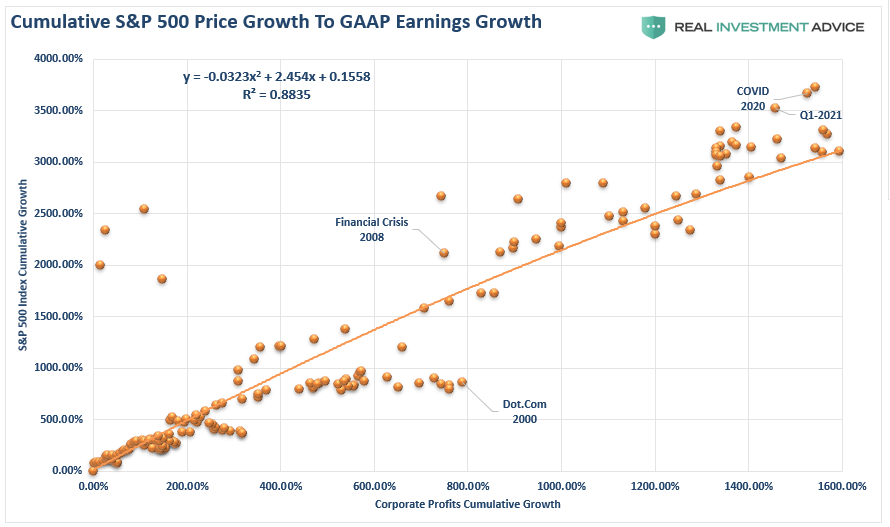

The reason this is important, from an investment standpoint, is the linkage between economic growth and the stock market.

Two Ways To Correct Valuations

In his letter, Dimon noted that stock market valuations are “quite high.” Still, a multiyear boom may justify current levels because markets are pricing in economic growth and excess savings that make their way into equities.

That is a significant statement and one that will most likely be proven wrong.

There is little argument valuations are high. As such, historically speaking, valuations have always reverted by prices falling to align with earnings. However, what Dimon is proposing is a period where prices remain flat while earnings rise.

Such has never happened historically. However, such is particularly relevant given that economic activity drives corporate profits and earnings.

If Dimon is correct about interest rates and inflation, the drag on economic growth will increase.

“Conversely, in this boom scenario it’s hard to justify the price of U.S. debt (most people consider the 10-year bond as the key reference point for U.S. debt. This is because of two factors: first, the huge supply of debt that needs to be absorbed; and second, the not-unreasonable possibility that an increase in inflation will not be just temporary.”

Given the rising inflation and rates divert disposable incomes from consumption. Such suggests that much of the population living paycheck-to-paycheck, any “cost” increase will immediately detract from economic activity.

Mr. Dimon’s Next Bailout

“Americans know that something has gone terribly wrong, and they blame this country’s leadership: the elite, the powerful, the decision makers – in government, in business and in civic society. This is completely appropriate, for who else should take the blame?”

What Mr. Dimon tends to forget is that it was the U.S. taxpayer who bailed out the financial system, he included, following the financial crisis.

Then again, following the economic shutdown.

Despite massive fraud in the major banks related to the mortgage crisis, the banks paid only minor penalties for their criminal acts, and no one went to jail. Before the financial crisis, the top 5-banks comprised 40% of the banking system. Afterward, it became 60%. Through it all, Mr. Dimon became substantially wealthier, while the American population suffered the consequences.

You better believe that Americans know something has gone wrong, and Jamie Dimon is “poster child” for the “financial mafia.”

With the household, corporate, and government debt at a record, the next crisis will require another taxpayer bailout. Since Mr. Dimon’s bank lent the money to zombie companies, households that could not afford it, took on excessive risks in financial assets, he will gladly accept the next bailout while taxpayers suffer the fallout.

While Mr. Dimon points the finger at everyone else, he is the problem. Of course, give any person a billion dollars, and they will likely become just as detached from “serfs” beneath his feet.

At some point, Americans have to stop hoping to magically cure a debt problem by adding more debt and then shuffling it between Central Banks.

But then again, such a statement is also delusional.

Disclaimer: Click here to read the full disclaimer.