Are Energy Stocks Cheap?

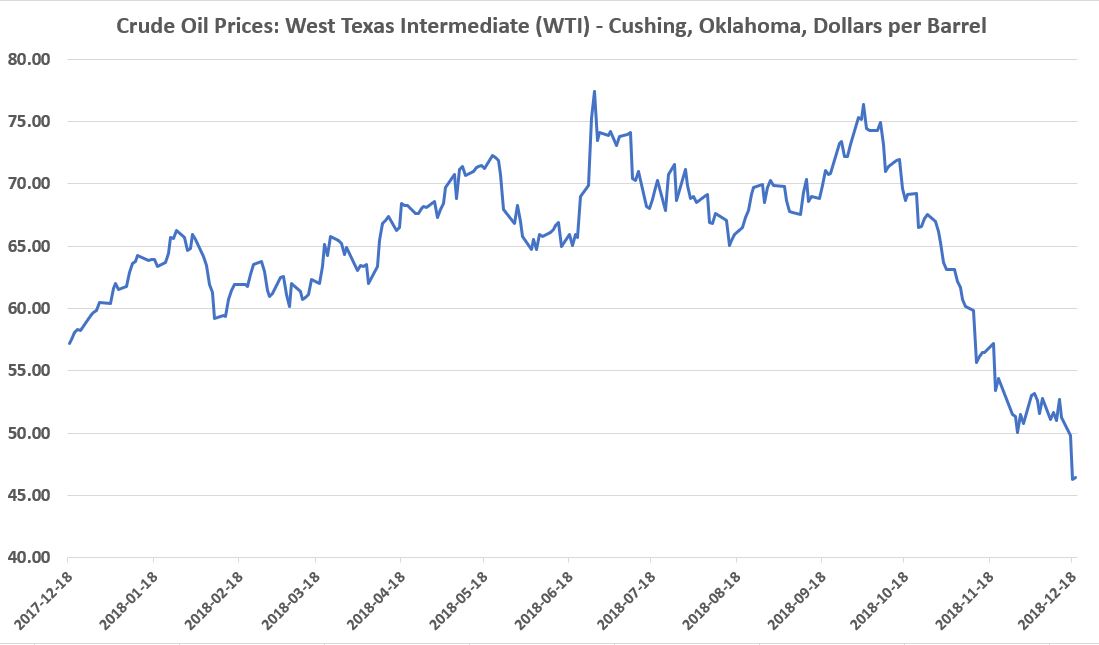

Oil prices have collapsed again from nearly $80 per barrel this past summer to under $50 per barrel now. Big price declines in the commodity always beg the question if there are any cheap stocks in the oil patch.

Let’s start with the domestic behemoth, ExxonMobil (XOM). It’s down from a high of nearly $90 per share this year to a little below $70. It’s trading at a P/E ratio of around 13, a Price/Sales ratio of around 1 and a Price/Book ratio of around 1.6. It’s also yielding well more than 4%. Those seem like reasonable multiples, but let’s move to a cash flow analysis.

The firm has averaged around $10 billion of free cash flow for the past five years, and that includes $14 billion year-to-date and $14.7 billion in 2017. Let’s say the firm averages only $10 billion per year for the next five years. Then let’s say it produces $15 billion in the sixth year and grows at the rate of inflation after that. If we apply a 10% discount rate to those numbers, we arrive at a company worth around $300 billion or a little more than its current market capitalization. In other words, the firm doesn’t have to perform better than it has recently to argue that its current price matches its value. Any improvement in free cash flow would mean its fair value is higher, and also that it should trade that way in a few years. If you have a little time, ExxonMobil should be a good bet if you make it one of a few stocks.

A smaller integrated company, Cenovus (CVE) looks attractive too. It trades at a P/E ratio of less than 5, Price/Sales ratio of 0.52 and a Price/Book ratio of 0.62. It also yields around 2%. The stock has dropped from more than $10 per share earlier this year to less than $7 now.

Cenovus has averaged around d $300 million of free cash flow for the past five years. Let’s say it maintains that for the next five. Then let’s assume it can get to $400 million in the sixth year and grow at the rate of inflation after that. If we apply an 8% discount rate to those conservative numbers, we get a fair value of more than $9 billion. The stock has an $8.6 billion market capitalization now. Just as in the ExxonMobil case, we’re assuming that the company doesn’t improve very much over the next five years.

Last, let’s consider the largest oilfield services company, Schlumberger (SLB). The stock trades at a P/E of 34, a Price/Sales of 1.6, and a Price/Book ratio of 1.43. It yields around 5.3%.

That P/E ratio seems high, but the stock has average around $5.2 billion of free cash flow for the past five years. If it continues to do that for the next five, jumps to $5.5 billion in year six, and then grows at the rate of inflation, we get a company worth over $100 billion if we apply an 8% discount rate. The company’s market capitalization is currently a little over $50 billion.