Carsten Ringler Makes The Basket Case For Gold Equities

TM editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Carsten Ringler, analyst and founder of Ringler Consulting and Research in Germany, strongly believes that precious metals prices will move sharply higher over the next few years and discusses some ratios that point that way. He suggests dedicating a portion of your investment portfolio to two baskets of precious metals equities: one for producers and another brimming with developers and explorers. In this interview with The Gold Report, Ringler takes the long view when it comes to precious metals equities and provides enough names to get you started.

The Gold Report: You prefer to value gold based on its worth relative to other financial benchmarks. Tell us about some of your go-to ratios and why they are meaningful.

Carsten Ringler: I'm looking at different ratios between different baskets of assets like, for example, the gold to real estate ratio. In January 1980, when gold peaked at $850 per ounce ($850/oz), a single-family home in the U.S. was $74,500 and the ratio was 88 oz, meaning it took 88 oz to buy the average home. At the moment a single-family U.S. home averages $237,400, which means you would need 202 oz gold to buy that house in today's market. Factoring in inflation since 1980 by using the CPI calculator from the Federal Reserve Bank of Minneapolis, gold should be around $2,473/oz. That means gold is very much undervalued.

Another ratio I look at is gold versus the Philadelphia Gold and Silver Index (XAU:NASDAQ), which consists of a basket of different gold and silver producers. I divide the price of this index by the gold price, and the ratio is currently .0417, but at its peak on May 31, 1996, the ratio was 0.38. That means the value of the gold and silver producers has fallen dramatically over the last 19 years, meaning that there's a lot of upside in precious metals stocks if the market is recovering, perhaps even 500–700% upside.

And the ratio between the S&P 500 ETF Trust (SPY:NYSE.Arca) and the Market Vectors Junior Gold Miners ETF (GDXJ:NYSE.Arca), a basket of junior gold producers, is 0.095 versus a high of 1.41 on Dec. 6, 2000. That means essentially the same thing. If we are going back to the ratio highs that we hit a few years ago, there's huge upside in gold mining stocks.

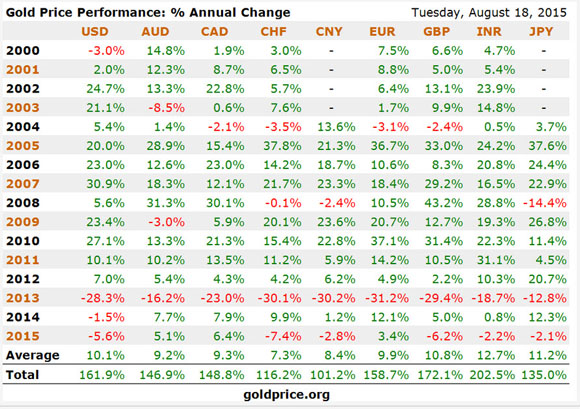

TGR: You use a chart that shows gold's annual price performance since the year 2000. Over that 15-year period, gold has increased an average of roughly 10% annually in all currencies. Isn't that chart really about the monetary expansion that has taken place over that same period?

Source: goldprice.org

CR: Absolutely. Since the financial crisis in 2008–2009, many central banks have been printing money to avoid deflation. Until 2011, the correlation between money printing and higher precious metals prices was quite high. I see gold and silver as currency; precious metals have anchored financial systems for thousands of years and do have a positive track record.

I'm really bullish on gold and silver, especially silver because it is used in more than 10,000 industrial applications. About 800 million ounces (800 Moz) of silver are coming from mine supply, plus an additional 200 Moz come from recycling each year, currently worth roughly $15 billion ($15B). But the U.S. national debt grows by $6.2B every 24 hours. This kind of monetary system is fragile. If people lose their confidence in the paper currency system, there could be a big run into the tiny precious metals market, not only to physical metals but into precious metals mining stocks as well.

TGR: That said, how do you explain gold's poor performance, basically since 2011?

CR: In 2000, gold was at $260/oz but then, at the late stage of the bull cycle, a lot of speculative money went into precious metals and gold spiked at $1,922/oz in September 2011. This was an overheating moment that triggered a heavy selloff. I still see further downward momentum before the upswing.

TGR: Do the current depressed valuations for precious metals stocks, in general, mean that they are undervalued or is this an accurate reflection of where metal stocks should be given current metals prices?

CR: That is the big question. If you look at the big gold producers like Kinross Gold Corp. (K:TSX; KGC:NYSE) or Barrick Gold Corp. (ABS:TSX; ABX:NYSE), they made significant mistakes when the gold price was hot, and they are being punished because they took on a lot of debt. Barrick's debt, for instance, is about $13B. Companies like that have been beaten down quite dramatically. But even small gold producers that are generating free cash flow are getting beaten down, too, like Teranga Gold Corp. (TGZ:TSX; TGZ:ASX) (TGCDF), the biggest gold producer in Senegal. But this is where there is value—the small- to mid-cap producers with low all-in sustaining costs, solid balance sheets and good management teams. These companies will survive these metals prices. And because they have been beaten down, say, 70–80%, the risk is lessened. Only the smart money is investing in these companies at these metals prices. But now is a good time to build a basket of interesting precious metals producers, and maybe another basket of interesting developers.

TGR: How should investors handle the precious metals equity portion of their portfolios given the current market conditions?

CR: That depends on an individual's risk profile. If you have a good stomach for risk, perhaps you should buy now, even if the market goes down another 20–30%. Buy on the way down and sell on the way up, that's what I'm doing in my portfolio—it is definitely a strategic way to buy a basket of hand-selected companies. I also suggest owning a good portion of physical metals in this kind of market environment. It is the money of last resort.

TGR: What are some overriding themes that you're taking advantage of?

CR: I'm quite bearish on the global equity markets. We saw a huge bull market from 2009 to 2015 on the S&P 500, when it went to around 2,080 from 666. That market is really mature. One number that scares me is the high margin debt on the New York Stock Exchange (NYSE). When the big market crash happened in 1987 we saw $38B in margin debt, but as of June 2015, NYSE margin debt was more than $504B. Everyone is dancing until the music stops. So I'm shorting the S&P 500, while building my basket of different precious metals producers.

TGR: Do you see the U.S. Federal Reserve raising rates in September?

CR: I see the Fed making some kind of small move, maybe 25 basis points. The economy is not in the best shape and if the Fed raises rates too much the dollar could become much stronger, which could hurt domestic industry and exports.

TGR: What are some gold producers that you are following and that continue to perform despite lower gold prices?

CR: One name is Metals X Ltd. (MLX:ASX) (MLXEF), based in Australia. The company is producing gold and is also Australia's biggest tin producer. It has a huge nickel project, too. Metals X will produce around 160,000 ounces (160 Koz) gold this year, but could reach around 450 Koz inside two years. The market cap is AU$449M, and the weak Australian dollar lowers its overall production costs.

TGR: In 2014–2015, Metals X produced 150 Koz at all-in sustaining costs (AISC) of AU$1,170/oz. Where is that growth going to come from?

CR: The growth should come from the Central Murchison gold project (CMGP) in Western Australia and the Rover project in the Northern Territory. CMGP could initially add another 196 Koz per year for the first 10 years of production. The stock has performed extremely well, going from to AU$1.59/share from AU$0.74/share in one year. The company also owns a sizable nickel project, which could be exciting at higher nickel prices.

TGR: What other names do you like?

CR: I also really like Klondex Mines Ltd. (KDX:TSX; KLNDF:OTCBB). The share price is up 70% since the beginning of 2015.

TGR: Klondex recently published the assay results from 44 holes at Fire Creek in Nevada. While the grades were a bit lower than expected, the widths were wider. What do those results ultimately mean for the company?

CR: The results are very positive. The drill campaign confirmed that Fire Creek is a high-grade asset that is underexplored. All of those results will be put into a new resource model. The company generates free cash flow on production, even in this market. Klondex has an underutilized 1,200-ton-per-day (1,200 tpd) mill, so it has the capacity to further boost production. I think management did an excellent job delivering what it said it would deliver.

TGR: And until recently the tonnage that Klondex could actually mine was capped. But the cap has been lifted.

CR: That was a big milestone, and until it was lifted Klondex produced gold under a bulk-mining permit. Now that the company has no restrictions, it can mine more ore there. All the news in the last two or three months has been quite positive. I expect the company to grow in the coming years.

TGR: Are there others you want to share with us?

CR: Another company I really like is Timmins Gold Corp. (TMM:TSX; TGD:NYSE.MKT). Timmins has been punished since the beginning of the year for the Caballo Blanco and Newstrike Capital Inc. acquisitions. The stock traded in 2012 above $3 and now it is at $0.36, but I think it is wise to buy gold assets when prices are cheap. If gold reaches $1,500/oz or higher, those projects are going to heat up again. The management team has proven to be good operators. The same team built the producing San Francisco mine on time and on budget. I saw the numbers from Q2/15 and I think the company could eventually get to $13–15M in operating cash flows if gold averages $1,250/oz per annum. Timmins has a lot of leverage if the market recovers. At $1,350–1,500/oz gold, the company could easily fund Ana Paula and/or Caballo Blanco, and be in a good position for the next bull market.

TGR: So you still have faith in management?

CR: I'm confident that CEO Bruce Bragagnolo will see the company through the tough times. I think we will see higher gold prices in the next 12–18 months. My price target on Timmins is $1.40.

TGR: What are some companies you're following on the silver side?

CR: Endeavour Silver Corp. (EDR:TSX; EXK:NYSE; EJD:FSE) is one of my favorite silver producers and I own shares in it. It has really good management. CEO Brad Cooke has been heavily involved with shareholders since 2004, and the management team all owns significant amounts of shares. Endeavour has purchased mines that were not profitable and turned them around. Terronera (formerly San Sebastián) is the company's next mine. Endeavour is driving down cash costs but is not making any big profits on annual production of 10–11 Moz silver equivalent at these low silver spot prices. This could be a $700M–1B market-cap company if the silver price reaches $28/oz.

I also like Newmarket Gold Inc. (NGN:TSX.V) (NMKTF). It has three mines in Australia. In H1/15 the company posted US$54.6M in operating cash flow on production of 115.6 Koz at AISC of US$985/oz. The company should produce around 205–220 Koz gold in 2015 at AISC of US$1020–1,100/oz. Most of its costs are in Australian dollars, so the company has really good margins. It also has 6.7 Moz in gold resources in all categories.

TGR: You also follow a number of precious metals developers and explorers. Tell us about some of those names.

CR: One company that is not well known is London-based Hummingbird Resources Plc (HUM:AIM) (HUMRF). It has two interesting gold projects in Africa. One is Yanfolila in Mali, which is fully funded and under construction. The ramp up to commercial production should begin in mid-2016. AISC are expected to be $733/oz on production of 79 Koz per year. Gold Fields Ltd. (GFI:NYSE) invested $100M on Yanfolila before it sold the project to Hummingbird, so the company has a $65M tax credit against any profits. The company also has the Dugbe project in Liberia, which hosts 4.2 Moz gold and could produce 125 Koz annually once it is in production. This is Liberia's largest gold deposit. Hummingbird's market cap is £25M—undervalued and unbelievable. I'm also a Hummingbird shareholder.

TGR: Any others?

CR: I also like Integra Gold Corp. (ICG:TSX.V; ICGQF:OTCQX). It owns the Lamaque project in Val-d'Or, Québec, a mining-friendly jurisdiction. The company owns a high-grade resource, very good infrastructure and a mill, which needs to be refurbished. The updated preliminary economic assessment published in January predicted a 77% internal rate of return at $1,175/oz gold. The company also bought the Lamaque North project for about CA$8M. When the market is better, this could be a takeout candidate.

Another company among the developers is Altona Mining Ltd. (AOH:ASX), which is developing the fully permitted and licensed Cloncurry copper-gold project in Queensland, Australia. The company has $47M cash and a joint venture partner in Sichuan Railway Investment Group. Signing of the final joint venture agreement is expected by February 2016. The project could reach production by 2018 at AISC of US$1.96/pound (US$1.96/lb) net of byproduct credits. At the moment copper prices are weak, but much could change in three years. This could be a really interesting project at $3.25/lb copper.

TGR: Perhaps one more name before we wrap this up?

CR: Another one that I really like is Pretium Resources Inc. (PVG:TSX; PVG:NYSE), which is developing the high-grade Brucejack project in British Columbia. It has a Proven and Probable resource of 7.5 Moz gold. If Pretium gets all the necessary mining permits and licenses for Brucejack, the funding will come in short order. Zijin Mining Group has invested CA$81M for a 9.9% stake. This is one of the few projects that would still be profitable at $800–900/oz gold. This is a really sexy and attractive project in my eyes. There are so many interesting developers out there.

TGR: What's on your must-have checklist for precious metals companies?

CR: Everyone should have their own checklist but all companies have to have enough money in the treasury to survive turbulent precious metals prices over the next 12–18 months. They have to have good management with significant ownership stakes. And each company should have a project that is likely to get financed. And then you buy in stages. You establish a position and if the market is gets weaker, you buy more. And over the next few months buy another portion as the company publishes positive news. But you want to hold these positions for the long term; that means that if the gold price goes back to its former highs or higher, which I think is possible in the next couple of years, then those companies will become cash cows. And if they are developers like Hummingbird or like Altona, then the metals in the ground will be valued at higher multiples. This is my strategy.

TGR: Provide our readers with some hard-earned German wisdom as they ride the waves of a choppy summer in the gold market.

CR: Do your homework and buy companies you believe in by building a position in different stages in different tranches on the way down and sell as the stock moves higher. You never hit the bottom or the top. Go with the company through all the ups and downs but also take some profits. If you are up 100%, maybe take 20–25% from your profits and choose another name with an outstanding management team and good project. Another bit of wisdom: be your own central bank. Hold precious metals in your hands because when all else fails, gold and silver are money.

TGR: Thank you for your time.

Carsten Ringler founded Ringler Consulting and Research GmbH in 2014. He represents the company as a managing director and analyzes mining companies, as well as the commodity sector. One of the consulting services is the creation and distribution of research reports on mining companies. Ringler has extensive capital market experience in trading and valuation of stocks, fixed income and money market products. His trading career began in 1991 when he worked for Deutsche Bank AG on the trading floor of the German stock exchange in Frankfurt.

Carsten Ringler founded Ringler Consulting and Research GmbH in 2014. He represents the company as a managing director and analyzes mining companies, as well as the commodity sector. One of the consulting services is the creation and distribution of research reports on mining companies. Ringler has extensive capital market experience in trading and valuation of stocks, fixed income and money market products. His trading career began in 1991 when he worked for Deutsche Bank AG on the trading floor of the German stock exchange in Frankfurt.

Disclosure:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of more