Clear And Present Danger? Not So Fast

Before the release of last week’s jobs report, investors were inundated with headlines seemingly suggesting that it wasn’t a matter of “if” but “when” the U.S. economy would enter into a recession. There is no doubt the economy has slowed from its 2018 pace, and recent data has been relatively “mixed” in nature. However, there are some economic numbers that imply there is no clear and present danger of a contraction.

So, what was the “bad” news that brought about the recession narrative? The ISM manufacturing and non-manufacturing surveys. Each of these releases revealed visible drops, coming in well below expectations. Given the current heightened state of anxiety, it comes as little surprise that market commentary took on a bearish economic tone. I’m not trying to dismiss these surveys’ results, but remember, these releases are not “hard” data. Rather, they are just what their name implies—surveys—and they can be subject to shifts in sentiment, especially given the negative trade rhetoric.

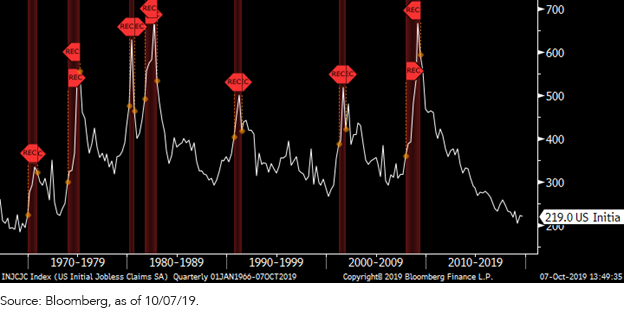

U.S. Weekly Initial Jobless Claims and Recession Periods

Perhaps a better focus and one the Federal Reserve (Fed) is more than likely examining is “actual” economic numbers, a.k.a. “hard” data. The September jobs report certainly fits that bill. While the headline payroll gain was a bit less than forecasted, the previous two months’ upward revisions more than offset the forecast “miss.” In addition, the unemployment rate fell by 0.2 percentage points to 3.5% as a result of another surge in the alternate jobs measure, civilian employment. This gauge surged by +391,000, tripling the number of workers who entered the labor force. In fact, this measure of job gains has now produced a +378,000 average increase over the last four months. To be fair, the year-over-year gain for wages did drop to +2.9%, but this merely reflected a “penny” decline after rising 11 cents in the prior month.

You know another “hard” economic report that is not getting its fair share of attention? U.S. Weekly Initial Jobless Claims. This figure tracks the number of people who have filed for unemployment claims for the first time with a government labor office on a weekly basis and is part of the Leading Economic Indicators series. The level of new claimants has now been below the 300,000 thresholds for over two years, with the most recent print coming in at “only” 219,000. As the graph above illustrates, this reading is relatively rare, especially for such a long period of time, and suggests that an imminent recession would be hard to come by without a sharp reversal in this trend.

Conclusion

Investors beware: Headlines surrounding upcoming economic data will no doubt be “charged” with potential recession language. Besides the money and bond markets, the Fed is also trying to figure out how this will all end up. In other words, data dependency, and potential bond market volatility, will most likely be the norm throughout the remainder of the year.

Unless otherwise stated, all data sourced is Bloomberg as of October 7, 2019.

Disclaimer: Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this ...

more