Are Tech Stocks Cheap?

Are technology stocks cheap? It seems like a strange question to ask as the market drops on news that Apple has indicated weaker future sales. I also doubted whether Facebook’s price reflected its business value in the middle of this past summer. I thought fair value for the business was around $140 per share assuming it could grow its free cash flow by a robust 6% annually over the next decade. The stock is now in the $130 range after pushing higher than $200 in the early summer.

But technology isn’t just the FAANG stocks (Facebook, Apple, Amazon, Netflix, and Google). And at least two important firms – DoubleLine and GMO – think the sector is at least relatively cheap. Here’s why.

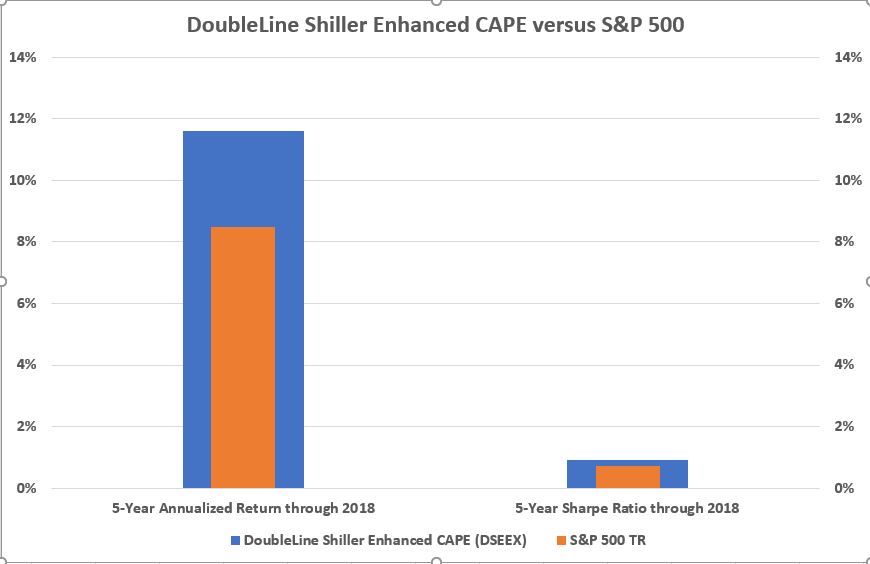

First, technology is trading cheaply on a Shiller PE basis, shown by the fact that the DoubleLine Shiller Enhanced CAPE Fund (DSEEX) holds the sector. By using a bond portfolio as collateral, this fund gains exposure to an equity derivative that delivers exposure to four of the five cheapest S&P sectors (tossing the one with the worst one-year price momentum) on the basis of their Shiller PE ratios — and technology is one of those sectors currently. The Shiller PE, as a reminder, is the current price of a stock, sector, or index relative to its past decade’s worth of real, average earnings. Right now (and for more than a year) technology has come up as one of the four sectors the fund owns, meaning its Shiller PE is lower relative to its own historical average than other sectors’ Shiller PEs are to theirs. The other sectors the fund owns currently are Healthcare, Consumer Staples, and Communication Services.

This mechanical application of the Shiller PE may not satisfy investors looking for more a more absolute definition of value, but, relative to other sectors, technology is cheap on a serious valuation metric. If you’re going to be allocated to U.S. stocks in some way, shape, or form, this is a reasonable way to achieve that allocation.

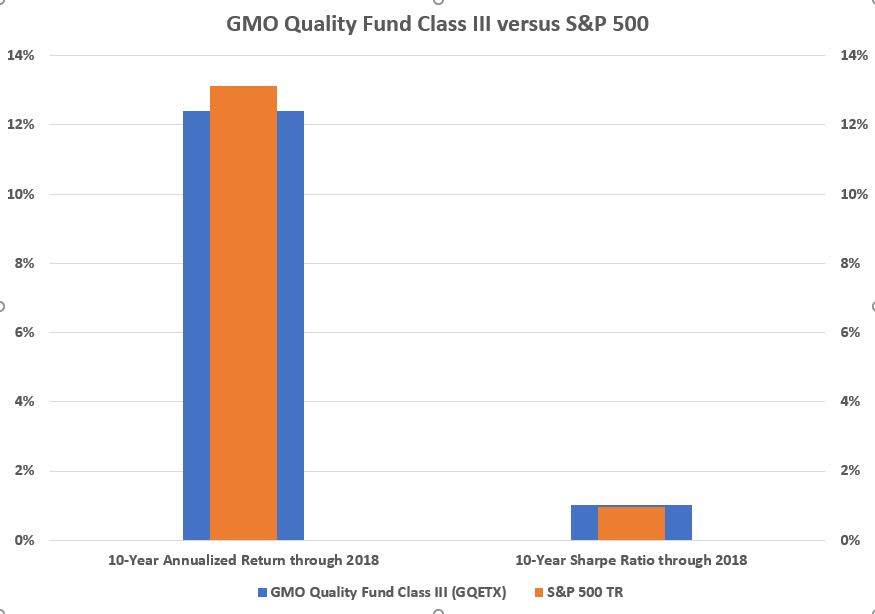

Second, GMO, which is also a fan of the Shiller PE metric, and uses it in its asset class valuation work, also likes technology stocks. The Boston-based firm just published a white paper, written by Tom Hancock, the head of the firm’s Focused Equity Team, arguing that technology stocks were attractive. The firm’s “Quality” strategy has 45% of its assets in technology stocks, “including positions in three of the five FAANG stocks.” Alphabet (Google) and Apple are the two largest holdings of the firm’s Quality mutual fund (GQETX), managed by Hancock.

Rather than relying on traditional valuation metrics when picking individual stocks, the firm looks at how Alphabet, for example, invests in R&D, and how that investment can translate into higher future revenues. In other words, R&D isn’t properly counted as an expense that will never yield future revenue and earnings growth. On the basis of accounting adjustments like this, GMO views Alphabet as a cheap stock.

Hancock notes that GMO’s Quality portfolio doesn’t trade at traditional valuation multiples that are different from the broader market. But, “in an expensive market, quality companies typically trade at higher P/E’s than most ‘value’ investors would like.” Higher multiples are justified for companies with resilient margins and strong business models, and Hancock thinks the strategy can produce returns of 5% in excess of inflation.

Quality companies in the U.S. are also cheaper than those outside of the U.S., and Hancock surmises that’s because of a kind of scarcity value. Companies with consistently high margins and returns on invested capital are less prevalent outside of the U.S., so they trade at dearer prices.

Moreover, the U.S. technology sector consists of a diverse group of stocks. Only one of the FAANGs – Apple – is in the top-10 of the S&P 500 Information Technology Sector. Some of the largest constituents of that sector are the darlings from the technology bubble of nearly 20 years ago – Microsoft, Intel, Cisco, and Oracle. They turned out to be good businesses that were just overpriced then. Hancock lists Microsoft’s virtues as being in the cloud growth business and having a lock on the consumer. Qualcomm, by contrast, has a unique position in the smartphone supply chain, while Oracle provides legacy software and benefits from high switching costs. Finally, Visa and Mastercard are “borderline tech” companies, but, nevertheless, find themselves near the top of the S&P 500 Information Technology sector.

So, despite being known for top-down asset class valuation calls, the GMO Quality strategy is bottom-up and fundamentally oriented. But, just like the more mechanical, single-factor approach of the DoubleLine fund, it also finds technology stocks cheap – or cheaper than their brethren in other sectors.

Both the DoubleLine Shiller Enhanced CAPE fund and the GMO Quality III fund are worthy of investors’ consideration. Beware that the latter is for institutional investors, given its $10 million minimum.